May 14, 2026 – A $25 billion Treasury auction cleared at 5.046% on May 13, 2026. Surging energy costs and persistent inflation expectations are rewriting the rate outlook.

In Summary

The 30-year Treasury yield cleared 5% for the first time since 2007.

A $25 billion May 13 auction priced at 5.046%, above pre-auction levels.

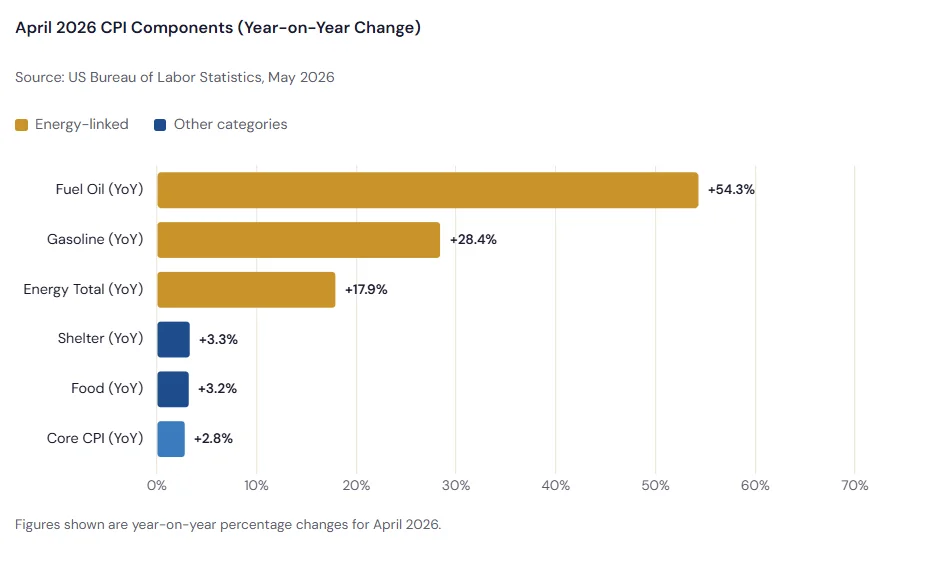

April CPI rose 3.8% year-on-year, the highest since May 2023.

Energy costs surged 17.9% annually, with gasoline up 28.4%.

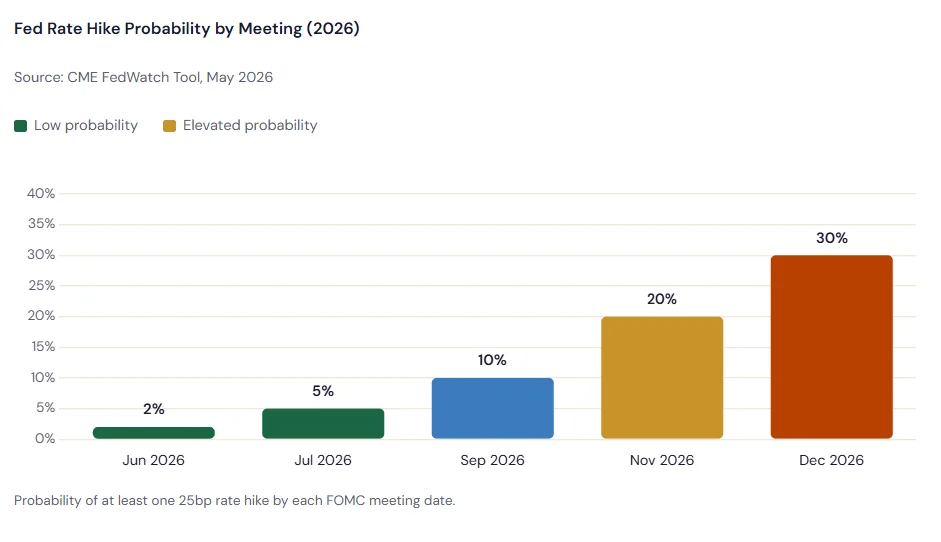

Markets now price a 30% probability of a Fed rate hike by December 2026.

