June 06, 2026 – A 227% price target revision marks Wall Street’s most dramatic shift on Tesla. The bank now bets on physical AI, robotaxis, and a $3.9 trillion addressable market.

In Summary

JPMorgan upgraded Tesla from Underweight to Neutral on June 5, 2026

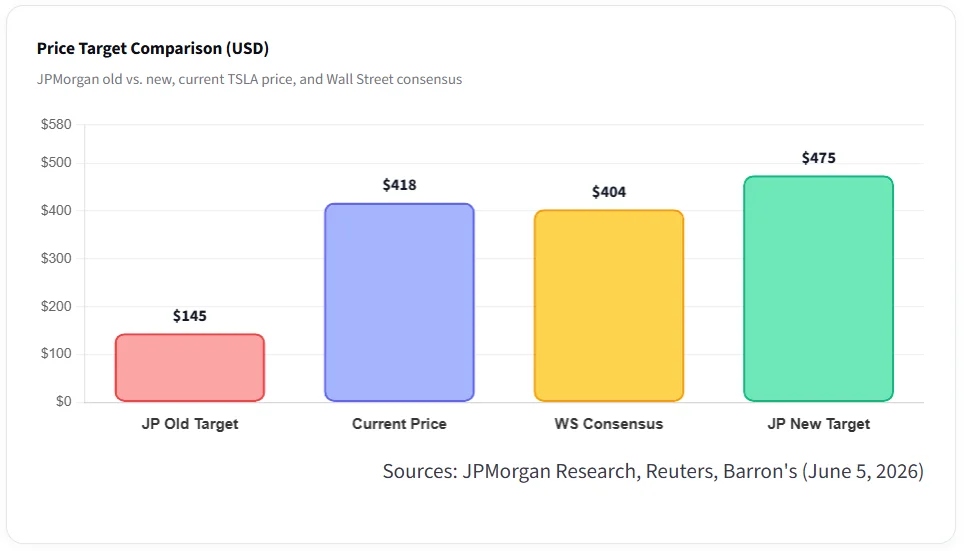

Price target surged from $145 to $475, a 227.6% revision in a single note

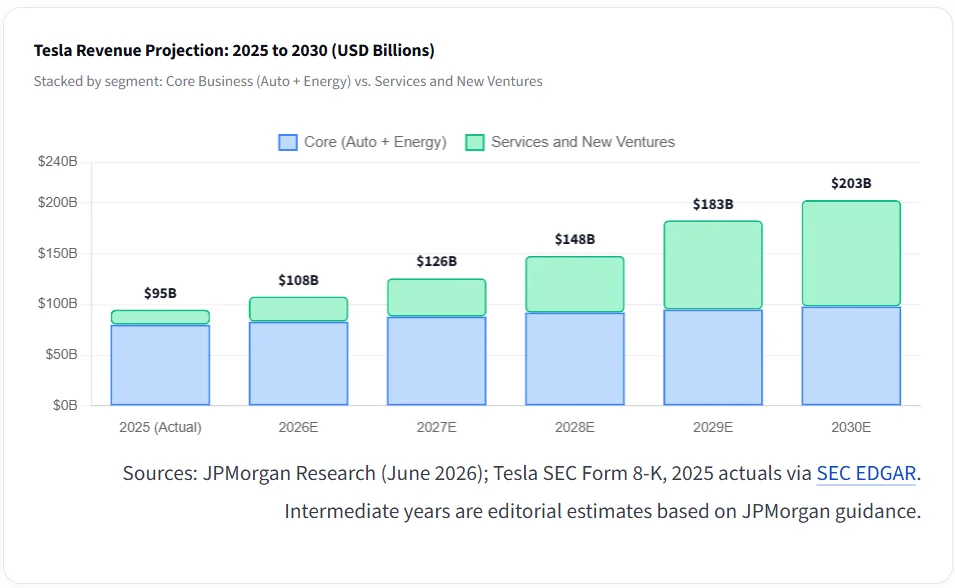

Tesla revenue is projected to grow from $95B in 2025 to $203B by 2030

Five-segment total addressable market reaches $3.9 trillion by 2035

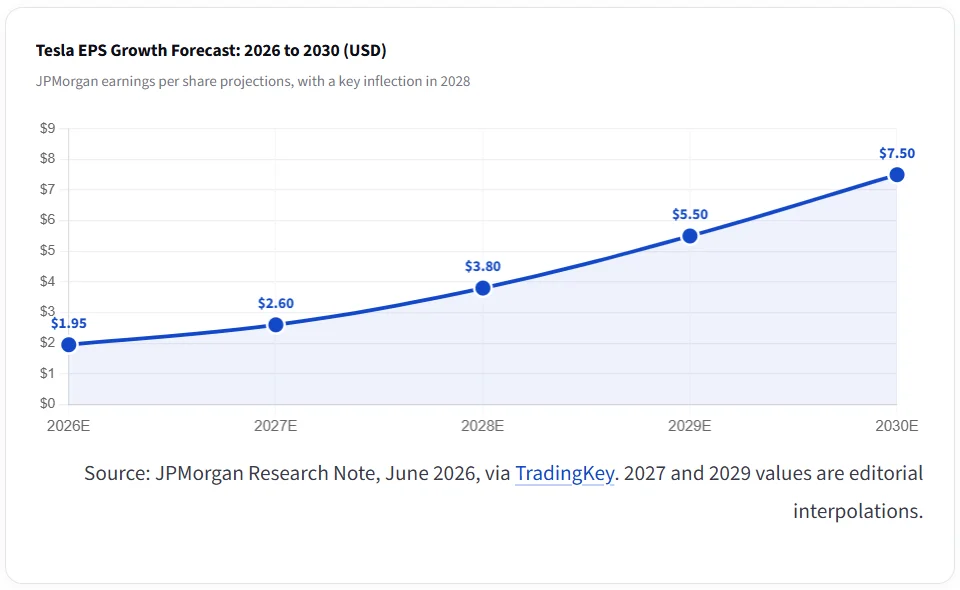

EPS is forecast at $7.50 by 2030, up from just $1.95 in 2026

Execution risks remain high; free cash flow turns positive only by 2029

JPMorgan made a dramatic reversal on Tesla on Friday, June 5. The bank raised its TSLA price target from $145 to $475. This represents a 227.6% revision in a single analyst note. Additionally, the firm upgraded Tesla’s rating from Underweight to Neutral. Analyst Rajat Gupta, who took over Tesla coverage last month, led this call.

A Historic Rating Reversal

JPMorgan had remained one of Tesla’s most persistent Wall Street skeptics. However, the new analyst team reconsidered the company’s long-term potential. The firm now frames Tesla as a “physical AI” company at industrial scale. This is a fundamental change in how investors should price the stock. Therefore, old valuation frameworks tied to car deliveries no longer apply.

The Physical AI Thesis

Analyst Rajat Gupta argues that Tesla’s vertical integration is still underestimated. The company controls its own chip design, software, training data, and factories. This gives Tesla a powerful starting-point advantage over competitors. Furthermore, no other company matches Tesla’s scale across both hardware and AI software. This integration, Gupta writes, is “still somewhat under-appreciated and misunderstood.”

Tesla’s FSD fleet has crossed 10 billion cumulative miles as of May 2026. Active FSD subscriptions reached 1.28 million in Q1 2026. That figure marks a 51% year-over-year jump. Consequently, Tesla’s software monetization story is gaining real traction.

Robotaxi and Optimus Milestones

Tesla’s robotaxi service launched in Austin in June 2025. Since then, it has expanded to Dallas, Houston, and the Bay Area. This rapid rollout validates Tesla’s autonomous driving capabilities at scale. Moreover, Tesla has confirmed that production of the Optimus humanoid robot will begin in July 2026.

JPMorgan estimates a global humanoid robot market of 30 million units by 2040. Additionally, Optimus could cut Tesla’s manufacturing costs by approximately 5%. This creates a powerful feedback loop for the entire business. Lower manufacturing costs lead to cheaper EVs, which in turn accelerates FSD adoption.

“Tesla’s unmatched vertical integration brings a starting-point advantage that is still under-appreciated. We believe the company is entering entirely new, largely untapped markets.”Rajat Gupta, JPMorgan Analyst, June 5, 2026

Revenue and Earnings Projections

