May 04, 2026 – Space security, AI fintech, and enterprise automation captured the bulk of weekly deal flow. Three defence-linked rounds alone accounted for nearly half of all capital deployed.

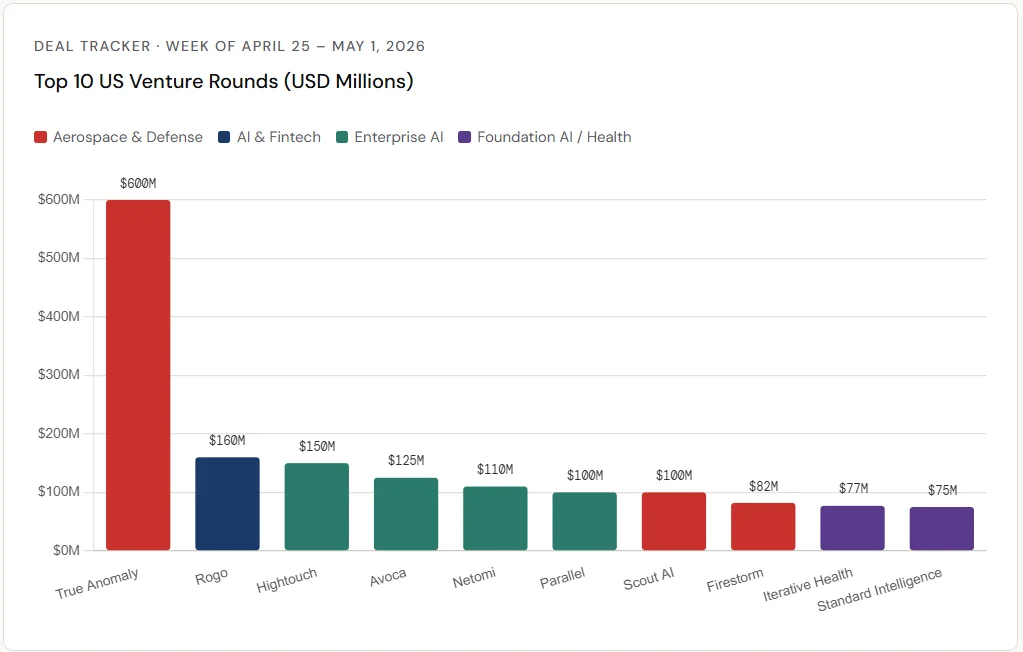

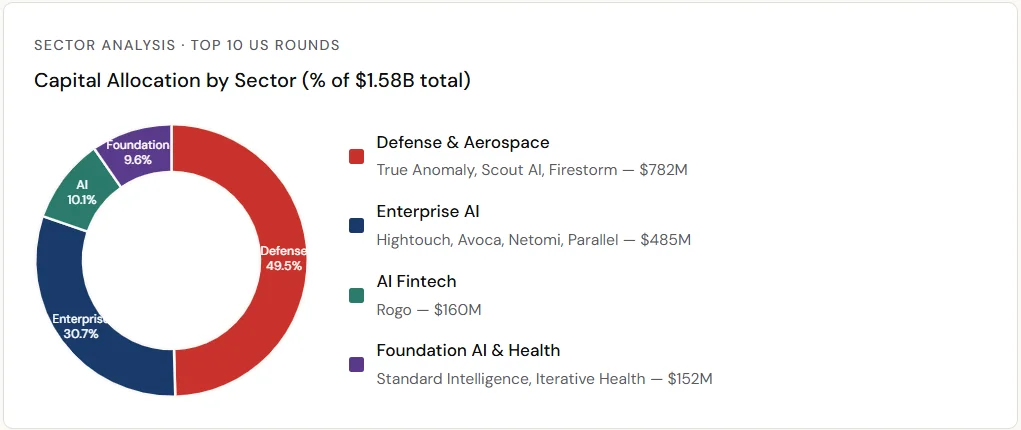

The week ending May 1, 2026, was a defining moment for defence venture capital. Three aerospace and defence startups raised a combined $782 million. That figure represents 49.5% of the week’s total top-ten US deal flow, per Crunchbase data.

This is not a one-week anomaly. It reflects a sustained investor pivot. The sector raised a record $7.7 billion in 2025. Geopolitical pressures and dual-use technology trends are now structural investment themes.

