June 22, 2026 – The Wall Street giant wants its Chase digital bank in three more European countries within five years, the Financial Times reports.

In Summary

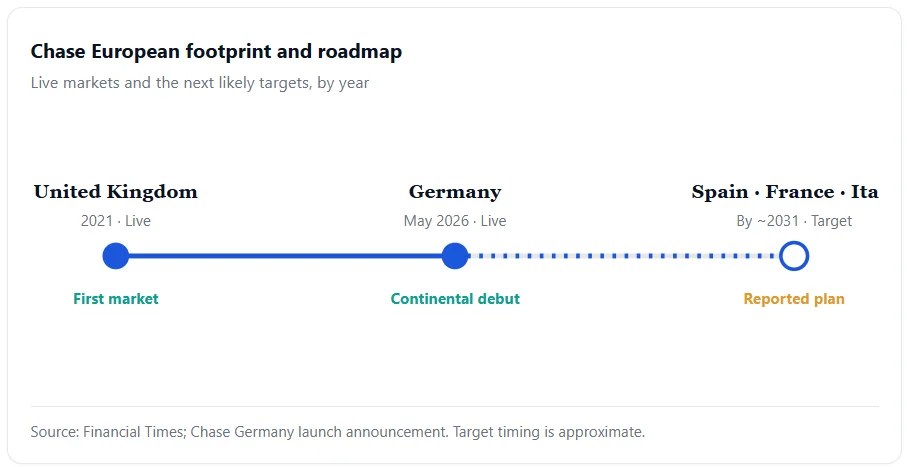

JPMorgan plans to grow its Chase digital bank into at least three more European countries by about 2031.

Spain, France and Italy lead the target list, according to a Financial Times report.

Chase already runs in the UK and Germany, with current accounts and lending due by 2028.

The bank enters a market led by Revolut, Monzo and N26, where most challengers still chase profit.

JPMorgan wants to take its Chase digital bank much deeper into Europe. The largest US bank by assets holds roughly $4.9 trillion on its balance sheet. Now it aims to add at least three more European countries within five years.

A bigger European bet

The Financial Times first reported the plan, citing people familiar with the talks. American Banker then featured the story in its weekly banking roundup. Spain, France and Italy lead the shortlist of likely markets.

Those three economies hold tens of millions of potential retail customers. Therefore, this push marks JPMorgan’s most ambitious consumer bet outside the United States. The bank already serves more than 80 million customers across the US and UK. European growth could widen that base further still.

From London to Berlin

Chase opened in the United Kingdom in September 2021. That debut became JPMorgan’s first retail bank outside its home market. In May 2026, Chase launched in Germany with a fee-free savings account.

The new account pays 4% for four months, then a variable 2%. Germany rewards savers well, so the offer landed in a receptive market. Moreover, JPMorgan opened a new Berlin office staffed with more than 150 specialists.

The bank chose Berlin over Frankfurt for a clear reason. The city sits close to the talent pool that built N26 and Trade Republic. By 2028, Chase plans to add current accounts, investments and lending in Germany. Consequently, the German rollout now reads like a template for future markets.

The numbers behind Chase UK

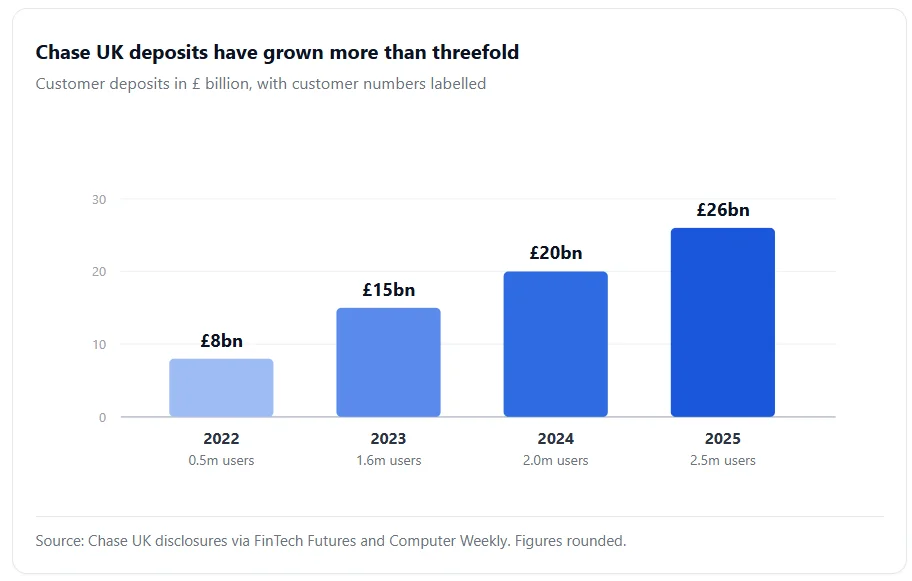

The British business explains JPMorgan’s confidence. Chase UK passed 2.5 million customers by December 2025. Its deposits climbed above £26 billion over the same period.

