June 30, 2026 – A Standard Chartered call and a reported Kraken stake are pushing investors to model a DAO-run lender with bank-style tools.

In Summary

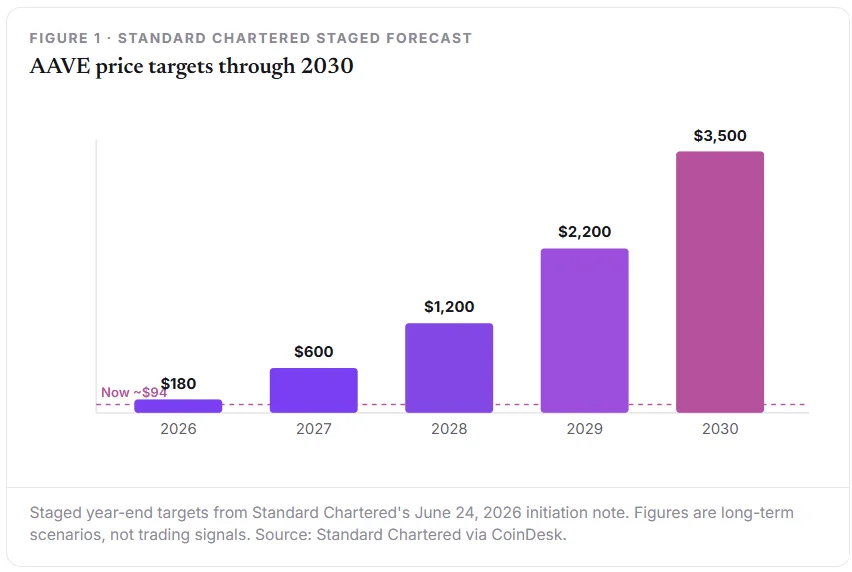

AAVE climbed about 13% to near $94 as a Standard Chartered note set a $3,500 target for 2030.

Investors now weigh Aave like a bank, judging deposits, fee capture, and capital returns.

The open question is how much protocol revenue reaches the DAO after partner cuts and incentives.

Aave’s rally has turned into a debate about value. Investors keep circling one question. Can a decentralized lender be judged like a bank?

AAVE climbed roughly 13% to near $94 in late June. The move tracked a bullish note from Standard Chartered. Analyst Geoff Kendrick set a long-range target of $3,500 by 2030, according to CoinDesk. That figure implies about a 50x gain from current levels. Moreover, he described Aave as an automated, on-chain bank that runs without staff.

Kendrick maps a staged climb rather than a single leap. His path runs through $180 this year, then $600, $1,200, and $2,200, before reaching $3,500. A jump to that level would lift AAVE’s market value from near $1.3 billion toward $50 billion. Clearly, the bull case leans heavily on tokenized assets reaching DeFi at scale.

Why does bank math now fit Aave

Aave already operates at a scale that outside capital can read. The protocol remains the largest decentralized lender. DefiLlama tracks billions in value locked and more than $2.2 billion in lifetime fees. Therefore, traditional valuation tools suddenly feel relevant here.

At its October 2025 peak, Aave held about $75 billion in deposits. That level would have ranked it among the 30 largest U.S. banks. The protocol now earns roughly $134 million in annualized revenue, and all of it flows to the DAO.

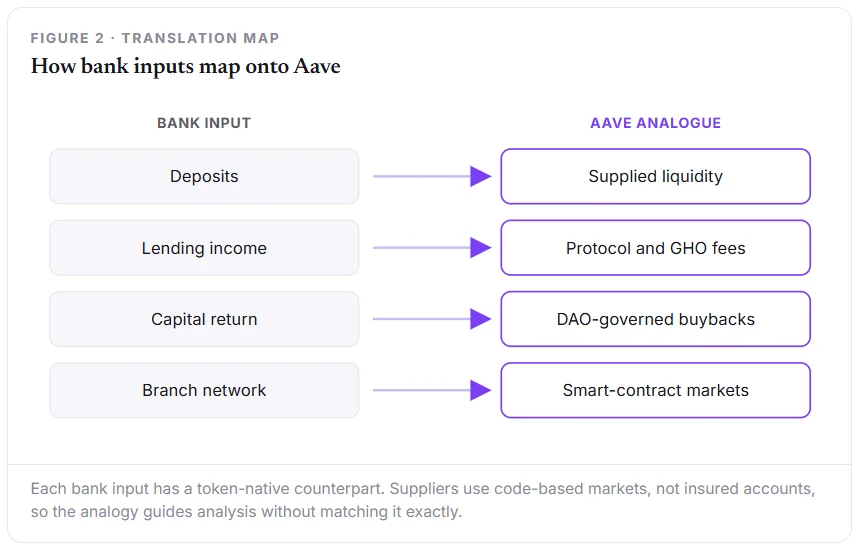

Banks are judged on familiar inputs. These include deposits, borrower demand, fee capture, and capital returns. Aave offers a crypto-native version of each one. However, every comparison carries a caveat.

Suppliers use code-based markets rather than insured bank accounts. In addition, gross protocol activity differs from net revenue. As a result, investors must interpret the headline numbers before trusting them.

