July 10, 2026 – A leading bond investor warns the long bond still looks vulnerable as the term premium climbs and deficits stay wide.

In Summary

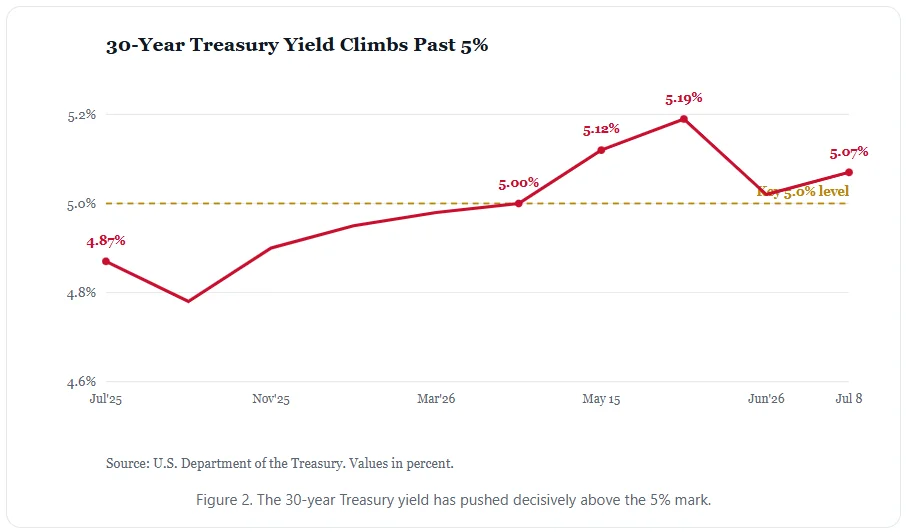

The 30-year Treasury yield closed near 5.07%, among its highest levels since 2007.

PGIM’s Gregory Peters remains underweight on long bonds and expects the term premium to continue rising.

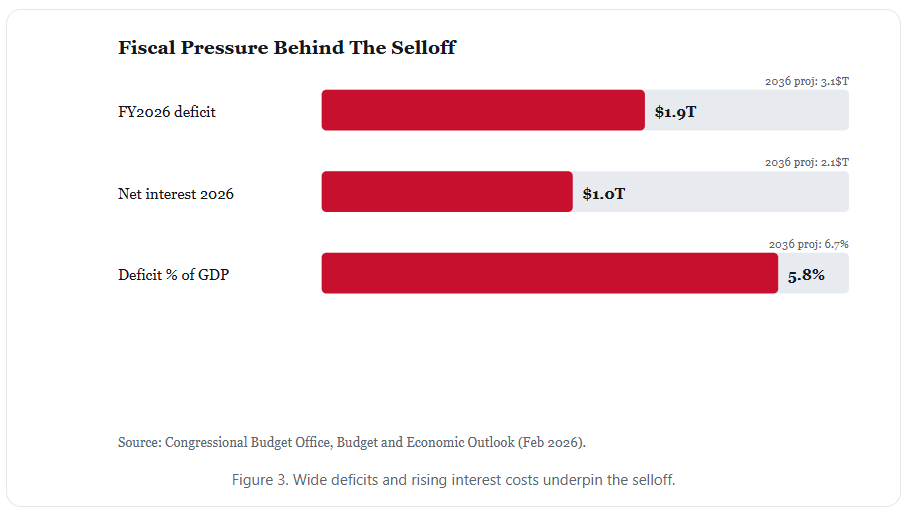

A $1.9 trillion federal deficit and heavy issuance continue to put upward pressure on long yields.

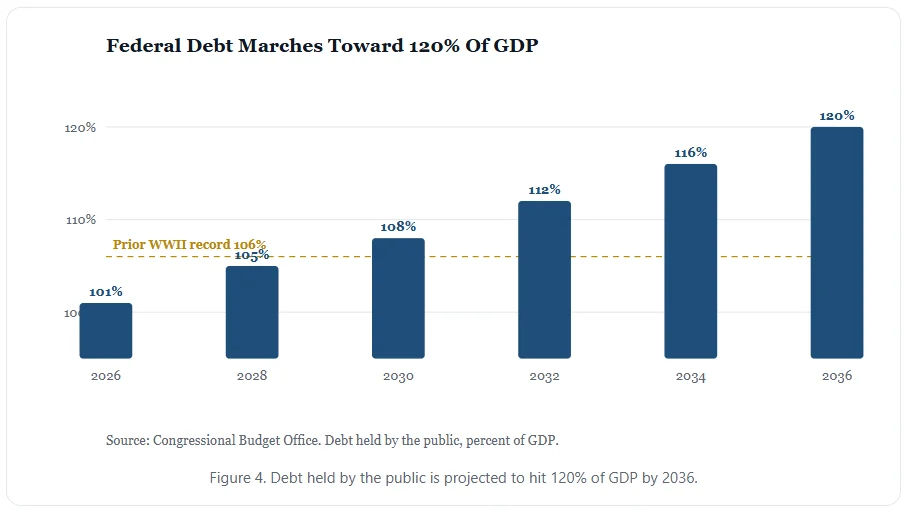

Debt held by the public is on track to reach 120% of GDP by 2036.

The repricing of the 30-year Treasury yield has only just begun, and one top bond investor sees more to come. Gregory Peters, co-chief investment officer at PGIM Fixed Income, argues that the long bond still looks weak. Moreover, he stays underweight on 30-year Treasuries despite their high coupons.

