June 27, 2026 – A record AI buildout is colliding with a shrinking cash pile, and investors are no longer giving Oracle the benefit of the doubt.

In Summary

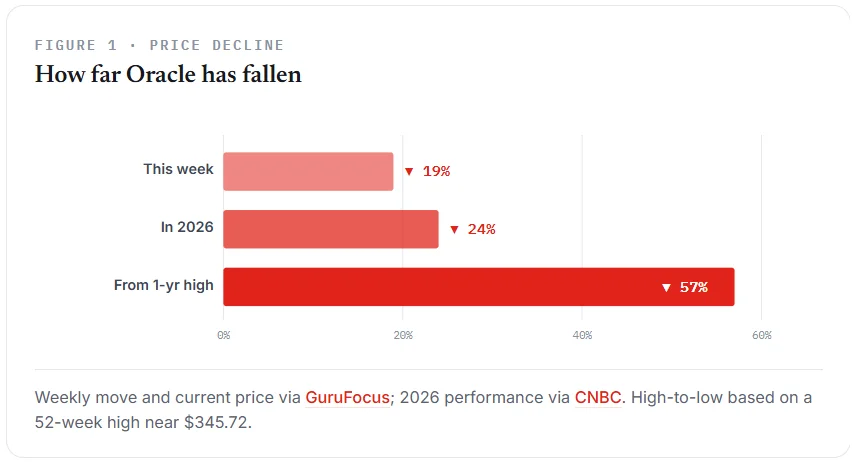

Oracle shares fell about 19% this week, the worst run since 2001.

The stock has dropped roughly 24% in 2026 and over 57% from its high.

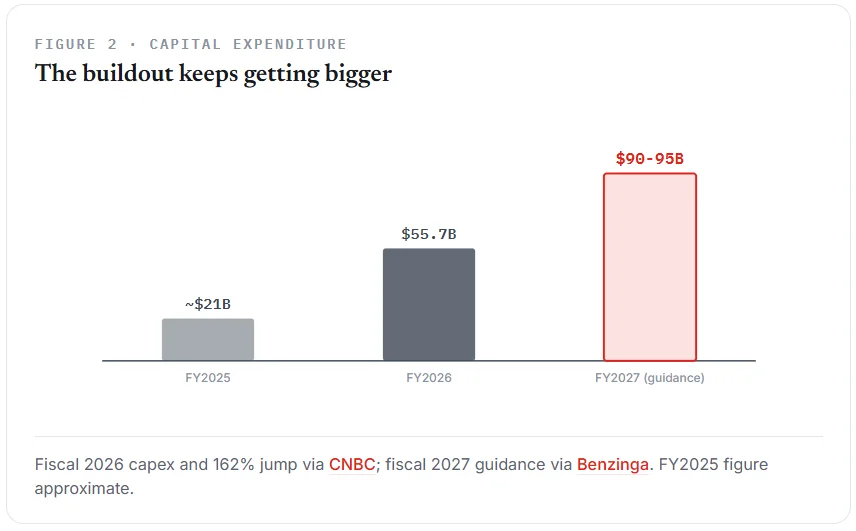

Heavy AI spending lifted capital expenditure 162% to nearly $56 billion.

Oracle posted a negative free cash flow of almost $24 billion.

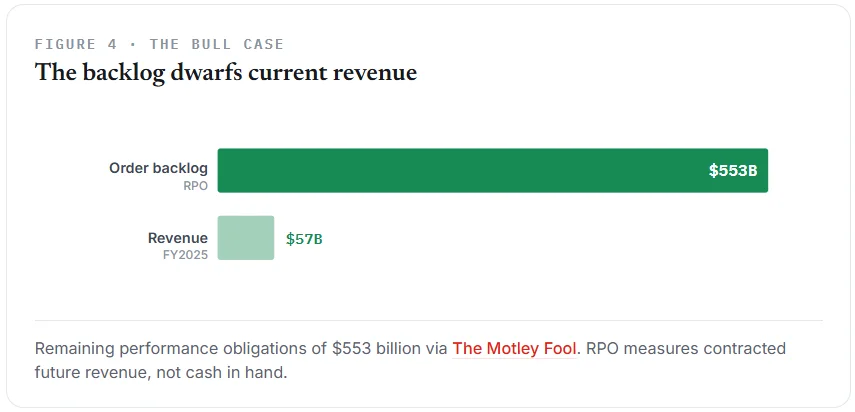

A record $553 billion order backlog still anchors the bull case.

Oracle just suffered a brutal stretch on Wall Street. The software giant ended its worst week since 2001. Investors fixed firmly on its strained finances. Shares slid about 19% across the week. Moreover, the stock has now dropped roughly 24% in 2026. The selloff signals deeper unease about Oracle’s costly bet on artificial intelligence. Increasingly, investors question how the company will fund its huge data-center buildout.

