June 06, 2026 – May nonfarm payrolls nearly doubled Wall Street forecasts. Federal Reserve rate hike odds surged to 61%. Here is what the blowout data means for dollar traders.

In Summary

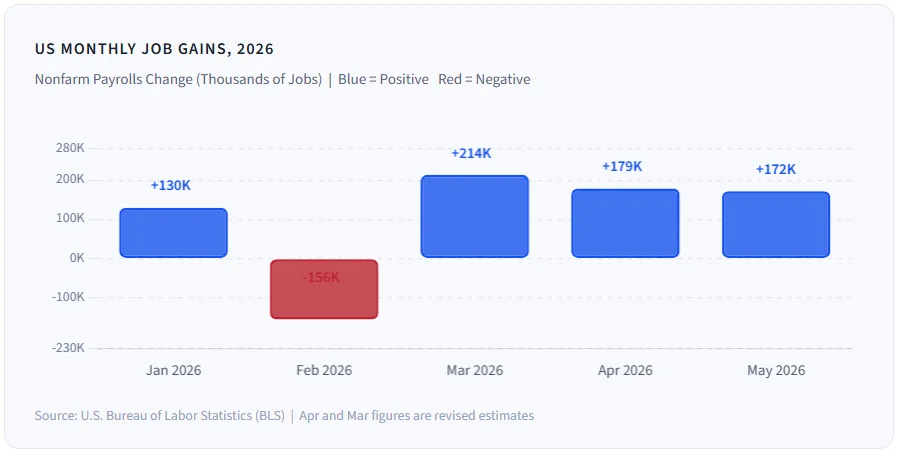

US May NFP jumped to 172K, nearly double the 85K consensus forecast

Unemployment rate held steady at 4.3%; wage growth eased to 3.4% annually

Prior months revised upward by a combined net 93K jobs

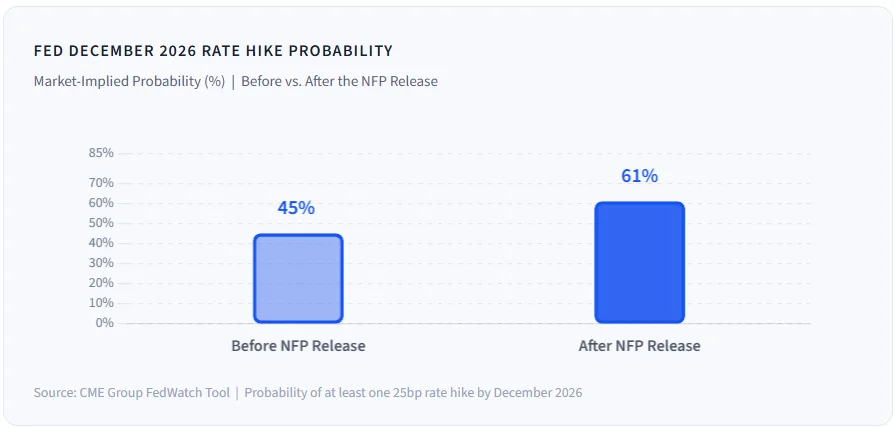

Fed December 2026 rate hike probability climbed to 61%, up from 45%

Oil below $100 per barrel is capping the full dollar breakout

ING expects continued dollar strength ahead of the May CPI release

The US dollar gained ground sharply on Friday. May nonfarm payrolls rose 172,000, far exceeding Wall Street’s forecast of 85,000. Markets responded by aggressively pricing more Federal Reserve tightening. Furthermore, the unemployment rate held steady at 4.3%, meeting expectations.

Payrolls Smash Every Forecast

May delivered a decisive win for dollar bulls. According to the Bureau of Labor Statistics (BLS), the economy added 172,000 nonfarm payrolls last month. Analysts had projected just 85,000. The actual print topped every single estimate in the consensus range.

Prior months also received meaningful upward revisions. March was revised from 185,000 to 214,000. April moved from 115,000 to 179,000. Together, these changes add a net of 93,000 jobs more than first reported. This pattern signals strong ongoing resilience in US hiring conditions.

Wage growth remained well-behaved in May. Average hourly earnings rose 0.3% month-on-month. Annual wage growth softened to 3.4% from 3.6% in April. The workweek held steady at 34.3 hours. Taken together, these details paint a very clear employment picture.

