June 02, 2026 – Atom Bank has become a fresh takeover target in the UK banking market.

In Summary

Yorkshire Building Society and Leeds Building Society are reportedly considering bids for Atom Bank.

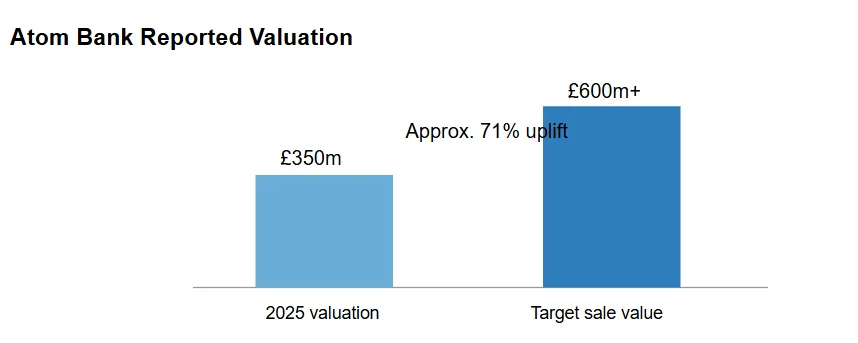

Atom’s owners are said to be seeking more than £600 million.

That would mark a sharp rise from Atom’s reported £350 million valuation last year.

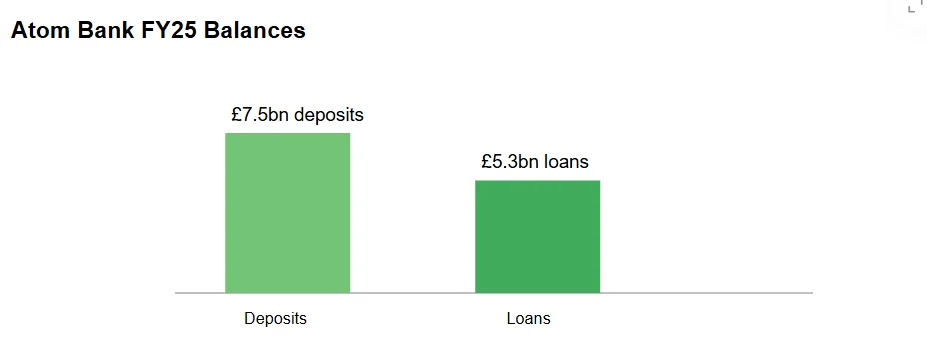

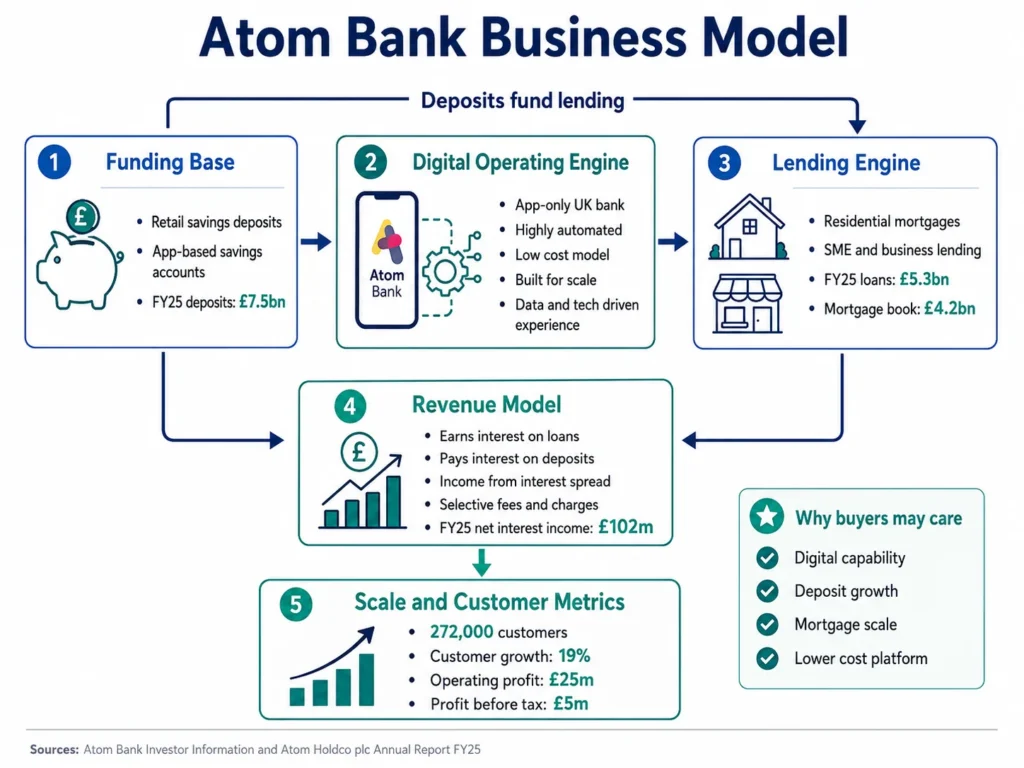

Atom reported £7.5 billion in deposits and £5.3 billion in loans in FY25.

The deal shows how UK mutuals are using acquisitions to fight larger banks.

Two major building societies are reportedly weighing bids for the digital lender. The possible bidders include Yorkshire Building Society and Leeds Building Society, according to a PYMNTS report citing the Financial Times. Atom’s owners have appointed Jefferies to manage the process. They are seeking a valuation above £600 million.