JPMorgan projects Tesla’s revenue to grow from $95 billion in 2025 to $203 billion by 2030. Therefore, the company would more than double its top line in five years. Notably, nearly half of that growth comes from services and emerging businesses. These include robotaxi revenue, FSD licensing, and Optimus robot sales.

On earnings, JPMorgan forecasts EPS at $1.95 in 2026. However, this figure rises sharply to $7.50 by 2030. That signals a nearly fourfold increase in earnings power over four years. Furthermore, an earnings inflection point begins clearly in 2028. After that point, approximately 50% annual earnings growth is expected.

The $3.9 Trillion Opportunity

Gupta breaks Tesla’s total addressable market into five segments. These are automotive, energy storage, robotaxis, humanoid robots, and infrastructure licensing. Together, they could reach $3.9 trillion by 2035, per JPMorgan’s research. As a result, Tesla is now targeting markets that largely do not yet exist.

Specifically, Tesla’s personal vehicle fleet could reach 35 million units by 2040. Additionally, its robotaxi fleet could reach 40 million units by the same date. These projections underline both the scale of the opportunity and the execution challenge.

Valuation and Risks: High Risk

Despite the optimism, JPMorgan flagged several significant execution risks. Regulatory approvals for autonomous vehicles remain uncertain and jurisdiction-specific. Scaling new technologies from prototype to mass production is a complex challenge. Moreover, free cash flow is not expected to turn positive until 2029.

Tesla currently trades at a price-to-earnings ratio of 383.9, signaling a premium valuation. JPMorgan concedes that current multiples are “undeniably lofty on near-term earnings.” Nevertheless, the firm argues Tesla should be valued on long-term potential. In addition, Tesla insiders sold approximately $21.5 million in shares over the past three months. No insider purchases were recorded during the same period, raising questions about confidence.

Market Reaction and Analyst Consensus

Tesla shares gained approximately 0.3% in Friday’s premarket trading session. TSLA is down 7% year-to-date but has risen 26% over the past 12 months. By comparison, the S&P 500 ETF (SPY) has gained 27% in the same period. Therefore, Tesla has underperformed the broader market on a year-to-date basis.

Wall Street consensus currently sits at “Moderate Buy.” The average 12-month price target stands at approximately $404. Thus, JPMorgan’s new $475 target exceeds the consensus by approximately 17%. Furthermore, Erste Group also upgraded Tesla from “Sell” to “Hold” on the same day. This broader shift in sentiment may attract additional institutional interest.

Bottom Line

JPMorgan’s upgrade marks a clear turning point in institutional sentiment on Tesla. The bank now sees a company building toward trillion-dollar markets in robotics and autonomy. However, near-term execution risks and a stretched valuation deserve serious consideration. Therefore, this remains a high-reward investment best suited for long-term, risk-tolerant holders.