July 07, 2026 – Cash keeps pouring into US money markets. Yet bank reserves now slip below comfort levels, and the Federal Reserve leans hawkish.

In Summary

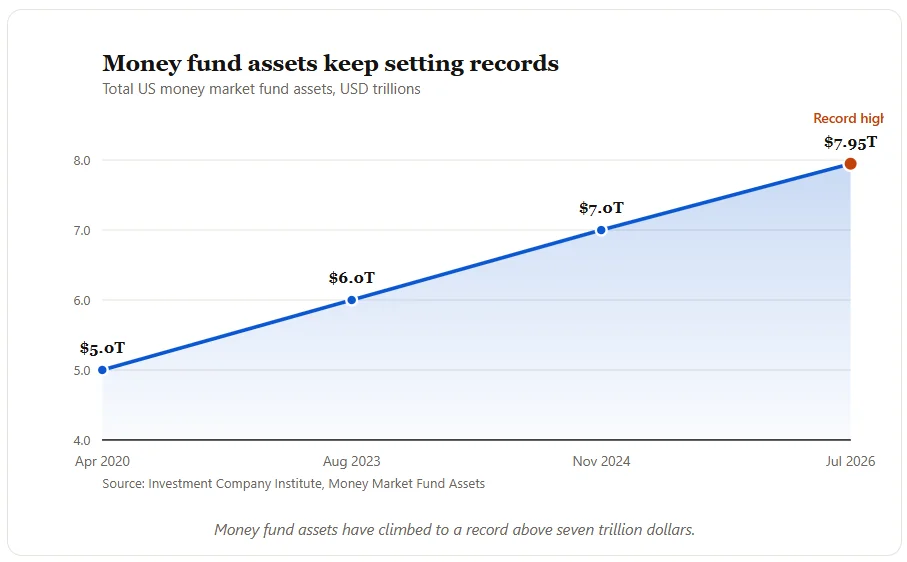

Money fund assets set a fresh record near 7.95 trillion dollars in early July 2026.

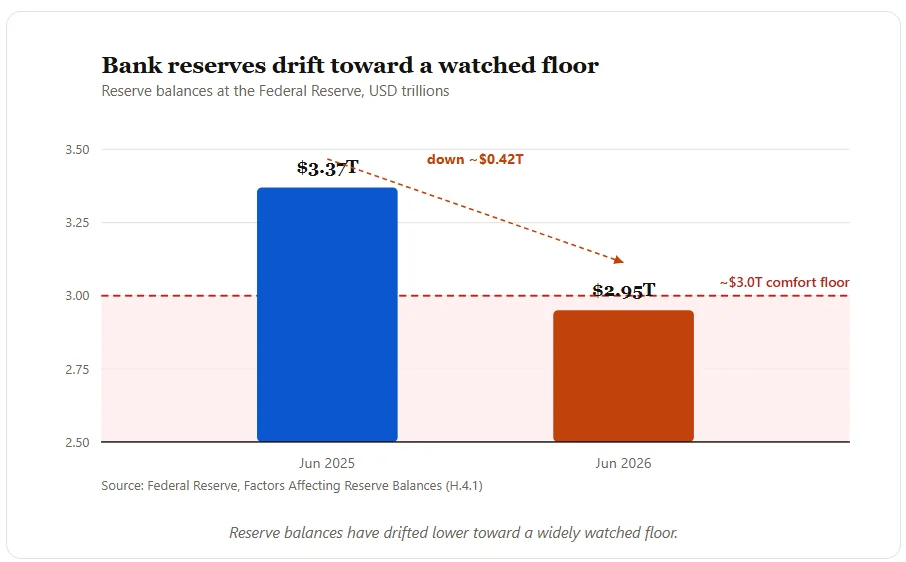

Bank reserves slipped to about 2.95 trillion dollars, close to a widely watched floor.