His view matters because the long end of the curve now sits near multi-decade highs. Indeed, the 30-year yield closed at 5.07% on July 8, 2026, based on U.S. Treasury data. Furthermore, that level ranks among the highest marks since 2007. In short, the long bond has entered a new regime.

Why the term premium keeps climbing

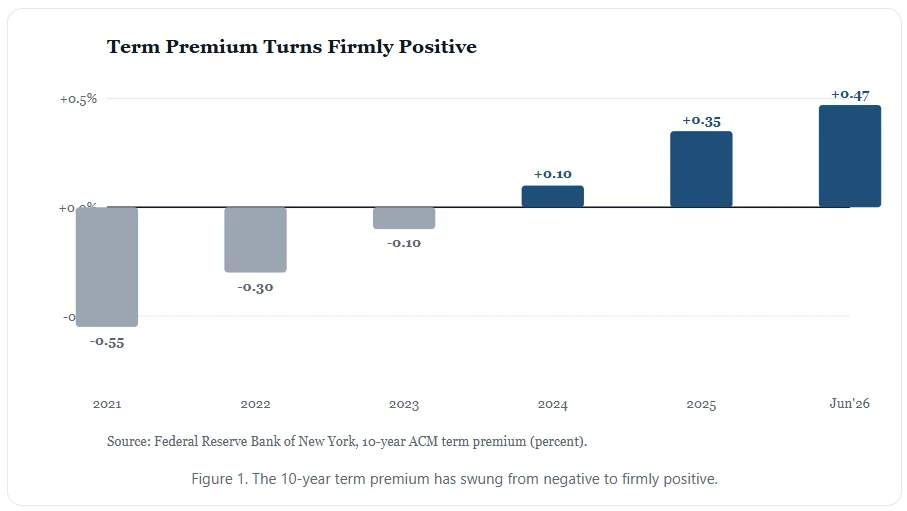

The story is not really about Federal Reserve rate cuts. Instead, it centers on the term premium. That premium is the extra pay investors want for holding long-dated debt. For years, it sat near zero or below. However, the picture has changed sharply in 2026.

The New York Fed puts the 10-year term premium near 0.47% as of late June. Consequently, the gauge has turned firmly positive for the first time in years. Therefore, softer rate-cut bets no longer pull long yields lower on their own. In other words, the old playbook no longer works cleanly.

Peters expects this premium to keep rising. As a result, he prefers to wait rather than add duration risk today. Additionally, he has called the global bond market chaotic and confidence fragile. In short, he wants more reward before he commits.

Fiscal pressure lifts the 30-year Treasury yield

Supply sits at the heart of the worry. The Congressional Budget Office projects a federal deficit of $1.9 trillion for fiscal 2026. Notably, that figure equals 5.8% of gross domestic product. Meanwhile, it far exceeds the 50-year average deficit of nearly 3.8% of GDP.

Net interest costs now total about $1.0 trillion this year alone. Because debt keeps rising, those costs climb further each year. In fact, the CBO expects public debt to reach 120% of GDP by 2036. Currently, that ratio sits near 101%.

Larger deficits mean heavier Treasury issuance. Subsequently, more long-dated paper hits the market, and buyers demand better terms. Thus, the term premium rises as supply outpaces steady demand. Over time, that gap can widen the whole curve.

A shifting buyer base

Demand trends also matter for the long bond. Traditional foreign buyers once took in Treasuries regardless of short-term price swings. However, that stable base has thinned over the past decade. As a result, the market now leans on more price-sensitive hands.

Financial hubs now hold a larger share of foreign Treasury stakes. These holders often trade far more than official reserve managers. Therefore, they react quickly to price and yield moves. Meanwhile, domestic buyers must absorb more of the supply.

Structural forces add to the shift. For example, aging pension funds see funding ratios improve when yields climb. Consequently, they feel less need to buy extra-long bonds. Besides, sticky inflation keeps hopes for real yields high. Together, these forces reduce natural demand for duration.

What it means for investors

The core question is not whether yields look high. Rather, it is whether they look high enough to pay for the risk. Peters clearly leans toward caution for now. Still, he admits the yields tempt him.

Higher long yields ripple across the wider economy. For instance, mortgage rates and business borrowing costs track the long bond closely. Accordingly, a lasting repricing would lift financing costs for homes and firms alike. In turn, that shift could slow growth.

Some investors view current yields as a real chance. After all, a 5% coupon offers solid income after years of thin returns. Nevertheless, the timing question stays tricky while the premium keeps building. Because of that risk, many prefer shorter maturities today.

History also urges care at these levels. Previously, sharp jumps in long yields often came before market strain. Therefore, seasoned investors watch the 5% mark with real caution. Yet a clear inflation cooldown could still shift the mood fast.

What could turn the tide

Several triggers could still cap the long bond. First, a firm drop in inflation would ease the pressure. Second, calmer energy prices would also help sentiment. Third, softer growth could revive bets on deeper rate cuts.

Fiscal signals also carry weight for the market. For example, each quarterly refunding plan reveals the size of the fresh issuance. Consequently, a tilt toward more long-dated bonds would raise the pressure. By contrast, a smaller long-end share would ease it.

Still, none of these shifts look certain today. Because inflation stays sticky, the near-term path favors higher yields. Moreover, wide deficits keep the supply story firmly in place. As such, Peters sees little reason to chase the long bond yet.

For now, the long end stays firmly in focus. If deficits remain wide and inflation remains sticky, the pressure is likely to hold. Ultimately, Peters suggests the repricing story still has room to run. Above all, patience may reward those who wait.