May 28, 2026 – Wall Street’s top bank raises its year-end forecast by 5.3%, pointing to exceptional Q1 earnings and AI-driven profit growth as the key catalysts behind the upgrade.

In Summary

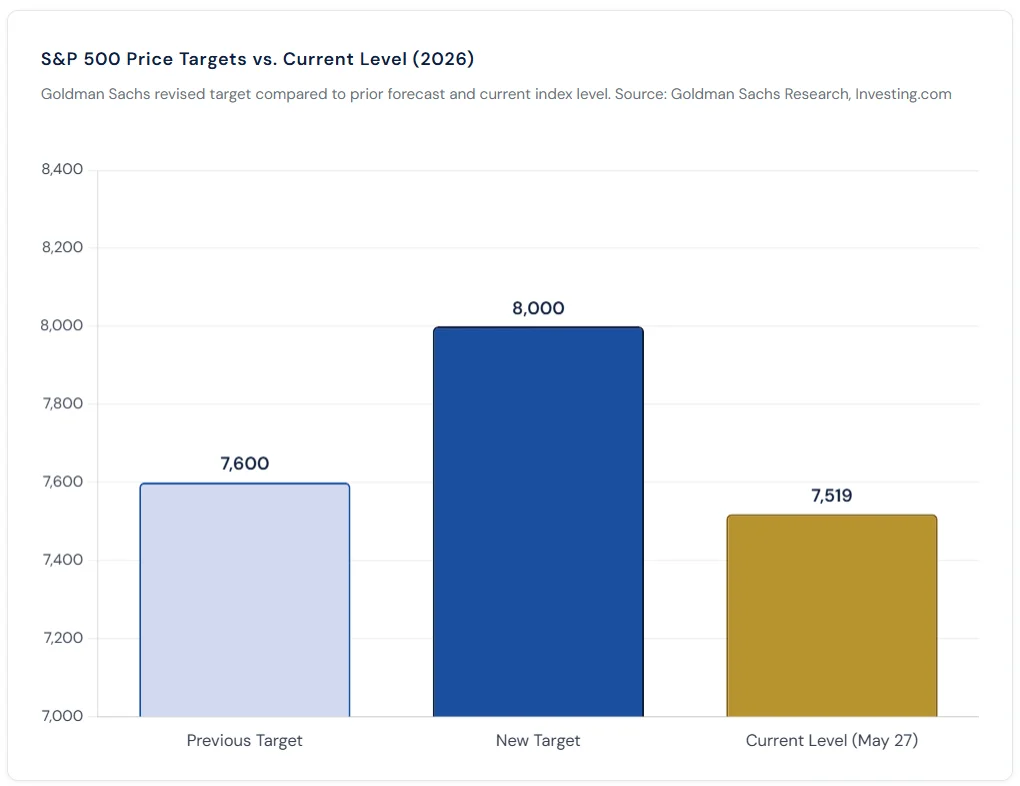

Goldman Sachs lifted its S&P 500 year-end target to 8,000, up from 7,600.

Analyst Ben Snider forecasts a further 6% index gain from current levels.

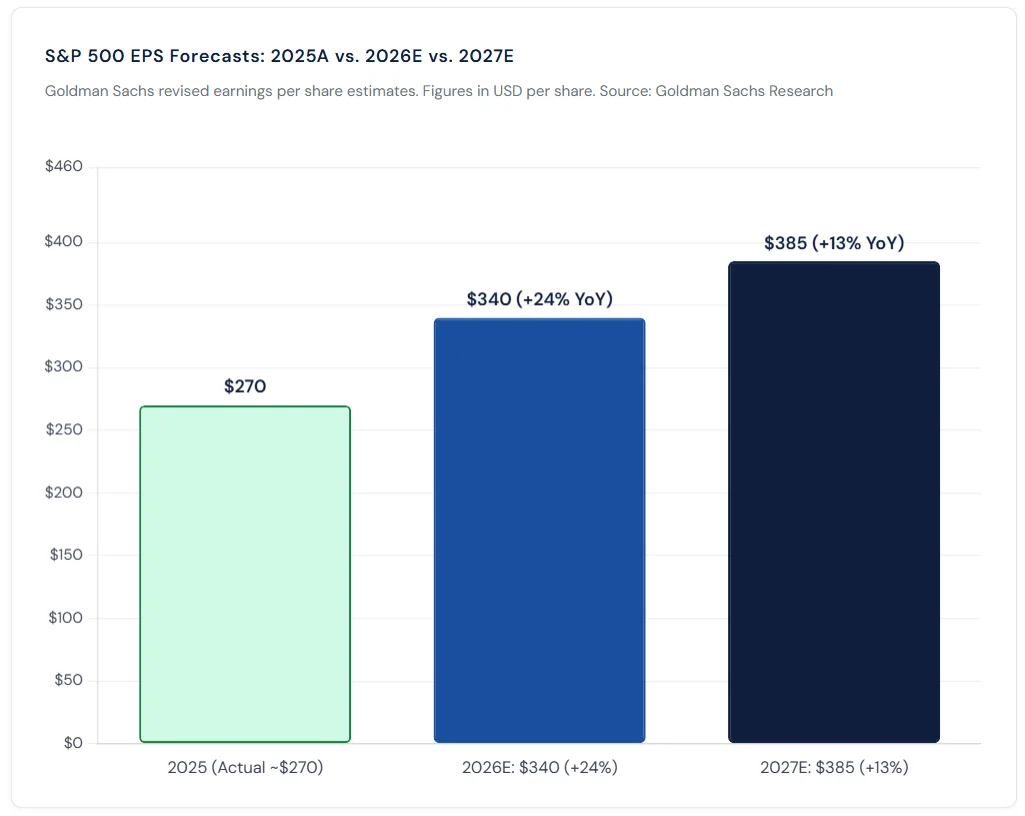

The 2026 EPS forecast stands at $340, implying 24% year-on-year growth.

