June 04, 2026 – Applied Aerospace and Defense raised $650 million in a 10x oversubscribed IPO. Yet shares closed 4.95% below the offer price on Day 1. Here is what investors need to know.

In Summary

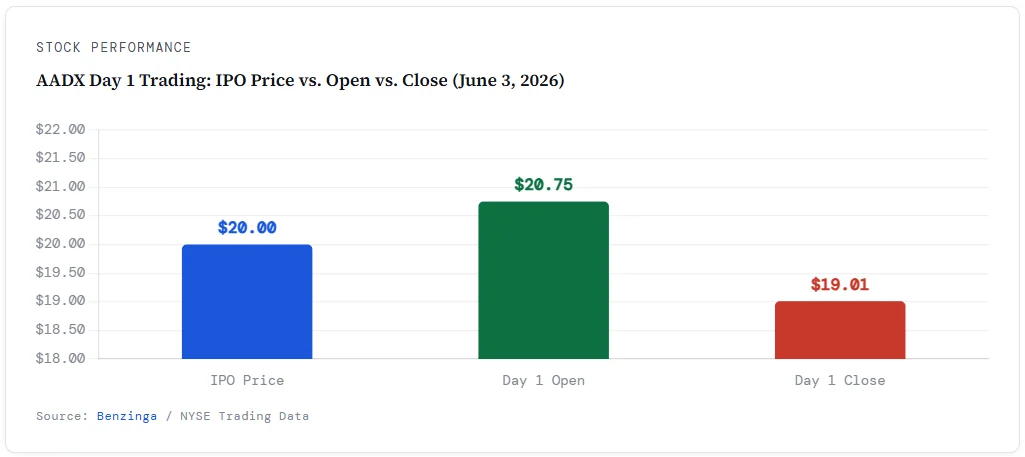

IPO Price: AADX priced at $20.00 per share on June 3, 2026, raising $650 million.

Demand: The order book was 10 times oversubscribed before trading began.

Day 1 Close: Shares reversed and ended at $19.01, a 4.95% drop from the offer price.

Heritage: The company traces its roots to 1900, predating powered flight.

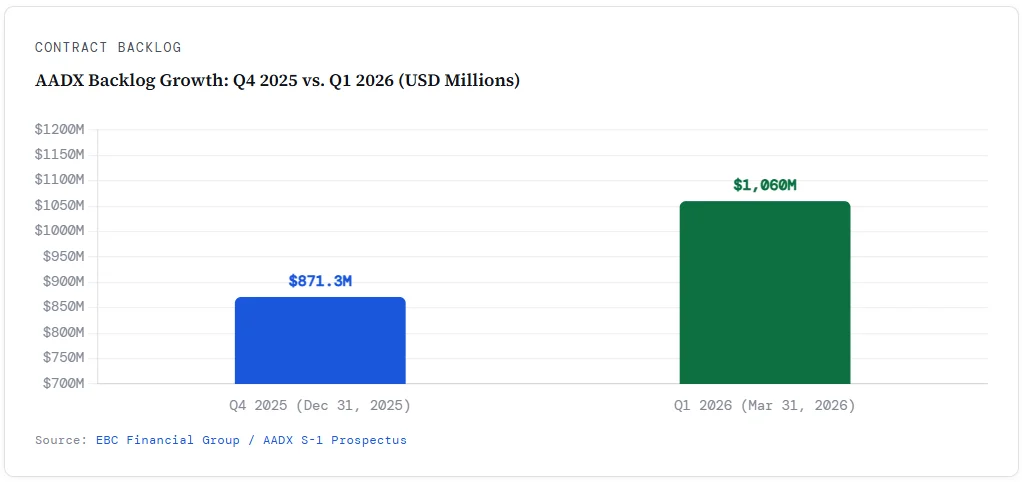

Backlog: Contract backlog reached $1.06 billion as of March 31, 2026.

Debt: Total debt stood at approximately $1.02 billion at IPO.

Sole-Source: 87% of 2025 revenue came from sole-source contracts.

Applied Aerospace and Defense (NYSE: AADX) began trading on June 3, 2026. The stock debuted on the New York Stock Exchange at a price of $20 per share. It raised $650 million through the offering. However, its first trading session ended on a sour note.

Shares opened strong at $20.75. Then selling pressure built through the afternoon. By the closing bell, AADX traded at $19.01. That marks a 4.95% decline from the IPO price. Furthermore, it signals a split verdict from the market.

