June 07, 2026 – Morgan Stanley raises its price target to $825, betting that four emerging AI products will transform the social media giant into a tech winner.

In Summary

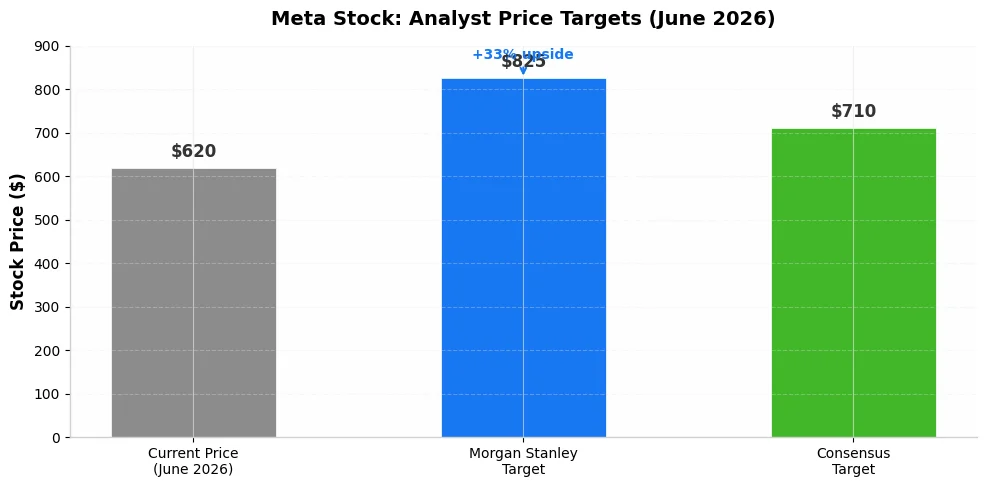

Morgan Stanley raised Meta’s price target to $825, implying 33% upside from current levels.

Meta’s quarterly ad revenue may surpass Google Search for the first time in Q2 2026.

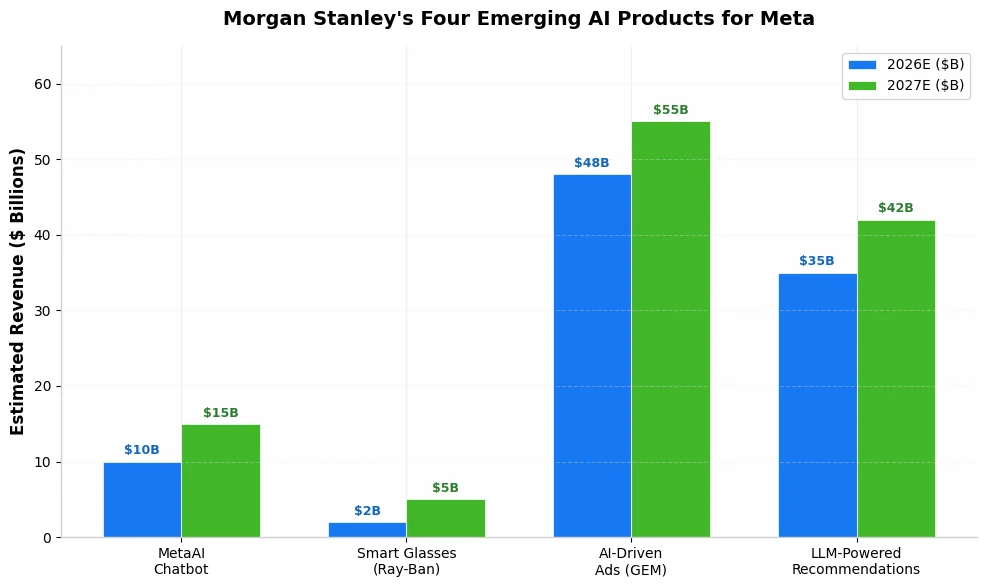

Four emerging AI products drive the bank’s bullish investment thesis.

MetaAI chatbot could generate $10 billion in annual revenue by 2027.

Capital expenditure guidance for 2026 reaches $115 to $135 billion.

