July 05, 2026 – Washington’s $1,000 baby bonus looks generous on paper. After inflation and tax, the real payoff tells a quieter story.

In Summary

The federal seed is a one-time $1,000 payment for U.S. children born between 2025 and 2028.

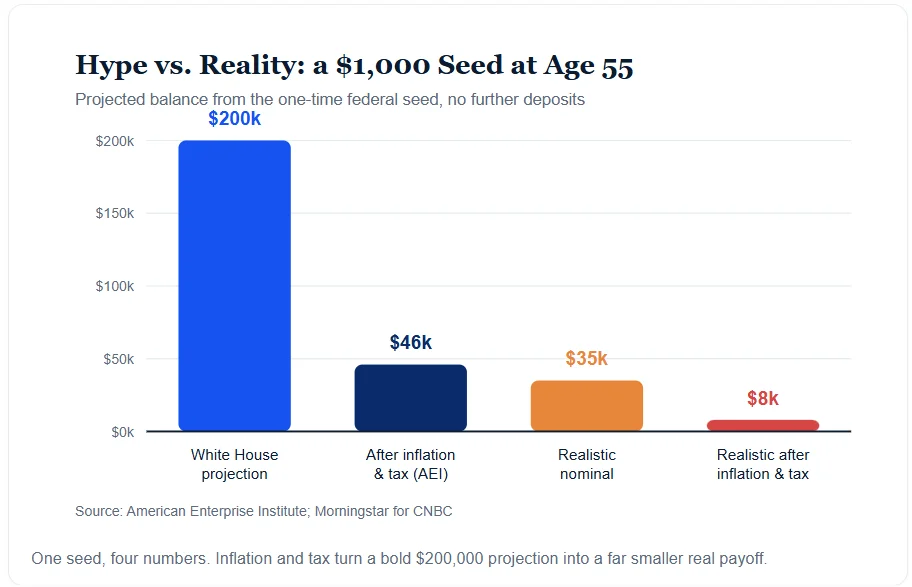

The White House projects $200,000 by age 55; AEI sees about $46,000 after inflation and taxes.

Under sober return math, the seed alone may reach roughly $35,000, or nearly $8,000 in today’s money.

Steady family and employer deposits, not the seed, drive most long-run growth.

Early withdrawals, known as leakage, can shrink some balances to $0.

A $1,000 Head Start for Newborns

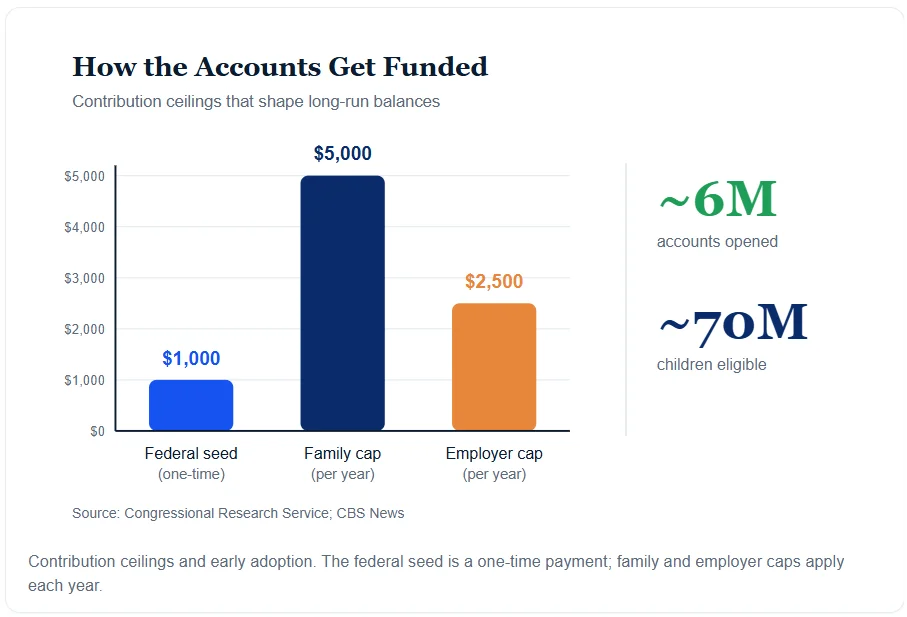

Washington has launched a bold savings plan for American kids. Trump Accounts now seed $1,000 for each eligible newborn. The government funds citizens born between 2025 and 2028. Families, employers, and charities can then add more over time. As of June 2026, nearly six million accounts had been opened. Meanwhile, about 70 million children still qualify nationwide.

Each account tracks a low-cost fund tied to the S&P 500. Fees are capped at 0.10% under the law. Moreover, families can add up to $5,000 each year. Employers may chip in $2,500 within that same limit. Therefore, the design looks cheap, simple, and easy to run. Notably, 86% of early applicants earn less than $200,000 per year. To claim the seed, a parent files a simple tax election. Each child may hold just one funded account.

