July 14, 2026 – Five of the largest US lenders report second quarter results before Tuesday’s opening bell. Meanwhile, the June inflation print lands in the same hour.

In Summary

Bank earnings and the June price print land within 90 minutes of each other on Tuesday.

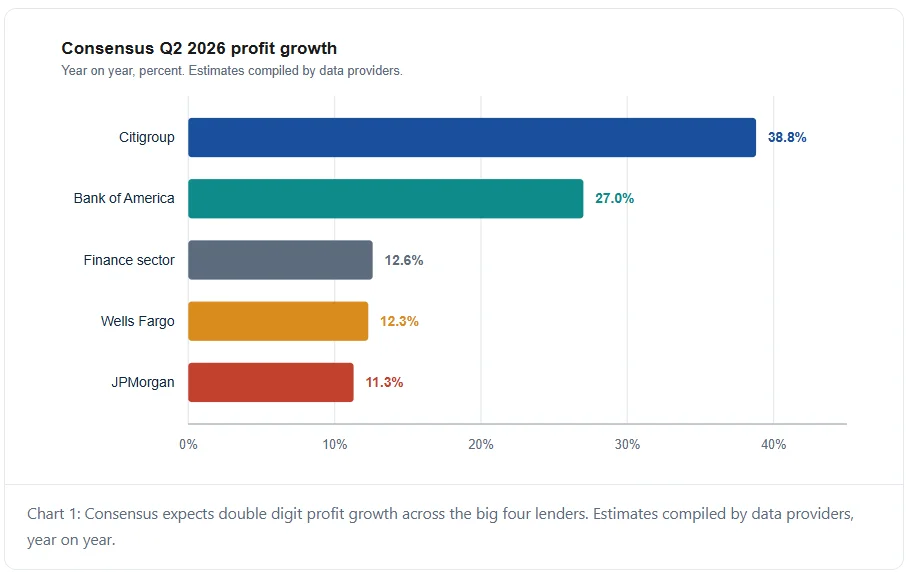

Street forecasts see Citigroup profit up about 39%, with Bank of America near 27%.

Net interest income guidance, not headline profit, will drive the share reaction.

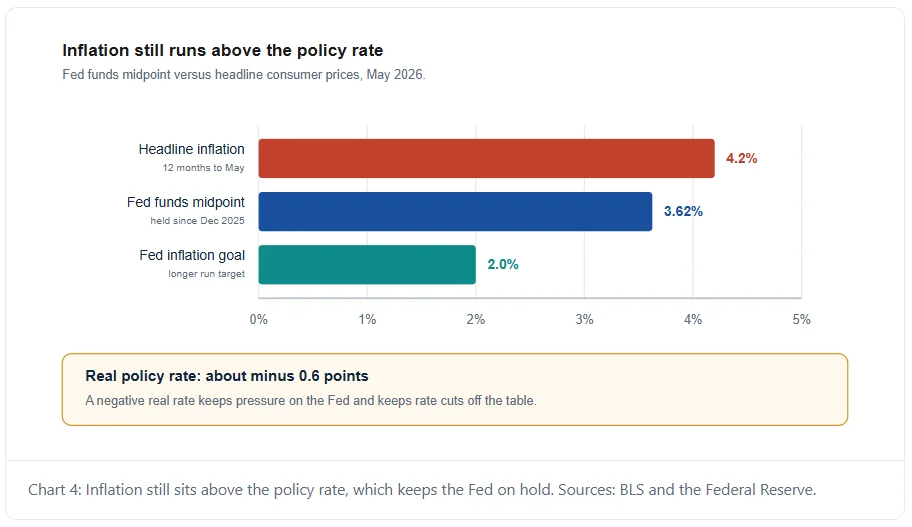

The Fed sits at 3.50% to 3.75%, and futures now lean toward a hike, not a cut.

All 32 banks cleared the June stress test, which frees cash for buybacks.