A stock under heavy pressure

Oracle’s slide stands out even in a weak software market. The iShares Expanded Tech-Software ETF has fallen about 16% in 2026. However, Oracle has dropped further, down around 24% this year. The pain also follows a euphoric run. In May, the stock surged about 40%, its best month since 2000. Since then, sentiment has flipped hard.

A broader fear weighs on the whole sector, too. Investors worry that AI models could replace many software products. Consequently, this anxiety has pressured software peers all year. The damage looks even starker over a longer window. Shares peaked near $346 within the past year. Now the price sits below $150. Therefore, Oracle has shed more than half its value from that high.

Such a move rarely hits a megacap. Oracle has fallen 25% or more in a single month only ten times since its 1986 listing.

AI spending drains the cash pile

At the core of the worry sits Oracle’s enormous spending. Capital expenditure jumped 162% to nearly $56 billion in fiscal 2026. Furthermore, that total blew past the Company’s own $50 billion guidance. This buildout mainly serves cloud customers such as OpenAI. Yet the bill now strains Oracle’s balance sheet.

The company posted a negative free cash flow of almost $24 billion last year. Consequently, many investors expect even more borrowing ahead. Management has guided fiscal 2027 capex to $90-$95 billion. As a result, the spending story shows no sign of slowing soon.

Debt and financing take center stage

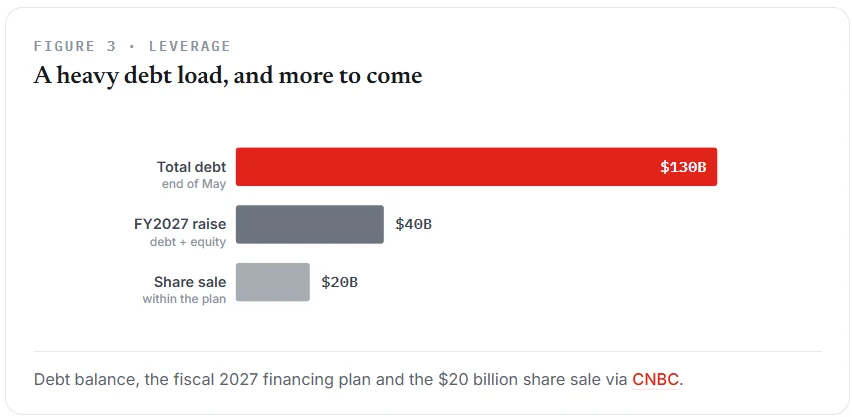

Oracle carried about $130 billion in debt at the end of May. To fund further growth, it plans to raise roughly $40 billion in fiscal 2027. This sum includes a $20 billion share sale announced earlier. The company already leaned hard on capital markets last year. It sold $43 billion in debt and issued $5 billion in equity. As a result, financing has become the central debate among shareholders.

“We expect financing and the pace of equity issuance to remain the central investor debate,” Evercore analysts wrote. Notably, those same analysts still recommend buying the stock.

Leadership and workforce in transition

Oracle is also reshaping its workforce during the turmoil. Headcount shrank 13% to 141,000 employees in fiscal 2026. Additionally, the company pulled back sharply on sales and marketing. The latest earnings call drew unusual attention, too. Co-founder Larry Ellison skipped the event entirely. Instead, dual chief executives Clay Magouyrk and Mike Sicilia answered questions. New finance chief Hilary Maxson joined them on the call.

Ellison’s absence carried clear symbolic weight. Because the stock retreated, his personal wealth ranking slipped. Several peers, including Jeff Bezos and Michael Dell, have now passed him.

The bull case has not disappeared

Still, many analysts read the selloff as a repricing rather than a collapse. Oracle’s remaining performance obligations reached $553 billion in a recent quarter. This backlog reflects future revenue under signed, non-cancelable contracts. For context, that figure dwarfs the roughly $57 billion in revenue Oracle booked in fiscal 2025.

Strong demand for AI cloud capacity underpins the optimism. Therefore, bulls argue the long-term growth story stays intact. Several banks still model a large rebound over the next year. Some even view the drop as a buying opportunity.

What investors should watch next

Oracle now faces a clear test of execution. It must convert that backlog into real cash flow. Meanwhile, it has to manage a heavy and growing debt load. Investors will scrutinize the next earnings report closely.

History offers a mixed but instructive guide here. After similar monthly crashes, the median result was a modest gain within a month. Two-thirds of those signals finished higher. However, a few painful exceptions dragged down the average. Still, sharp near-term swings remain likely. For now, Oracle’s finances will continue to drive the story.