That number matters. Atom was reportedly valued at £350 million during a funding round last year. Therefore, a £600 million sale would imply a valuation uplift of about 71%. It would also mark a major shift from Atom’s earlier IPO ambitions.

The timing is not accidental. UK building societies are under pressure to scale. They face large banks, digital challengers and deposit-hungry fintechs. Acquiring Atom could give a mutual lender instant digital capability.

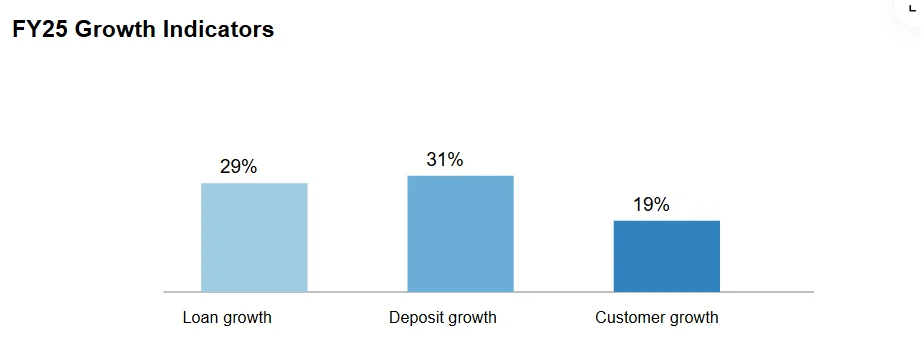

Atom is no longer a small experimental platform. In FY25, the bank reported £7.5 billion in deposits, up 31% from FY24. Its mortgage balances reached £4.2 billion, also up 31%. Customer numbers rose 19% to 272,000.

However, Atom remains smaller than the largest UK fintech banks. PYMNTS noted that Atom trails rivals such as Monzo and Revolut in customer scale. This creates a strategic opening. A mutual buyer could combine Atom’s technology with a larger balance sheet.

Why Building Societies Want Atom

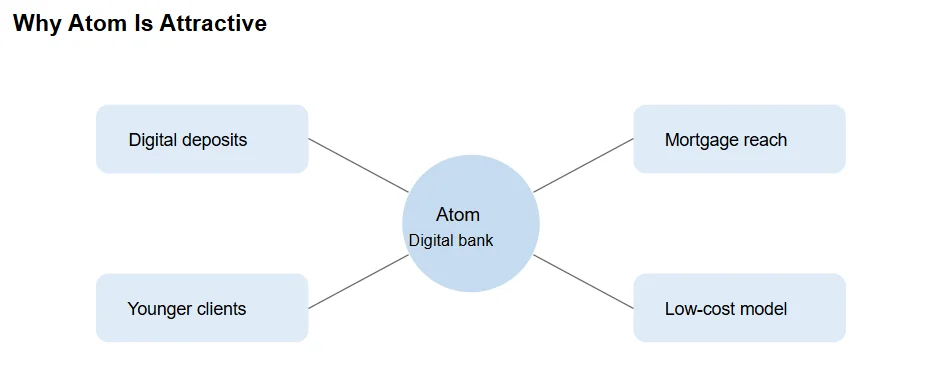

The logic is clear. Building societies need younger customers, faster onboarding and stronger app-based savings products. Atom already offers that infrastructure.

Atom describes its model as simple, automated and low cost. It focuses on retail deposits, residential mortgages and SME lending. The bank says this model supports a lower cost-to-asset ratio than mainstream lenders.

That is attractive for mutuals. Their core strength remains savings and mortgage trust. Yet they often lack the technology profile of digital banks. Atom could close that gap quickly.

The deal would also follow wider consolidation. Nationwide completed its Virgin Money acquisition in 2024. Coventry Building Society also agreed to buy Co-operative Bank for £780 million. PYMNTS cited both deals as part of the sector’s acquisition push.

Atom’s Numbers Strengthen the Case

Atom’s FY25 numbers show real operating momentum.

The bank reported £102 million in net interest income. Operating profit stood at £25 million. Profit before tax was lower at £5 million, down from £7 million in FY24.

That mix sends a balanced message. Atom is growing quickly. However, profitability remains thin. A buyer would be purchasing scale potential, not mature earnings power.

This is why valuation will be sensitive. A price above £600 million would price Atom at around 8% of FY25 deposits. It would also be about 120 times FY25 profit before tax. That looks expensive on earnings. However, it may look reasonable as a digital platform deal.

The Bigger Market Signal

The possible Atom sale signals a deeper shift in UK banking.

Digital banking is no longer a side project. It is becoming core infrastructure. Mutual lenders can no longer rely only on branch trust and mortgage heritage.

At the same time, fintech banks need balance sheet strength. Atom’s sale process shows that technology alone may not be enough. Funding cost, regulatory capital and customer scale still matter.

For Atom’s shareholders, a sale may offer a cleaner exit than an IPO. Public markets remain selective toward fintech listings. Buyers with strategic needs may pay more than public investors.

What Happens Next

The key question is whether bidders meet Atom’s valuation target.

Some industry executives reportedly believe bids may fall below £600 million. That is understandable. Atom has strong deposit growth, but modest profit before tax.

Still, the strategic value is high. A successful acquisition could reshape the mutual banking playbook. It may also push other UK lenders to review digital acquisition targets.

For readers, the takeaway is simple. This is not just a bank sale story. It is a signal that digital banking assets now carry infrastructure value.

If a building society buys Atom, the UK mutual sector could become more competitive. It could also become more digital, faster than expected.