Analysts Turn Bullish on Meta’s AI Strategy

Morgan Stanley has named Meta Platforms a “top pick” for investors. The investment bank raised its price target to $825 per share. This new target implies roughly 33% upside from current trading levels. Analyst Brian Nowak leads the coverage team. He believes Meta’s AI transformation remains undervalued by the market. The stock has climbed 10% year-to-date in 2026. However, Morgan Stanley sees further gains ahead. The bank expects AI monetization to drive the next growth phase.

Wall Street has taken notice of Meta’s AI pivot. Multiple analysts now rate the stock as overweight. Previously, the rally focused on cost-cutting measures. Meta declared 2023 its “Year of Efficiency.” Management slashed headcount and streamlined operations. Now the growth logic shifts toward AI returns. Morgan Stanley calls this a qualitative leap. The bank predicts return on invested capital will improve significantly. This improvement stems from core AI product launches.

The Four Products Powering Meta’s AI Future

Morgan Stanley identified four emerging products that could transform Meta into an AI winner. First, the MetaAI chatbot stands out as a major revenue opportunity. Analysts project this product could generate $10 billion in annual revenue. Second, smart glasses and wearable devices expand Meta’s hardware footprint. Wearables represent a new computing platform for Meta. The company has already shipped millions of Ray-Ban units. Third, AI-driven advertising through the GEM ranking model improves click rates. Facebook ad clicks rose 3.5% after this deployment. Instagram conversion rates also improved by more than 1%. Fourth, large language models now rewrite Meta’s recommendation system. This overhaul could boost engagement across all platforms.

Mark Zuckerberg recently described the current system as “primitive.” He made this comment during the latest earnings call. Despite this label, Reels viewing time surged over 30% year-over-year. The new LLM-powered architecture will better understand user goals. It will also analyze context and interests more efficiently. Consequently, advertisers gain better targeting capabilities. Users enjoy more relevant content feeds.

Ad Revenue Set to Surpass Google Search

Meta’s advertising business may reach a historic milestone in 2026. Morgan Stanley predicts Meta’s quarterly ad revenue will surpass Google Search in Q2. Google has long dominated digital advertising markets. Meta achieved 34% to 35% growth when reaching $57 billion quarterly scale. Google only managed 15% growth at that same level. This comparison highlights Meta’s superior AI-driven efficiency. Advertisers increasingly prefer Meta’s AI-powered targeting tools. These tools deliver better returns than traditional search ads.

Furthermore, Instagram Reels viewing time jumped over 30% year-over-year. Facebook feed views also climbed 7% in Q4. These engagement gains directly support higher ad pricing. Meta expanded its GEM ad-ranking model to all Reels. The company also doubled GPU training resources. Therefore, conversion rates continue climbing across platforms.

Massive Infrastructure Spending Builds a Moat

Meta plans to invest heavily in AI infrastructure this year. The company issued 2026 capital expenditure guidance of $115 to $135 billion. This spending covers data centers, chips, and power infrastructure. Power constraints pose the biggest challenge for data centers. Meta secures energy deals to support its expansion plans. Morgan Stanley advised Meta on a $27 billion structured joint venture. This deal supports a U.S. AI data-center campus. Additionally, Meta uses chips from NVIDIA, AMD, and its own MTIA designs. The Andromeda architecture runs across multiple chips. Consequently, Meta builds an insurmountable AI moat.

Some investors worry about high spending levels. However, demand currently grows faster than supply. Meta explicitly stated that capacity bottlenecks still exist. Revenue growth should outpace these investment costs. Morgan Stanley models show infrastructure spending rising $36 billion. This increase drives about 75% of operating expense growth. Nevertheless, the bank considers this spending necessary. It sustains long-term growth and competitive positioning.

AI CapEx sits at the center of the U.S. economic outlook. Global real GDP growth should reach 3.2% in 2026. This investment supports the expansion. Therefore, Meta’s infrastructure bet aligns with macro trends.

