July 17, 2026 – The Middle East war is reshaping commodity prices for years, not months, as Hormuz flows shrink and Brent crude defends a high floor.

In Summary

A leading materials index is forecast to climb almost 35% into the third quarter of 2026.

Prices ease later but stay above 2025 levels every quarter through 2028.

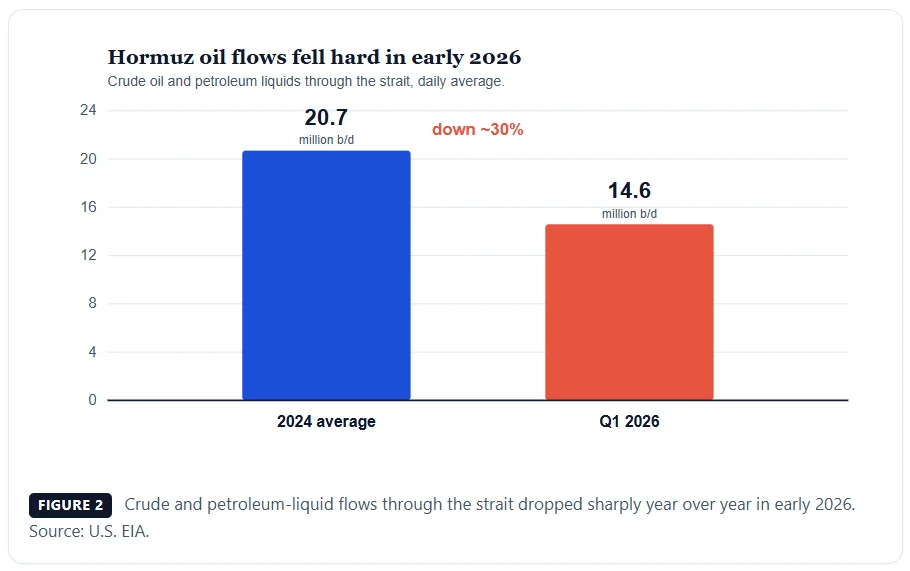

Hormuz oil flows fell to 14.6 million barrels a day in early 2026, down nearly 30%.

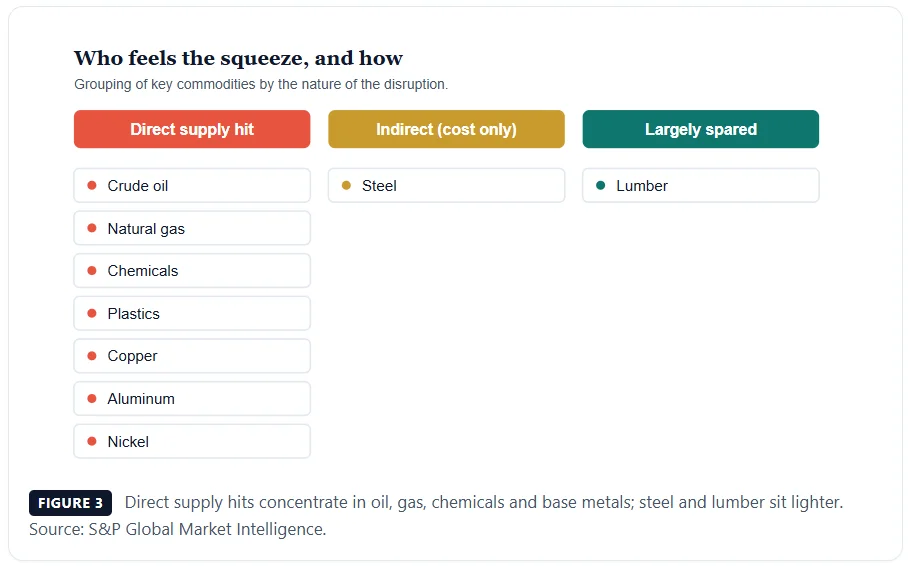

Oil, gas, chemicals, plastics, and base metals face direct supply hits; steel and lumber less so.

Brent crude is projected to hold above $100 a barrel into 2028.

Commodity prices will stay high long after the Middle East war ends, new data shows. Experts now see a “higher for longer” path across energy, metals, and chemicals. Moreover, that strain looks set to run through 2028.

The war has already lifted costs across the board. However, the deeper story lies in how slowly the market can heal. Refilling stockpiles, fixing damaged plants, and reopening sea lanes all take time. So buyers face steep bills even after a truce arrives.

A “higher for longer” price path

A leading price gauge captures the shift well. The index tracks a broad basket of raw inputs each week. Experts expect it to jump almost 35% between late 2025 and the third quarter of 2026. Later, prices should ease through 2027 as demand softens. Still, the gauge remains above the 2025 level every quarter. Indeed, even the last quarter of 2028 sits higher than the end of 2025.

This path matters because commodity prices feed straight into factory costs. As a result, higher input costs ripple through to food, fuel, and finished goods. Consequently, homes and firms absorb the strain side by side.

The Hormuz chokepoint

A single waterway explains much of the pressure. The Strait of Hormuz, the world’s most vital oil chokepoint, carries roughly a fifth of the world’s seaborne oil. In 2024, about 20.7 million barrels of oil moved through it each day, official energy data show. The strait also handles a large share of global gas cargoes. Because so few other routes exist, any blockage hits markets fast.