Services Drive All Job Growth

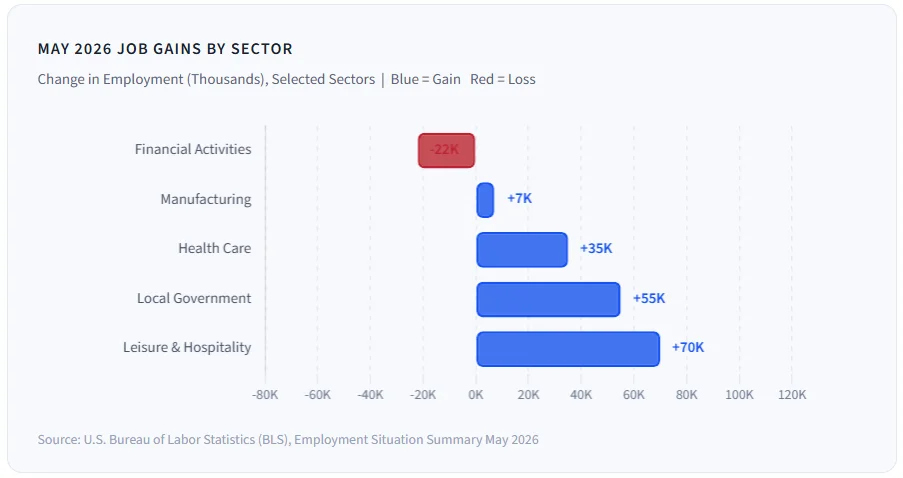

Services dominated the May employment picture. Leisure and hospitality led all sectors with 70,000 new jobs. Food services and drinking places accounted for the bulk of this gain, adding 48,000 jobsalone. Local government hiring contributed 55,000 positions. Health care continued its steady expansion, adding 35,000 jobs.

Manufacturing added a modest 7,000 jobs. Financial activities, however, shed 22,000 positions. Therefore, goods-producing and financial sectors remain under pressure. Service industries continue to carry the US labor market forward.

Fed Rate Hike Odds Climb to 61%

Markets responded decisively to the strong report. CME FedWatch data show that December 2026 rate-hike odds have climbed to 61%. Before the release, markets placed that probability at 45%. Moreover, markets had previously priced just 17 basis points of additional Fed tightening.

ING analyst Francesco Pesole anticipated this shift in a pre-release note. He projected payrolls above consensus at 100,000 versus a street estimate of 88,000. The actual 172,000 print exceeded even his above-consensus forecast by a wide margin. He argued that an upside surprise would push markets to fully price a Fed rate hike.

The USD Index rose about 0.5% in June. It had already gained 0.9% in May. Consequently, the dollar has built solid gains across two consecutive strong months. The Federal Reserve has maintained elevated interest rates amid the ongoing conflict in Iran. Previously, markets expected rate cuts in mid-2026. That narrative has now fully reversed.

Oil Prices Cap the Dollar Breakout

Strong economic data alone has not triggered a full dollar breakout. Brent crude oil remains the key constraint. ING highlighted that Brent has struggled to reclaim the $ 100-per-barrel level. This is despite the US-Iran negotiations stalling for more than 100 days.

Pesole noted that markets appear to price in optimism about an eventual peace deal. This sentiment is keeping oil prices from spiking higher. As a result, the dollar has found a ceiling despite a materially stronger macro backdrop. For a sustained breakout, oil would likely need to surge toward the $100 threshold.

The conflict in Iran has driven energy costs up across the board since it began. Persistent high energy costs remain an inflationary input for the US economy. Additionally, this environment supports the case for the Fed to hold rates elevated longer.

Currency Pairs and What to Watch Next

Several currency pairs now approach critical technical levels. EUR/USD held above 1.1600 but faces growing selling pressure. GBP/USD slipped below 1.3400 after the jobs release. USD/JPY moved back toward 160.00, where Japanese authorities previously issued verbal warnings.

Gold prices fell toward $4,300 per troy ounce on the news. Rising dollar strength and higher rate expectations weigh on non-yielding assets like gold. Moreover, the next key macro test is the May CPI report on June 10, 2026.

A strong CPI print would further reinforce the hawkish Fed narrative. Conversely, softer inflation data could limit additional dollar gains. Either way, the May jobs report has firmly reset the macro conversation in the dollar’s favor.