Financial Performance Supports the Bull Case

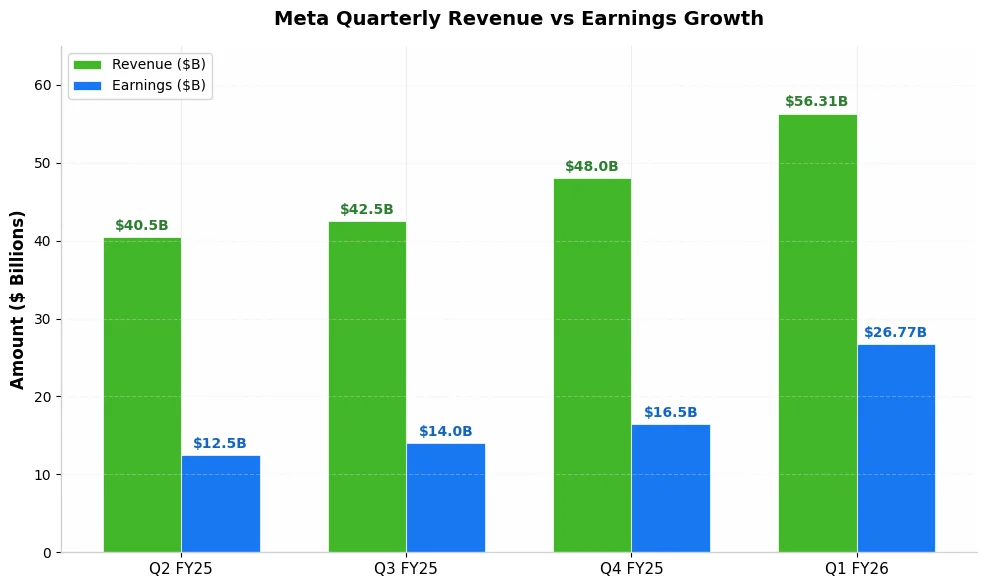

Meta recently reported strong quarterly earnings. Revenue reached $56.31 billion in Q1 2026. Earnings per share also beat analyst expectations. The company raised its 2027 EPS forecast by 10%. Free cash flow generation remains robust and growing. The balance sheet easily supports this aggressive investment cycle. AI coding tools now boost engineer productivity by 30%. Some advanced users report output surging 80%. Therefore, Meta efficiently converts computing power into tangible profits.

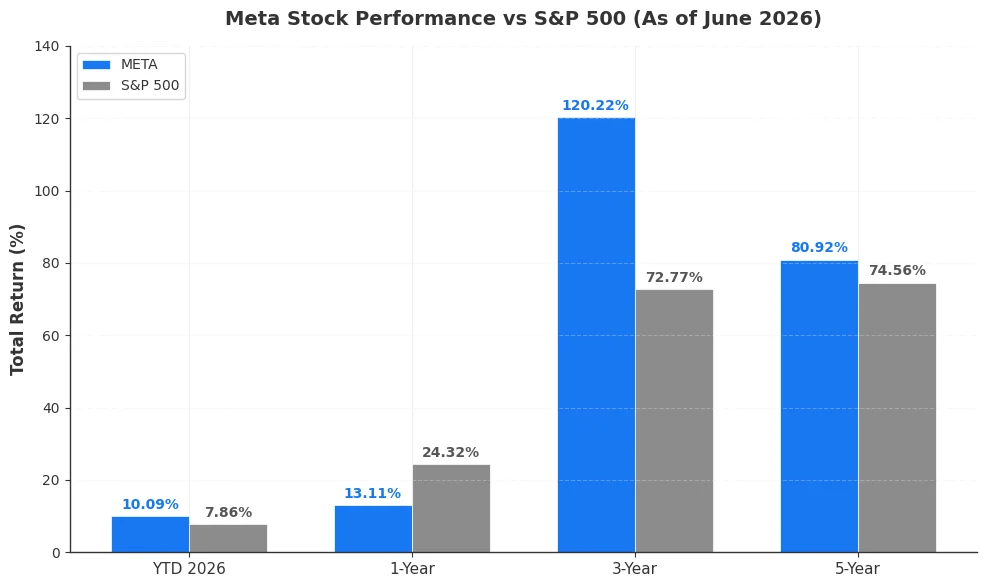

Meta’s three-year return stands at 120%. This performance far exceeds the S&P 500’s 73% gain. The stock currently trades around $620. Therefore, significant upside remains if targets are hit.

Conclusion

Meta Platforms emerges as a clear AI winner in 2026. Morgan Stanley’s $825 price target reflects strong conviction. Four emerging products support this bullish thesis. Investors should watch ad revenue trends closely. The AI transformation is just beginning. Long-term investors may find current entry points attractive. The convergence of AI and social media creates value. Meta’s shift from “traffic monetization” to “personal superintelligence” infrastructure marks a generational leap.