The war has sharply choked those flows. During the first quarter of 2026, daily volumes fell to 14.6 million barrels. That drop marks a nearly 30% decline from a year earlier. Furthermore, freight and insurance costs climbed as tankers avoided the region. Meanwhile, buyers scrambled to source barrels from farther away.

Natural gas markets feel the same tight grip. The strait moves a large slice of global gas trade too. When cargoes stall, spot gas prices jump in Asia and Europe. Consequently, power bills and heating costs edge higher across both regions. That squeeze then bleeds into the wider cost base.

Winners, losers, and shortage risk

Energy sits at the heart of the shock. Nevertheless, the damage spreads well beyond crude. Chemicals, plastics, and base metals all face direct hits. Copper, aluminum, and nickel land squarely in the firing line. In contrast, steel escapes the worst direct blows. Instead, it suffers from costlier transport and softer demand. Lumber, notably, dodges direct harm.

Oil holds a high floor

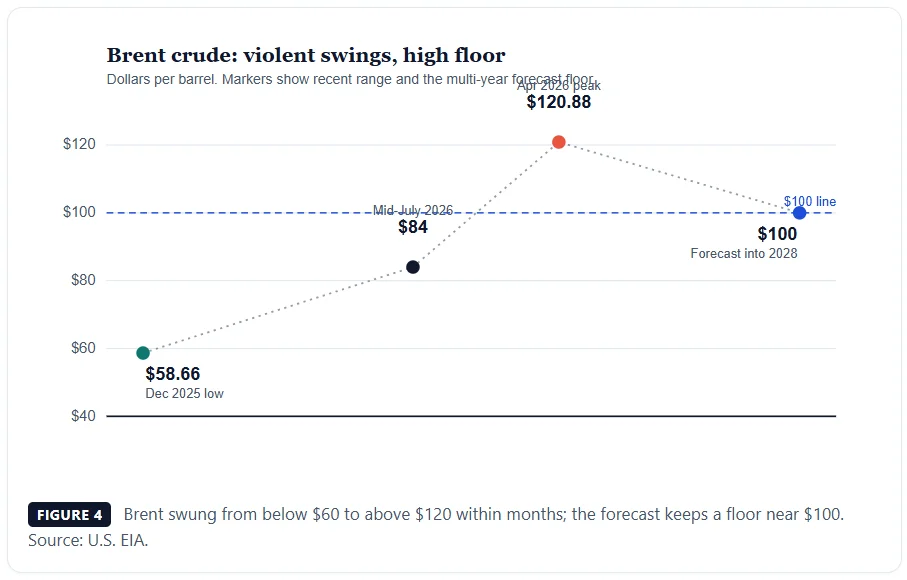

Oil prices tell the clearest story for readers. Brent crude has lately traded near $84 a barrel. Earlier in 2026, the grade spiked above $120 amid fears. Later, a brief truce pulled prices back toward $60. However, fresh strikes near the strait revived supply worries. Experts now expect Brent to hold above $100 into 2028. This view reflects thin stockpiles and lasting plant damage.

Aluminum shows how supply can stay tight for months. Output from Gulf smelters dropped sharply during April. Recovery will come slowly, so prices will stay firm. Additionally, new capacity from Southeast Asia offers only partial relief. Chemicals follow a similar path of stubborn strength. Buyers will pay far more than 2025 rates through 2027.

Steel breaks from the pack in a useful way. Prices should peak in the second quarter across most regions. Afterward, softer demand and easing costs pull them lower. The United States, though, may see its peak arrive later. Overall, the metal offers a rare pocket of relief.

Shortage risk still hangs over several key inputs. If the strait stays shut, stockpiles could run dry. Helium, vital for chip plants, tops the worry list. Similarly, sulfur feeds fertilizer, copper refining, and nickel refining. Aluminum could also hit painful limits under a longer siege. Although this case is not the base view, it tilts risk upward.

Asia carries the heaviest load from the squeeze. The region buys vast volumes through the strait each day. As a result, its plants feel cost pressure first and hardest. Money spent on fuel and food cannot fund other purchases. Therefore, appliance sales and building budgets may shrink.

What comes next

The forecast rests on one central bet about the strait. Experts expect a slow return to normal traffic over the summer. Should that hold, energy costs and demand both ease later. Yet the recovery still leaves prices well above pre-war marks. Because damage lingers, the market cannot simply snap back.

What buyers should do

Buyers can take practical steps despite the doubt. First, they should lock in supply where contracts allow. Second, they can spread sourcing away from the strait. Finally, they should monitor stock levels for early signs of shortages. Smart hedging can also cap exposure to sudden price spikes. Clear contracts and firm timelines give suppliers useful certainty. These moves will not erase the pain fully. Still, they can soften the blow as commodity prices settle higher.

Traders should also weigh how policy shifts sway the path. Central banks monitor fuel costs closely when setting rates. Higher energy bills can keep inflation sticky for longer. Thus, rate cuts may come slower than many hoped. In turn, that stance can cool growth and temper demand.

The bottom line stays simple for planners and investors. Commodity prices have entered a slower, costlier chapter. Even a swift peace would not reset the clock at once. So firms should budget for high inputs well into the decade.