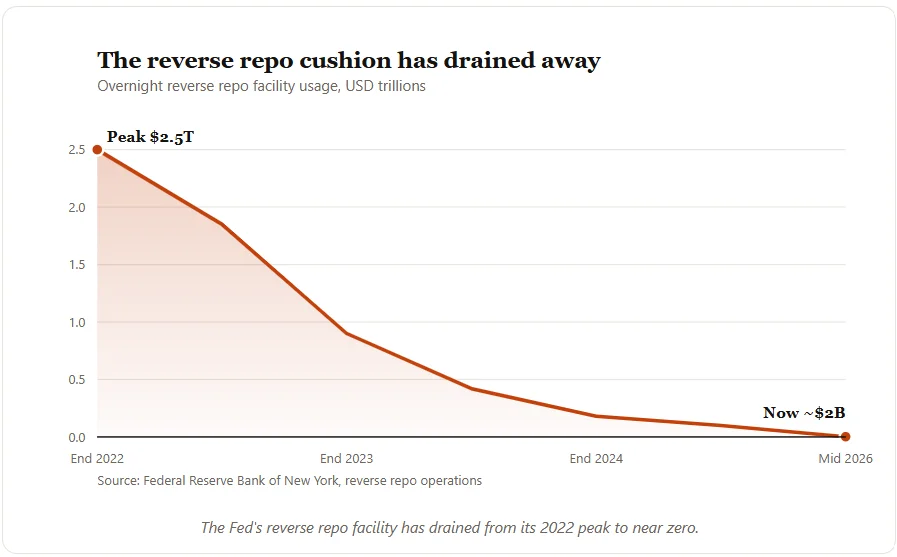

The reverse repo cushion has drained from 2.5 trillion dollars to roughly 2 billion.

The Fed now buys Treasury bills directly to keep reserves ample.

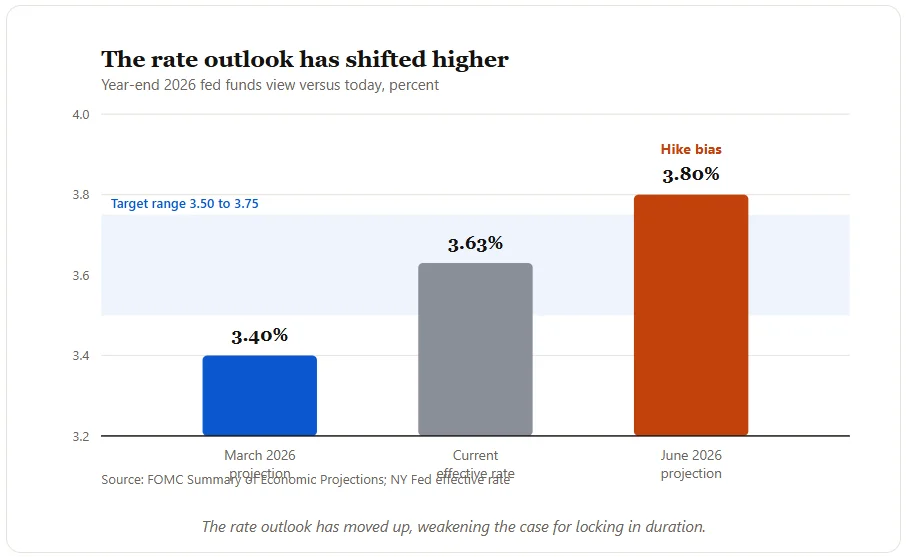

A hawkish rate outlook weakens the classic case for terming out.

US money markets look calm on the surface. Underneath, the plumbing tells a tenser story. Record cash sits in money funds today. Meanwhile, bank reserves keep draining lower. The Federal Reserve now buys Treasury bills to steady the system.

US money markets stay flush with cash

Money fund assets just hit a fresh record. Total assets reached 7.95 trillion dollars in early July 2026. That marks yet another peak for the industry. Furthermore, the inflows show little sign of slowing. Retail savers alone now hold 3.09 trillion dollars.

Government funds hold the bulk of this cash. They buy Treasury bills and repos in size. Prime funds, meanwhile, chase a little extra spread. Institutions run the largest slice overall. In fact, they hold well over half of all assets.