The shock that still shapes the debate

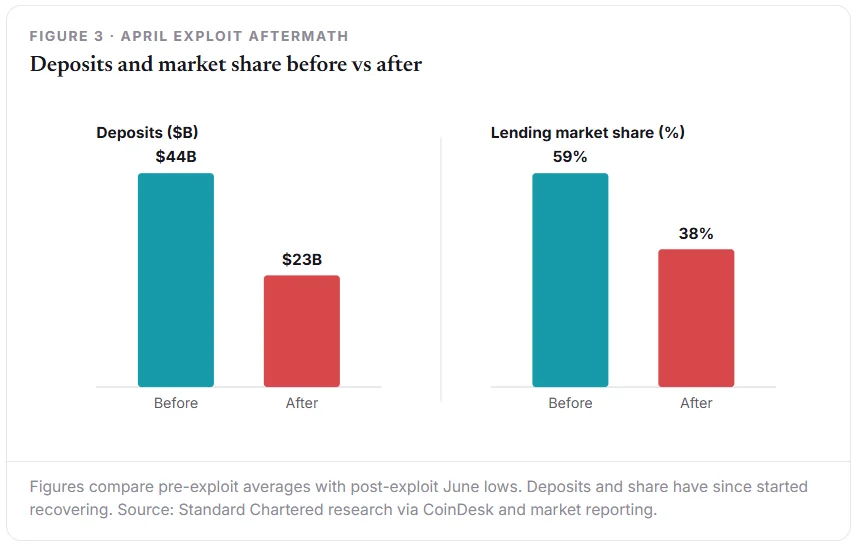

Aave’s 2026 has not been smooth. In April, attackers exploited KelpDAO’s cross-chain bridge. They minted about $292 million in unbacked rsETH. Then they used those tokens as collateral to borrow real assets.

Aave’s own smart contracts stayed intact. Still, the fallout proved severe. Deposits fell from roughly $44 billion to about $23 billion. Meanwhile, Aave’s share of the lending market slid from 59% to 38%. Standard Chartered now treats those June lows as a floor.

Confidence has begun to rebuild since then. The new Aave V4 release has drawn fresh capital. Its deposits passed $200 million within three months of launch. Active loans there have also climbed above $56 million.

A reported Kraken stake sharpens the question

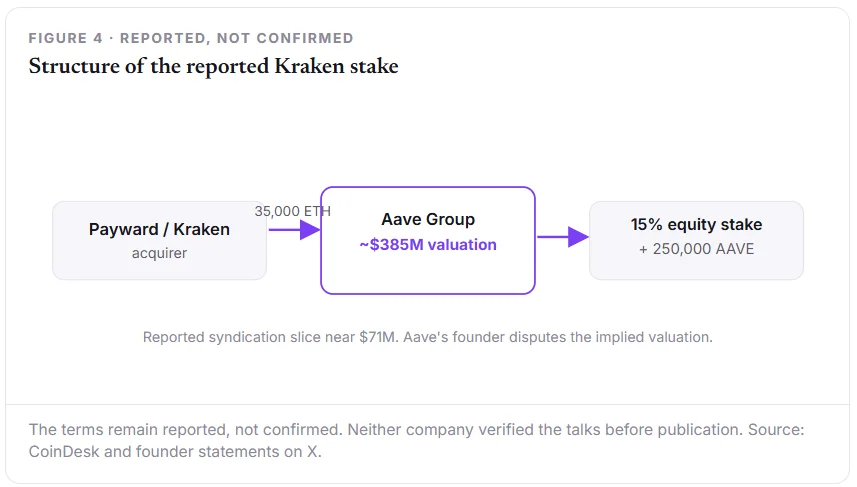

Strategic interest has added another layer. CoinDesk reported that Kraken’s parent, Payward, is in talks for a 15% stake in Aave Group. The proposed deal values that entity near $385 million. Under the reported terms, Kraken would send 35,000 ETH for 250,000 AAVE tokens plus equity, per CoinDesk.

Founder Stani Kulechov pushed back quickly. He rejected any sale of AAVE at a steep discount. He made his case in a post on X. All protocol and GHO revenue flows to the AAVE token under the Aave Will Win framework. He also cited steady revenue as proof of strength. Notably, neither company confirmed the talks before publication. So buyers cannot simply treat AAVE as ordinary corporate equity.

Horizon turns the test toward institutions

Horizon makes the institutional case concrete. The permissioned market lets regulated firms borrow against tokenized assets. Aave reported that Horizon passed $450 million in net deposits and about $135 million in borrowing after VanEck’s fund joined. Consequently, the protocol looks increasingly legible to asset managers.

Yet Horizon is one product, not the entire protocol. Its economics still depend on partner terms and DAO governance. So the bank analogy stays useful but incomplete.

What investors should watch next

The next signal is governance quality, not just price. Institutional capital tends to reward clear cash flows and stable rules. If Aave keeps revenue, buybacks, and partnerships coherent, the bank comparison could hold. If that balance slips, the same analogy becomes a ceiling instead of a green light.