The US 30-year Treasury bond crossed a landmark threshold on Wednesday, May 13. Investors locked in a yield of 5.046% at a $25 billion government bond auction. Bloomberg reported it was the first time since 2007 that the long bond yielded 5% or more.

The auction cleared slightly above pre-auction trading levels. That gap signals subdued investor demand. It reflects a bond market adjusting to a new inflation reality shaped by surging energy prices.

What Is Pushing Yields Higher?

Energy is the primary driver. The US Consumer Price Index rose 3.8% year-on-year in April 2026. That reading was the highest since May 2023, according to the Bureau of Labor Statistics.

Energy costs surged 17.9% annually in April. Gasoline prices climbed 28.4% over the same period. Energy components alone accounted for more than 40% of the monthly headline gain.

Oil is trading above $100 per barrel. The national average gasoline price stands at $4.50 per gallon. Both reflect the market impact of the ongoing US-Iran conflict.

Core CPI, which excludes food and energy, rose 2.8% annually in April. The monthly core reading of 0.4% was the highest since January 2025. That figure still runs well above the Fed’s 2% target.

The Federal Reserve Is in a Difficult Position

The Federal Reserve held its benchmark rate at 3.5% to 3.75% at its most recent meeting. Three board members dissented. They opposed any continued signal toward further rate cuts.

Kevin Warsh, newly confirmed as Fed chair, previously advocated for lower rates. That stance is now harder to maintain. Inflation has moved in the wrong direction for two consecutive months, according to CNBC.

Markets are repricing the rate outlook quickly. CME FedWatch data shows traders now price a 30% chance of a rate hike by December 2026. Just weeks ago, rate cuts were the consensus across the broad market.

“Inflation is heading in the wrong direction.”

“It is very unlikely the Fed can lower rates any time soon.”

-Chris Zaccarelli, Chief Investment Officer, Northlight Asset Management

What the 5% Threshold Means for Markets

The 5% level on the 30-year bond carries significant historical weight. Each prior approach to this threshold triggered tighter financial conditions. Equity valuations fell, credit spreads widened, and rate-sensitive sectors underperformed.

The October 2023 episode offers the clearest comparison. The 30-year yield climbed above 5.1% on a “higher for longer” policy outlook. The S&P 500 fell sharply over a brief period before recovering.

Deutsche Bank strategist Steven Zeng has noted the current 5% yield could attract pension funds and long-duration investors. Sustained institutional interest, however, depends on how the Fed responds to incoming inflation data.

Auction Demand Was Tepid

Demand at the May 13 auction was described as middling. Auctions earlier in the same refunding cycle, for 3-year and 10-year notes, also fell short of expectations.

When demand falls short, the Treasury must offer higher yields to sell its bonds. That creates a compounding effect on borrowing costs. The cycle can put further upward pressure on already-elevated yields.

The US Treasury has committed to keeping auction sizes unchanged for at least the next several quarters, per its quarterly refunding statement. However, with fiscal-deficit pressures mounting, analysts expect official guidance to shift by year-end.

The Inflation Timeline Ahead

Energy prices remain the key swing factor. A resolution of the Iran conflict could bring inflation down rapidly. The US is the world’s largest oil producer, which helps cushion supply shocks.

Cleveland Fed president Beth Hammack has described 2026 as the fourth major shock in five years. She cited the pandemic, the Russia-Ukraine war, tariffs, and now Iran. That sequence is eroding confidence in any “transitory” inflation narrative.

The Fed’s preferred inflation gauge, the PCE price index, stood at 3.5% over the 12 months through March 2026, per the US Treasury’s TBAC economic statement. That is 1.5 percentage points above the 2% target.

Real wages are also under pressure. Average hourly wages slipped 0.5% in April on an inflation-adjusted basis. That drag on consumer purchasing power could slow spending in the months ahead.

What This Means for Investors

For bond investors, 5% on the long bond is historically attractive. The key question is whether yields hold at this level or push higher.

For equity investors, the calculus is more complex. Higher-for-longer rates compress valuations. They also raise the cost of capital for growth-dependent companies.

For the broader economy, the critical risk is elevated rates meeting weakening consumer demand. That combination has historically preceded sharper economic slowdowns. The bond market is now clearly pricing that scenario as a meaningful possibility.