Investors clearly still like the yields on offer. The effective federal funds rate sits near 3.63 percent. Therefore, a cash-like return above 3 percent looks appealing. Moreover, money funds pass most of that yield straight to shareholders. So the pull toward these products remains strong.

Reserves slip toward the danger zone

Bank reserves, by contrast, tell a very different story. They fell to 2.95 trillion dollars by late June 2026. A year earlier, reserves stood near 3.37 trillion dollars. Consequently, roughly $ 400 billion has left the banking system.

Analysts watch the 3-trillion-dollar mark closely. Below it, funding markets can turn jumpy fast. Back in 2019, thin reserves sparked a repo scare. As a result, the Fed wants to avoid any repeat. It therefore now adds reserves through bill purchases.

The Fed’s balance sheet also frames this backdrop. Total assets stand at nearly 6.7 trillion dollars today. Earlier tightening shrank that pile substantially. Mortgage bonds still roll off it each month. However, fresh bill buying now offsets much of that runoff.

The Treasury also shapes this liquidity picture. Its cash pile is near $ 919 billion. When that balance climbs, reserves tend to fall. Thus, a forthcoming cash rebuild would further drain liquidity.

The reverse repo cushion has vanished

The Fed once ran a huge reverse repo facility. Balances there peaked near 2.5 trillion dollars in late 2022. Today, they hover around just 2 billion dollars. In effect, that giant cushion has now vanished.

This shift matters for the whole system. Previously, spare cash was parked safely at the Fed each night. Now that buffer no longer masks any tightness. Instead, private repo rates increasingly set the tone. Consequently, small shocks show up faster in funding costs.

Quarter-end still brings brief bursts of demand. Some funds tap the facility to tidy their balance sheets. Yet those visits stay small and fleeting. On most days, private markets absorb the cash instead.

The Fed reshapes its money market toolkit

The central bank has quietly retooled its approach. Officials now buy Treasury bills to manage reserves directly. They also reinvest maturing mortgage bonds into bills. This tilt keeps the balance sheet toward the short end. Meanwhile, the net reserve impact stays roughly balanced.

Such bill buying echoes the Fed’s 2019 playbook. Back then, targeted purchases calmed a sudden funding squeeze. Today, the goal looks similar yet more preventive. Officials clearly prefer early action over a later scramble.

The June policy statement reaffirmed ample reserves as the goal. Notably, that language ran much shorter under new leadership. Still, the core message stayed perfectly clear. Policymakers will keep the market plumbing working smoothly.

Why terming out looks harder now

Terming out simply means buying longer-dated paper. Investors swap overnight cash for three- or six-month bills. In return, they hope to lock in current yields. That trade shines brightest when cuts loom ahead.

Locking in longer maturities once looked like an easy win. The logic assumed that rate cuts lay just ahead. However, that comfortable view has shifted sharply. In June 2026, policymakers held rates at 3.50 to 3.75 percent. It was their fourth straight decision to hold.

The dot plot then turned distinctly hawkish. Officials lifted their year-end median to 3.8 percent. Back in March, that same figure sat at 3.4 percent. Traders now price a possible hike as soon as October.

Stubborn inflation drives most of this caution. The Fed sees core inflation near 3.3 percent this year. Energy shocks from the Middle East add further pressure. Therefore, meaningful cuts look distant for the moment.

As a result, the case for terming out clearly weakens. Investors receive lower returns for extending maturity today. Still, some value can remain over a longer horizon. For patient buyers, locking rates hedges against a later downturn.

What comes next for US money markets

US money markets remain both flush and fragile. Cash is abundant, yet reserves keep thinning out. The next real test arrives as the Treasury rebuilds cash. Above all, watch reserves, repo rates, and the Fed’s bill buying closely.

A calm summer could still give way to strain. September and quarter-end often put stress on funding markets. Therefore, the coming months deserve real attention. For now, though, the system holds together well.

Yields also keep the incentives finely balanced. Savers earn solid returns while waiting for clarity. Meanwhile, borrowers watch every shift in repo closely. In short, patience may prove the smartest position.