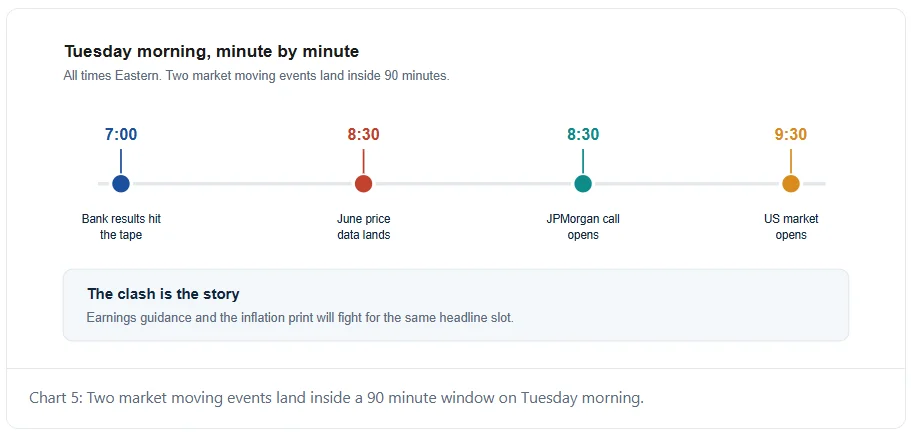

Bank earnings season opens on Tuesday with a crowded tape. JPMorgan Chase, Bank of America, Citigroup and Wells Fargo all report before the US market opens. Goldman Sachs joins them. The largest lender set its release for about 7:00 a.m. Eastern Time, with a call at 8:30 a.m. Yet the Bureau of Labour Statistics drops June price data at exactly 8:30 a.m. So traders must price two very different signals within minutes.

A rare double print

The overlap matters because inflation now drives the bank story. Headline prices rose 4.2% in the year to May. That pace sits well above the Fed’s 2% goal. Also, the Federal Open Market Committee held its target range at 3.50% to 3.75% on June 17. The vote was 12 to 0. Officials then lifted their year-end rate views. Futures markets now lean toward a hike, not a cut. So a hot June print could reprice the whole sector in seconds.

What the numbers should show

Street forecasts point to a strong quarter. Estimates compiled by data providers put JPMorgan’s profit growth near 11% from a year ago. Bank of America should grow about 27%. Citigroup leads the group at nearly 39%, while Wells Fargo trails at nearly 12%. In total, the finance sector profit should climb about 13% on 8% higher revenue.

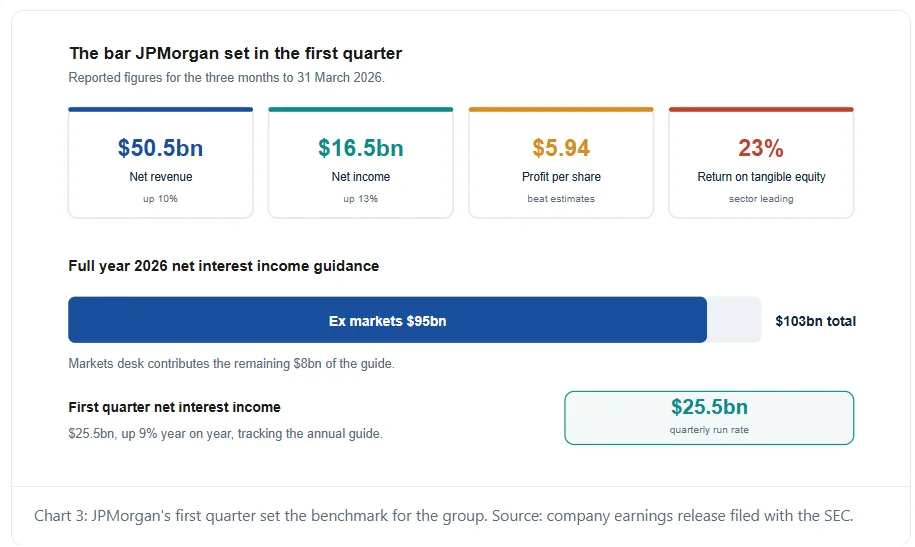

Two engines drive those gains. First, trading and deal fees remained strong throughout the quarter. Second, loan growth held up as shoppers kept spending. The first quarter set a high bar. JPMorgan posted net income of $16.5 billion, revenue of $50.5 billion and profit of $5.94 a share. Net interest income hit $25.5 billion, up 9%. Return on tangible common equity reached 23%.

