July 13, 2026 – Two billion-dollar deals led US venture last week. But the steep cliff below them shows a market that now backs very few firms.

In Summary

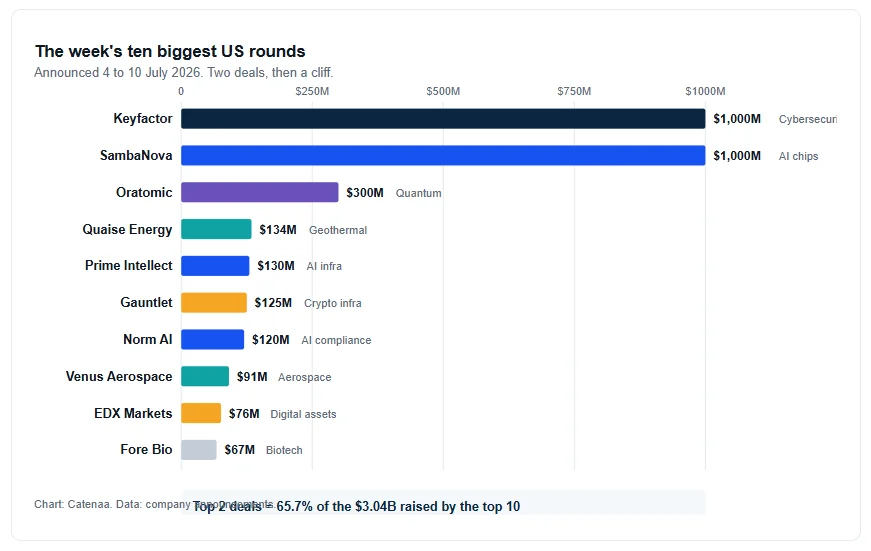

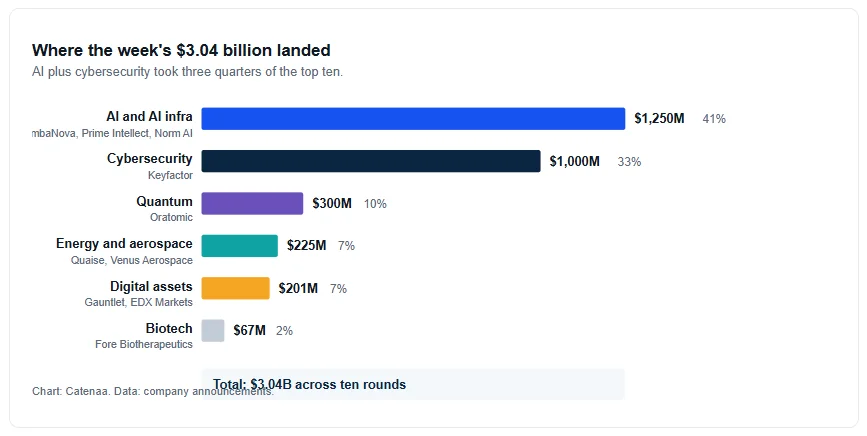

Ten US rounds raised about $3.04 billion between 4 and 10 July 2026.

Keyfactor and SambaNova each took $1 billion, or 65.7% of the weekly total.

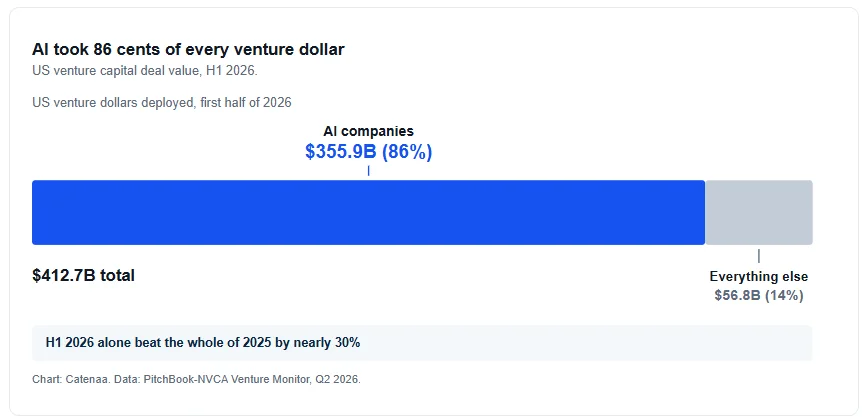

AI absorbed 86% of all US venture dollars in the first half of 2026.

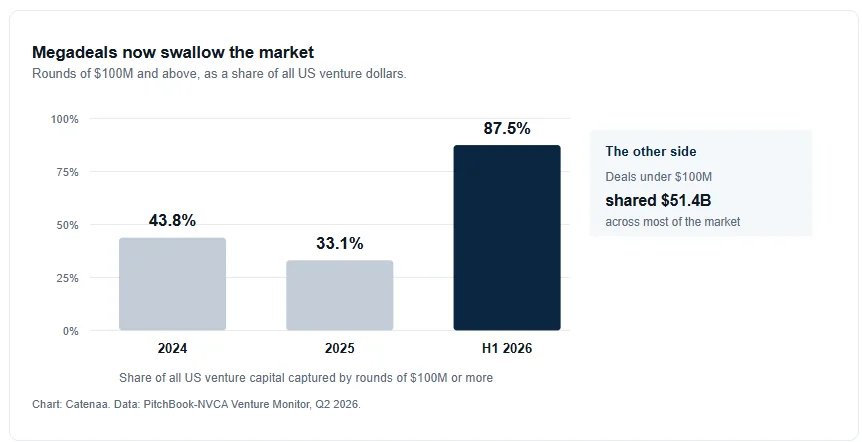

Rounds of $100 million or more captured 87.5% of capital deployed.

