Citigroup warns that oil markets are underpricing supply-disruption risks. A bull case of $150 per barrel is now on the table.

In Summary

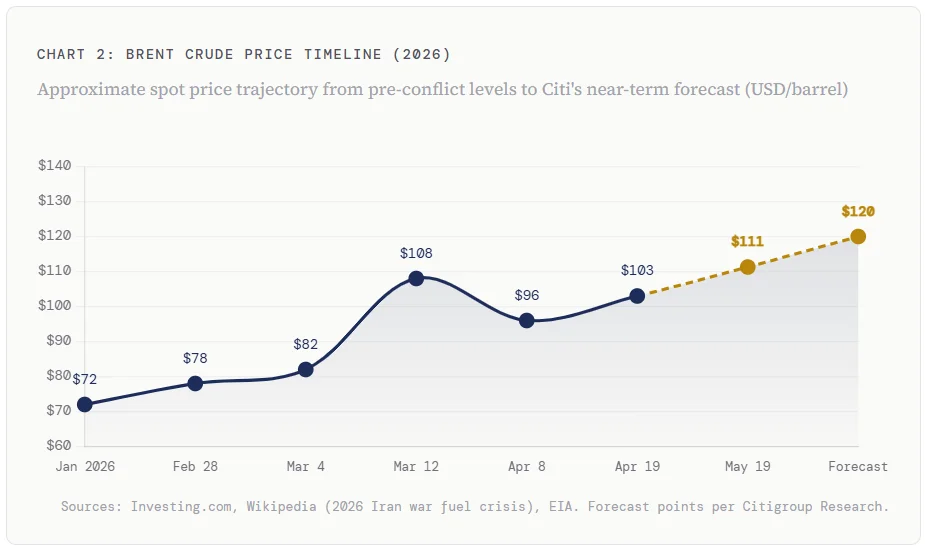

Citi forecasts Brent crude to reach $120 per barrel in the near term.

The bull case pushes to $150 per barrel, assuming the Strait of Hormuz gradually reopens in Q3 2026.

Brent July futures settled at $111.28 per barrel on May 19, 2026.

Citi sees 2026 oil demand growth contracting by 0.6 million barrels per day (mb/d).

Global oil inventories are set to draw by roughly 1 billion barrels this year.

The 2027 central price range sits at $80 to $90 per barrel, contingent on Hormuz access.

Citigroup expects Brent crude to reach $120 per barrel in the near term. The bank warns that oil markets are significantly underpricing supply-disruption risks. Furthermore, Citi outlined a bull-case target of $150 per barrel. This forecast follows Brent July futures, which settled at $111.28 on May 19.

Citi’s Three-Scenario Outlook

Citi has mapped three distinct price paths for crude oil. First, the near-term base case targets $120 per barrel. Second, the bull case pushes to $150 per barrel. However, this scenario assumes the Strait of Hormuz gradually reopens during Q3 2026.

Looking further ahead, the 2027 outlook remains uncertain. Therefore, Citi set a central range of $80 to $90 per barrel for that year. This assumes Iran maintains control of the Strait of Hormuz flows. It also factors in balanced oil exports against long-term demand growth expectations.

The Strait of Hormuz: Why It Matters

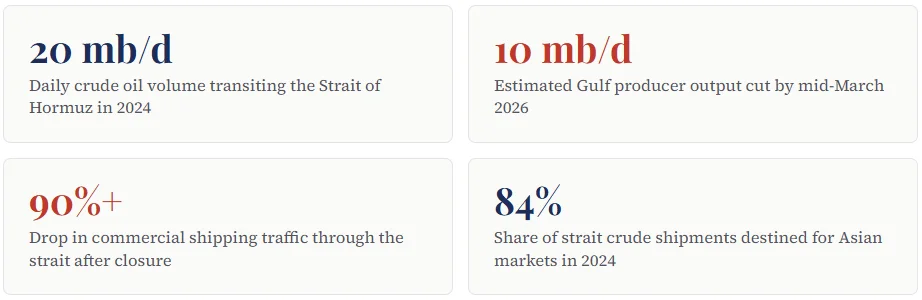

The Strait of Hormuz is the world’s most critical oil chokepoint. According to the US Energy Information Administration (EIA), approximately 20 million barrels transited the strait daily in 2024. That figure represents roughly 20% of all globally traded crude oil. Furthermore, the Strait handles about 20% of the world’s LNG shipments.

Iran declared the Strait closed on March 4, 2026, following the outbreak of the US-Iran conflict. Commercial shipping traffic subsequently dropped by more than 90%. Consequently, the International Energy Agency (IEA) described this as the largest supply disruption in global oil market history. Iraq, Kuwait, and Saudi Arabia collectively cut output by at least 10 million barrels per day by mid-March.

“Oil markets are under-pricing the risk of a prolonged supply disruption and broader tail risks.”

-Citigroup Research Note, May 19, 2026

Supply Squeeze: Demand and Inventory Data

Citi also weighed in on global demand and inventory trends. The bank forecasts 2026 oil demand growth to contract by 0.6 million barrels per day. However, Citi warned that this figure overstates the extent of real consumption declines. Inventory drawdowns and refinery cuts mask relatively limited destruction of end-use demand.

Moreover, Citi estimates global oil inventories will draw down by approximately 1 billion barrels in 2026. This significant inventory drain further tightens the global supply balance. Therefore, any supply recovery will take considerable time to translate into lower pump prices.

The Geopolitical Backdrop

US Vice President JD Vance reported progress in US-Iran negotiations on May 19. Neither side expressed a desire to return to military action. Accordingly, Brent futures dipped slightly on the news, settling at $111.28 per barrel.

Nevertheless, tensions remain fragile. Iran previously launched attacks on US-flagged ships using cruise missiles, drones, and small craft. A ceasefire took hold on April 7 and 8, but strait traffic remains well below pre-war levels. In May, the UK deployed drones, fighter aircraft, and a Royal Navy warship to defend commercial shipping routes.

The Federal Reserve Bank of Dallas estimated that a three-quarter supply disruption could reduce global real GDP growth by 1.3 percentage points. This underscores how much economic damage a prolonged standoff could cause. Even a two-quarter disruption implies a 0.3 percentage-point drag on global output.

A Word on Broader Risks

Warren Patterson, head of commodities strategy at ING, observed that oil prices are being whipsawed by developments in the Middle East. He noted that de-escalation and re-escalation are alternating rapidly. This volatility makes directional commodity trading particularly challenging right now.

Beyond oil, the Strait disruption has rattled LNG, fertiliser, and food markets. Over 30% of globally traded urea exports normally transit the Strait of Hormuz. Therefore, a prolonged closure carries severe knock-on effects for global agriculture and food security.

What This Means for Markets

Oil at $120 per barrel would spread energy inflation across all sectors. Airlines, manufacturers, and consumers would face sharply higher costs. Therefore, central banks will find it harder to cut interest rates.

Additionally, emerging markets with large oil import bills are especially vulnerable. Countries including Pakistan, Bangladesh, and Vietnam already face severe fuel shortages. A further price surge to $150 would deepen these economic pressures considerably.

Three Key Signals to Watch

- Any reopening of the Strait of Hormuz to commercial shipping. Even a partial reopening could rapidly shift price momentum lower.

- Progress in US-Iran diplomatic negotiations. A durable peace agreement would sharply reduce tail risk premiums embedded in crude prices.

- OPEC+ production responses to the supply gap. Any coordinated output increase from non-Gulf producers could cap the upside.