The one number that moves the stock

Investors will look past the headline profit. Instead, they will hunt for the net interest income guide. In April, the bank cut its full-year view to about $103 billion. Strip out the markets desk, and the figure drops near $95 billion. The stock still fell, even after a fine quarter. Clearly, the market cares more about the forward spread than the trailing profit.

Here, the macro backdrop cuts both ways. A patient Fed keeps deposit costs sticky. But a higher-for-longer path also props up yields on new loans. So any upgrade to that $103 billion figure would land as a real surprise.

Credit and capital look sturdy

Credit gives the bulls their best case. Card write-offs and late payments stay in check. Management still guides to a card loss rate near 3.4%. Also, the June stress test cleared all 32 banks. The Fed modelled 10% joblessness, a 39% slump in office values and a 30% drop in house prices. Even so, group capital fell just 1.6 points and held above every floor.

That result frees cash. So, buybacks and dividend hikes now top the list of investor questions. Capital return, not fear of credit, defines this cycle. Watch for fresh repurchase news alongside the results.

Where the risks hide

Not every line looks clean. Office loans still carry stress, and private credit continues to grow outside banks. Moreover, deposit costs fall slowly once rates plateau. A sharp reserve build would therefore quickly dent the mood. Watch the provision line as closely as the profit line.

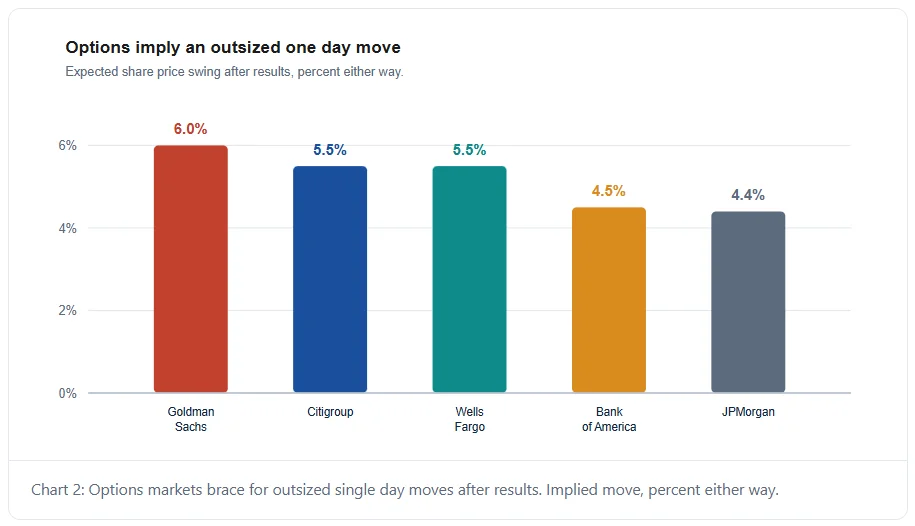

Traders expect fireworks

Options pricing tells its own story. Traders brace for a one-day swing near 6% in Goldman Sachs shares. Citigroup and Wells Fargo screen near 5.5%. Bank of America and JPMorgan sit near 4.5%. Those levels tower over the average move seen after recent reports. In short, the market expects a shock, not a quiet nod.

Valuation raises the stakes too. Bank shares have run hard into the print. Therefore, a mere beat may not be enough. Guidance will decide the tape.

What to watch

Three lines deserve close attention on Tuesday. Watch the net interest income guide, the reserve build and the buyback pace. Above all, watch how bosses frame the rate path. Banks that lean into a higher-for-longer world will guide one way. Those bracing for cuts will guide the other way. Finally, keep one eye on the price data. If inflation runs hot, even a clean quarter may struggle to hold a bid. Bank stocks rarely fight the Fed and win.

One more thing sets the tone. The group kicks off the wider reporting season. Hence, a weak start would sour sentiment far beyond the banks themselves.