True Anomaly Sets the Pace for Space Security

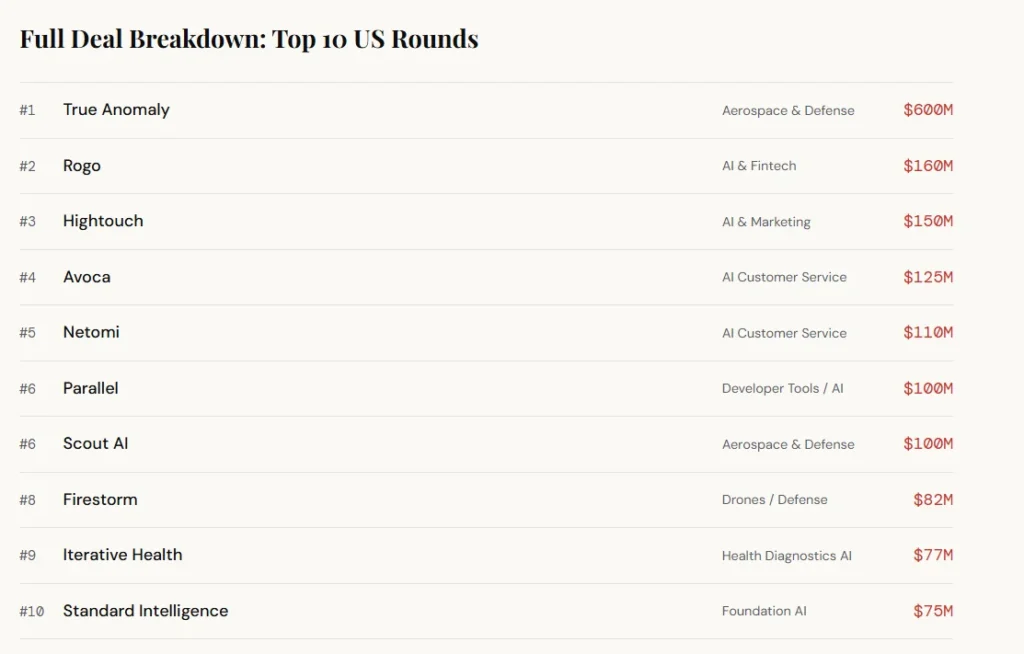

The week’s biggest deal belonged to True Anomaly. The Centennial, Colorado startup closed a $600 million Series D round. Eclipse and Riot Ventures co-led the raise. Accel, Menlo Ventures, and Paradigm also participated.

True Anomaly builds in-orbit defence and space security systems. Its total funding now stands at $1.1 billion. That positions it firmly as a category-defining company in a sector few VCs touched five years ago.

Two more defence-linked deals followed. Scout AI, a Sunnyvale-based firm building AI for aerospace applications, raised $100 million in a Series A. Draper Associates and Align Ventures led. Meanwhile, San Diego drone company Firestorm closed an $82 million Series B. Lockheed Martin and In-Q-Tel were among its backers.

Scout AI’s large Series A is itself a signal. A $100 million early-stage round for a defence AI startup shows how much investor conviction has shifted. Crunchbase noted a record high in defence startup funding globally in 2025. The trajectory shows no sign of reversing.

AI Is Rewriting Financial Research

The second-largest deal of the week went to Rogo. The New York-based AI startup secured $160 million in a Series D. Kleiner Perkins led. Sequoia Capital and J.P. Morgan Growth Equity Partners joined.

Rogo builds AI tools that automate financial research workflows. Its total funding now tops $314 million. The deal is consistent with a broader pattern. Investors are betting on AI replacing costly manual processes in banking and asset management.

High-value knowledge work is in the crosshairs. Law, accounting, and financial research are all seeing significant AI deal flow. Rogo targets the same structural shift: fewer analysts doing more with AI-assisted tools.

Enterprise AI Commands Mid-Market Rounds

Four enterprise AI deals clustered in the $100–$150 million range. Together, they raised $485 million. That’s a meaningful share of the week’s total US deal activity.

Hightouch raised $150 million in a Series D. Bain Capital Ventures and Goldman Sachs Alternatives co-led. The San Francisco startup provides agentic AI for marketing data activation. Its total funding reached $332 million.

Avoca brought in $125 million in a Series B. General Catalyst and Meritech Capital Partners led. The New York company automates customer communication workflows using AI agents.

Netomi closed a $110 million Series C led by Accenture Ventures. Notable angels included OpenAI co-founder Greg Brockman and Mustafa Suleyman of Microsoft AI.

Parallel closed a $100 million Series B. Sequoia Capital led, with Index Ventures and Kleiner Perkins joining. The Palo Alto startup is building a suite of AI developer agents.

Foundation Models and Health AI Round Out the Week

Standard Intelligence raised $75 million in a Series A. Spark Capital and Sequoia co-led. The pre-money valuation was set at $425 million. Notable investors included hedge fund titan Stanley Druckenmiller and AI researcher Andrej Karpathy.

Standard AI trains large models on video data rather than annotated screenshots. This approach targets cost reduction and scalability in “computer-use” AI, a fast-growing category.

Iterative Health closed a $77 million Series C round, with Google Ventures leading alongside Intrepid Growth Partners. The Cambridge, Massachusetts, company applies AI to gastroenterology diagnostics. Its total raised now exceeds $268 million.

Defence and space security are no longer fringe bets. They are the dominant conviction plays of 2026 venture capital.

Global Deals: Europe Breaks Records, China Pushes Robotics

Outside the US borders, the week produced three significant international raises. London-based Ineffable Intelligence closed a $1.1 billion seed round. Lightspeed and Sequoia led. It is the largest seed round ever recorded for a European startup.

That record was set just weeks after Paris-based Advanced Machine Intelligence raised a $1.03 billion seed. Europe is now producing frontier AI labs at a scale that rivals Silicon Valley’s early-stage output.

In China, Volant Aerotech raised $300 million for its electric vertical takeoff aircraft. Robotica pulled in $200 million in industrial humanoid robotics. S.F. Express and Tsinghua Holdings joined that round.

The week’s global picture is clear. Capital is concentrating on defence tech, foundational AI, and autonomous systems. The competition across geographies is intensifying rapidly. Q1 2026 was already a record-breaking quarter for global AI startup funding. This week’s data adds further weight to that trend.

What This Week Tells Us

Three themes define this week’s deal flow. First, defence and space security have become the market’s highest-conviction bets. True Anomaly alone raised more than the combined totals of any three other companies on the list.

Second, enterprise AI is maturing fast. Four companies offering AI agents for marketing, customer service, and developer tools all raised above $100 million. That signals strong enterprise adoption and real revenue traction.

Third, the foundation model race has no finish line. Investors backed Standard Intelligence, Ineffable Intelligence, and Advanced Machine Intelligence in a single week. Competition at the model layer remains fiercely funded.

The data points to one simple conclusion. Capital is no longer searching for AI’s use case. It has found several and is now scaling them aggressively.