AI money now funds chips, training tools and compliance, not just model labs.

Keyfactor and Oratomic sit on opposite sides of the same post-quantum trade.

A Week That Split Into Two Tiers

AI funding rounds now soak up almost every venture dollar in the US. Between July 4 and July 10, the ten largest US rounds raised about $3.04 billion. Yet just two deals took 65.7% of that sum. Keyfactor and SambaNova each landed $1 billion. So the other eight rounds split only $1.04 billion.

The gap tells the real story. Third place went to quantum startup Oratomic at $300 million. So the drop from second to third place exceeded 70%. Below Oratomic, the midpoint deal shrank to about $128 million. In short, the week looked like a barbell rather than a broad market.

This shape is no fluke. National data shows the same skew. US startups raised $412.7 billion in the first half of 2026. The Venture Monitor from PitchBook and the NVCA logged that figure. Also, the total beats all of 2025 by nearly 30%.

But AI firms took $355.9 billion of that pot. So 86 cents in every venture dollar went to one theme. Rounds of $100 million or more took 87.5% of all cash put to work. Everything smaller shared just $51.4 billion. And thousands of firms had to fight over it.

Why AI Funding Rounds Keep Moving Down The Stack

Note where the AI cash lands. It no longer chases model labs alone. SambaNova builds chips that run models. Prime Intellect sells tools to train them. Norm AI turns rules into code. Each firm sits below or beside the frontier model layer.

SambaNova closed the first slice of a $1 billion Series F. That deal prices the chipmaker at $11 billion. General Atlantic led the round. It also named JPMorganChase as a partner for fast, on-site AI. The bank will run SN40 and SN50 systems inside its own walls.

That customer win may matter more than the headline number. Banks rarely move touchy workloads in-house without real belief. Still, the price tag looks steep. SambaNova raised a $350 million Series E just five months back. And in December, talks with Intel put the firm near $1.6 billion. So the new mark sits roughly seven times higher.

Prime Intellect shows the same shift on a smaller scale. This San Francisco startup raised $130 million from Radical Ventures. Venture arms of Nvidia, Intel and Dell all joined. It now claims 6,000 customers. Also, it says sales exceed $100 million per year.

Norm AI makes the same point from a third angle. The New York firm raised $120 million in a Series C led by Khosla Ventures. Its software reads laws and rules, then turns them into checks that code can run. Banks and brokers buy it to police their own staff.

In short, backers pay for picks and shovels now. They no longer pay for one more frontier lab. Chips, training kits, and rule engines all sell into AI budgets. None of them race OpenAI head-on. So the trade looks safer, even at rich prices.

The Quantum Trade Cuts Both Ways

The sharpest link runs between the week’s first and third biggest deals. Keyfactor took more than $1 billion from Summit Partners. The firm guards machine identities and digital keys for over 2,500 clients. Above all, its backers cite one driver. Firms must move to post-quantum crypto.

Oratomic sits on the far side of that same trade. This Caltech spinout left stealth mode only in March 2026. Its work argues that a stable quantum machine needs 10,000 to 20,000 qubits. Older math assumed millions. So the clock on breaking RSA keys speeds up sharply. Vinod Khosla called it his firm’s largest first cheque ever.

In effect, one group paid for the threat. Another group paid for the shield. Both wrote cheques in the same week. Indeed, that mirror explains why cyber won the top slot. Summit expects firms to become quantum-ready before 2030. Keyfactor already serves more than 40% of the Fortune 100. It also won FedRAMP status for US federal work. Scale like that draws growth equity, not classic venture money.

Where The Rest Of The Money Went

Outside AI, cash flowed to slow, hard tech. Quaise Energy took $134 million to drill deep with millimetre waves. Venus Aerospace won $91 million for very fast engines. Both firms face payoffs measured in decades. Still, their backers took that wait.

Digital asset plumbing also drew real cheques. Japan’s SBI Group backed two deals. Gauntlet raised $125 million to model risk in DeFi. EDX Markets raised $76 million to run a crypto venue for big funds. Together, those cheques hit $201 million. Note who wrote them. Strategic Japanese money did not crypto native funds. That shift says a lot. Big balance sheets now buy the rails, while token funds sit out.

Fore Biotherapeutics closed the list with $67.4 million for cancer drugs. Notably, no consumer app firm made the top ten.

What The Squeeze Means Next

Records at the top now hide a slump below. New fund launches are on track for their worst year since 2016. And three firms took 48.1% of all fresh venture cash. So fewer backers now steer far more of the market.

The squeeze bites hardest at the bottom. Deals under $100 million shared just $51.4 billion in the half. That slice fed most of the market by count. Seed founders therefore fight for scraps while megadeals swell.

This setup looks brittle. If AI growth stalls, the pain spreads wide. PitchBook analysts flagged that risk. Yet even a win brings danger. Venture returns follow a power law. So most firms that raise at today’s prices will still let their backers down.

For founders outside AI, the signal reads clearly. Cash still flows to deep tech bets with hard science behind them. Quantum, geothermal and hypersonics all proved that last week. But for everyone else, the door just got much narrower.