A Company Built From Historic Roots

Applied Aerospace and Defense formed in December 2025. Private equity firm Greenbriar Equity Group created it by merging two manufacturers. The first was PCX Aerosystems, founded in 1900. The second was Applied Aerospace, established in 1954. Together, they carry over 125 years of manufacturing history.

PCX Aerosystems has a remarkable origin. It was founded two years before the Wright Brothers’ first flight. Applied Aerospace, meanwhile, emerged just after the sound barrier was broken in 1947. Therefore, the company’s combined heritage spans virtually the entire arc of modern aviation.

“These are not new relationships. They are supplier partnerships forged over decades, the kind that take generations to build and are nearly impossible to replicate overnight.”

What Applied Aerospace and Defense Makes

AADX produces mission-critical hardware. Its products are unglamorous but essential. The company makes fuselage and wing structures, solid rocket motor cases, and rotor-head assemblies. It also produces flight control surfaces, nose cones, engine shafts, landing gear, and satellite bus structures.

Customers include industry giants such as SpaceX and Lockheed Martin. SpaceX’s Falcon 9 depends on AADX components to fly. Moreover, Lockheed Martin jets would not leave the runway without its parts. These relationships are deeply embedded and hard to replace.

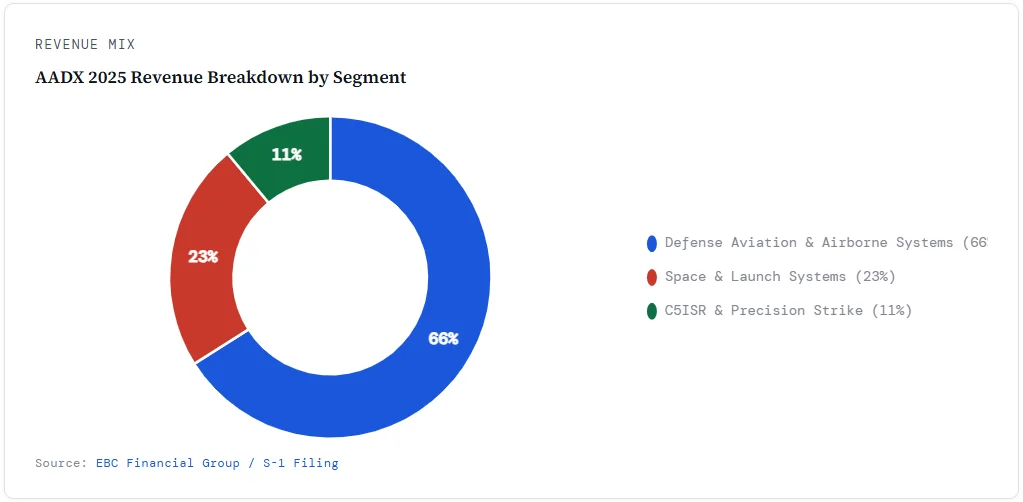

Three segments drive revenue. Defense aviation and airborne systems lead at 66%. Space and launch systems follow at 23%. C5ISR and precision strike systems contribute the remaining 11%. This mix positions AADX as a defense-industrial supplier with meaningful exposure to the space sector.

Notably, 87% of 2025 revenue came from sole-source or single-source contracts. This concentration reduces competitive risk significantly. However, it also raises delivery pressure. Any production failure has outsized consequences for customer programs.

IPO Structure and Use of Proceeds

Morgan Stanley and Jefferies served as lead underwriters. BofA Securities, RBC Capital Markets, and Guggenheim Securities also participated. Baird, Stifel, and Wolfe-Nomura Alliance were bookrunners. Academy Securities acted as co-manager.

The company entered the market with heavy debt. Total indebtedness was approximately $1.02 billion at March 31, 2026. Accordingly, most IPO proceeds are used for debt repayment. The company plans to use $532.8 million to repay term-loan obligations. A further $56.1 million targets revolving credit borrowings.

This debt-reduction focus is intentional. A cleaner balance sheet improves financial flexibility. It also positions AADX to compete for new contracts in growing defense programs.

The Backlog: A Signal of Future Revenue

The contract backlog is a key metric for any defense manufacturer. AADX reported a backlog of $1.06 billion as of March 31, 2026. This is up from $871.3 million at year-end 2025. The backlog exceeds reported annual revenue by more than twice. Therefore, it provides strong near-term revenue visibility.