For comparison, the unit held just £8 billion and 500,000 customers in 2022. Furthermore, the business reached a profitability milestone in late 2025. That moment arrived earlier than several analysts had predicted.

JPMorgan once warned of annual losses of nearly $450 million during the build phase. Yet the bank stayed patient and kept investing. As a result, it now treats Britain as proof that the model travels. The chart below tracks the steady climb in UK deposits.

A crowded, fast-growing market

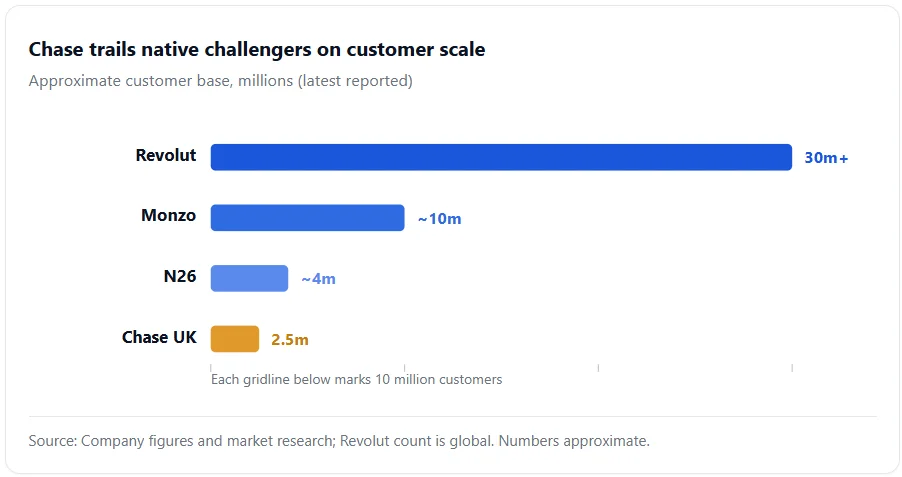

However, Chase enters a fiercely competitive arena. Revolut counts more than 30 million customers worldwide. Investors valued Revolut at nearly $75 billion in a November 2025 share sale.

Monzo serves roughly 10 million customers, mostly in Britain. N26, meanwhile, holds about 4 million active users across Europe. By contrast, Chase UK still trails rivals on raw customer counts. Yet it often leads them on deposits per customer.

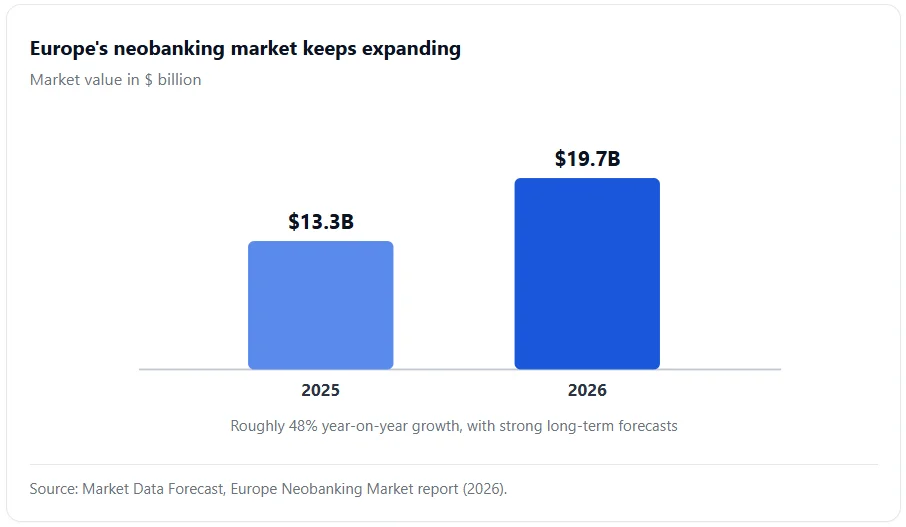

The wider prize keeps expanding, too. Europe’s neobanking market was worth about $13.3 billion in 2025 and may reach $19.7 billion in 2026. The region also remains the world’s largest neobanking market. These charts show the customer gap and the market’s momentum.

The road ahead

Scale alone will not secure victory for Chase. JPMorgan must win trust from savers who already bank locally. It must also satisfy separate rules in Spain, France and Italy. The European Central Bank helps supervise lenders across the eurozone.

Still, JPMorgan brings deep pockets and a long view. The bank absorbed losses on Chase UK for years before profits arrived. Native challengers grew faster on customers, yet they burned cash too. Many neobanks still struggle to turn a steady profit today.

JPMorgan can fund a slow, disciplined build that startups cannot match. If the next launches mirror the UK curve, Chase could reshape European retail banking. For now, though, the expansion stays a plan rather than a firm rollout. Investors and rivals will watch the bank’s next moves closely.