AI infrastructure beneficiaries account for roughly 50% of projected EPS growth.

Valuation expansion is not expected to drive returns; the P/E stays near 21x.

Oil price shocks and midterm election seasonality remain key near-term risks.

Goldman Sachs published a note on Wednesday raising its S&P 500 year-end target. The bank now forecasts the index will close 2026 at 8,000. That is up from its previous target of 7,600. Analyst Ben Snider authored the research, citing an exceptionally strong first-quarter earnings season.

The S&P 500 currently trades near 7,519. Therefore, the new target implies a further 6.4% upside from today’s levels. Goldman believes continued earnings growth will power this move. Valuation expansion, however, is not expected to contribute meaningfully.

A Bold Upgrade Backed by Earnings

Goldman’s revision rests on two upgraded profit forecasts. First, the bank raised its 2026 S&P 500 earnings-per-share (EPS) estimate to $340. That represents 24% year-on-year growth. Second, it now targets 2027 EPS at $385, implying a further 13% increase. Both figures are meaningfully higher than prior consensus estimates.

Furthermore, the Q1 2026 earnings season delivered results well above expectations. According to FactSet’s Earnings Insight, approximately 79% of S&P 500 companies reported Q1 earnings above analyst estimates. That beat rate is well above the 10-year average of 74%. Moreover, aggregate earnings growth for the quarter came in above initial forecasts.

The S&P 500 has already climbed roughly 10% year-to-date. Snider argued that this performance reflects genuine earnings momentum. Importantly, it has not been fueled by investors paying higher multiples. Instead, the market has re-rated earnings power upward. This distinction matters greatly for the outlook ahead.

AI Infrastructure Fuels Half of EPS Growth

Technology and artificial intelligence spending remain the dominant themes. Goldman estimates that AI infrastructure beneficiaries will generate approximately half of all S&P 500 EPS growth in 2026. This is a striking concentration of returns within a single investment theme.

Specifically, Snider highlighted two groups. The first is hyperscalers, meaning cloud and AI platform companies such as Microsoft, Alphabet, and Amazon. The second is power infrastructure businesses. These include utilities and industrial firms that support the energy demands of large data centers. Additionally, stocks with the strongest earnings revisions have broadly outperformed in 2026.

“AI infrastructure beneficiaries will account for roughly half of S&P 500 EPS growth this year,” Goldman Sachs analyst Ben Snider wrote on Wednesday.

Valuations Steady Near 21x Forward Earnings

One of Goldman’s key arguments is that valuations have already adjusted. The S&P 500’s forward price-to-earnings (P/E) multiple declined 4% year-to-date. This occurred even while the index rose 10%. The market, therefore, became cheaper relative to earnings as earnings outpaced prices.

Goldman’s model incorporates a P/E multiple that “remains close to the current 21x.” This is broadly in line with the 5-year historical average. Consequently, the bank does not expect multiple expansion to be a driver. Earnings, not sentiment, must carry the market higher from here.

Risks That Could Derail the Rally

Goldman did not present an unconditional bull case. Snider flagged several material risks. An oil price shock could tighten financial conditions. That combination has historically ended bull markets. Oil prices have recently fallen, but geopolitical tensions in the Middle East keep the risk elevated.

In addition, AI infrastructure stocks have already rallied sharply. Their strong year-to-date gains raise the performance hurdle for future quarters. Investors may require sustained earnings beats to justify current prices. Moreover, midterm election seasonality typically suggests softer returns in summer and early autumn.

According to Federal Reserve Economic Data (FRED), the U.S. economy has shown resilience in 2026. However, the Fed’s interest rate policy remains a watch point. Higher-for-longer rates could weigh on equity multiples if inflation re-accelerates.

What This Means for Investors

Goldman’s note offers a constructive but selective outlook. Broad index exposure still carries merit, given the earnings backdrop. However, the bank urges investors to focus on companies with the strongest upward earnings revisions. These businesses have consistently outperformed in the current environment.

Within AI, the message is nuanced. Hyperscalers and power infrastructure remain attractive. Nevertheless, investors should be mindful that consensus expectations are already elevated. Furthermore, any macro deterioration could disproportionately weigh on these high-multiple names.

Finally, Goldman’s tactical signal is cautious. The momentum-driven nature of the recent rally suggests near-term returns may moderate. However, the fundamental earnings story remains intact. A further 6% gain by year-end is achievable, assuming earnings are delivered as projected.