However, investors should note one important caveat. Backlog is not the same as earned revenue. Contracts must still convert into actual deliveries. Execution risk is real. Any delay or cancellation directly impacts reported results.

Why the Market Backdrop Favors AADX

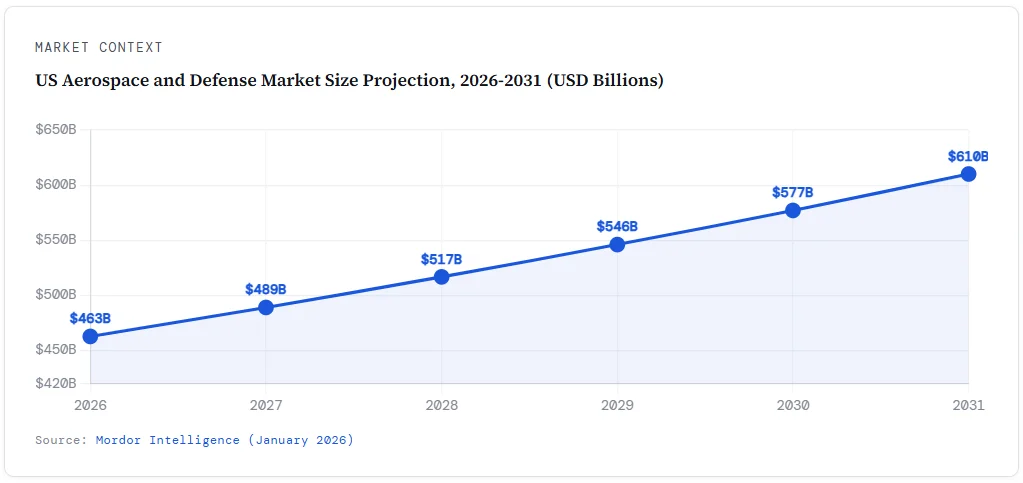

The timing of this IPO is strategically sound. The US aerospace and defense market is valued at $463.06 billion in 2026. It is projected to grow to $610.15 billion by 2031. That represents a 5.67% compound annual growth rate. Furthermore, space platforms are the fastest-growing segment at a 7.12% CAGR.

The US FY2026 defense budget is another tailwind. Procurement spending stands at $152.8 billion. Research and development funding is $142 billion. These figures signal sustained demand for the components AADX supplies.

Geopolitical tensions are driving further spending increases. Defense modernization programs are accelerating across NATO and allied nations. Additionally, commercial space launch activity is growing rapidly. AADX sits at the center of these trends.

Reading the Day 1 Selloff

The 10x oversubscription signals strong institutional demand at the pricing level. Nevertheless, the first-day loss warrants a closer look. This kind of reversal is not unusual for industrial IPOs. Early allocatees often sell to lock in quick profits after a strong open.

However, a few specific concerns may have weighed on sentiment. First, the company carries over $1 billion in debt. Second, most IPO proceeds go to debt repayment rather than growth investments. Third, 87% sole-source concentration, while protective, also creates delivery-risk exposure.

Moreover, the 28% gross margin is moderate for a defense manufacturer. Premium industrial defense companies often achieve margins well above 30%. Therefore, margin improvement will be a key benchmark for investors in the coming quarters.

Competitive Landscape

AADX competes in a high-barrier, relationship-driven industry. Its primary peers include TransDigm Group, Ducommun, and Heico Corporation. These companies trade at premium valuations due to high switching costs in aerospace supply chains. AADX’s century-long relationships represent a significant structural moat.

Additionally, AADX benefits from the vertical integration strategy. It designs, fabricates, and tests in-house. This reduces dependency on third-party suppliers. It also allows faster prototyping and tighter quality control. Both factors are important to customers like SpaceX and Lockheed Martin.

What to Watch Next

Several milestones will define the AADX investment case in 2026. First, investors should watch quarterly backlog conversion rates. Backlog growing faster than revenue is a positive signal. Second, debt paydown progress will affect the balance sheet quality narrative. Third, any new contract awards with major customers will move the stock.

In summary, AADX brings extraordinary industrial heritage to a well-timed public offering. The fundamentals are solid. The market context is favorable. However, the debt overhang and modest Day 1 trading suggest the market is adopting a wait-and-see posture. Watch execution closely over the next two to three quarters.