Trump Accounts Meet an Inflation Problem

Kids cannot touch the cash until they turn 18. At that point, the account becomes a normal IRA. However, the headline numbers deserve a much closer look. The White House says a $1,000 seed could reach $200,000 by age 55. Yet that math assumes yearly stock gains above 10%. Furthermore, it skips both future inflation and later taxes.

Analysts at the American Enterprise Institute pushed back hard. They took the same $200,000 and adjusted it. After inflation and tax, the real value falls to about $46,000. Put simply, future dollars buy far less than today’s dollars. This gap matters most for money held across many decades. Market valuations are also high, which often signals weaker future gains.

The Gap Between Projection and Payoff

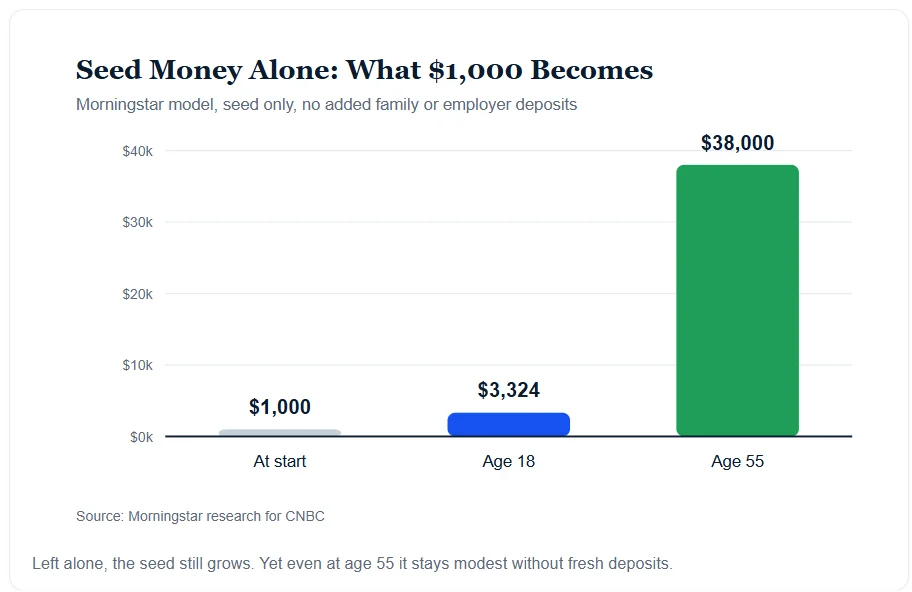

The gap grows wider under more sober return math. AEI thinks the untouched seed likely grows to roughly $35,000. After inflation and tax, that sum equals nearly $8,000 today. Morningstar reached a close view in work for CNBC. Its model put the seed-only balance near $38,000 at age 55. Both figures land far below the bright $200,000 headline.

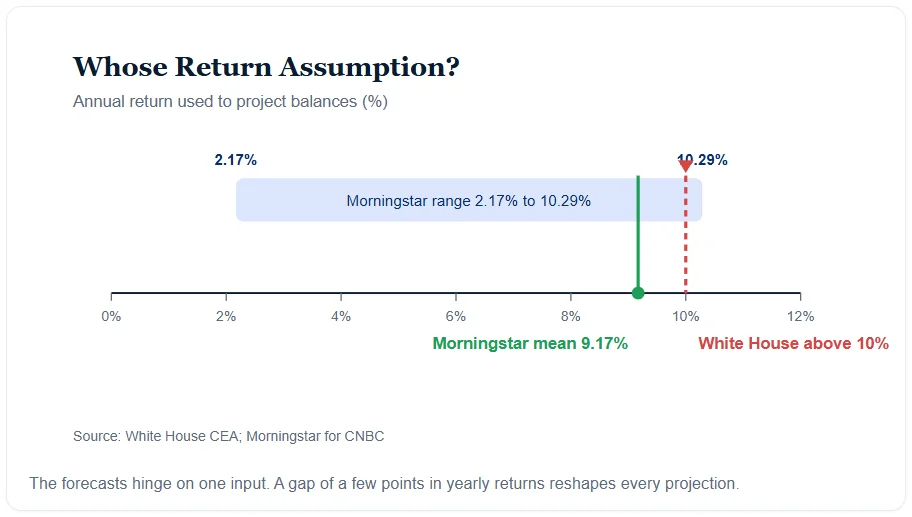

Return math drives much of this sharp split. The White House leans on gains of more than 10% each year. By contrast, Morningstar’s mean return was 9.17%. Its results ranged from 2.17% to 10.29%. Thus, small shifts in the math swing the payoff a lot. Investors should treat any single forecast with real care.

Even the White House shows humble figures for the seed alone. Its own mid-range case puts a seed-only account near $5,800 by age 18. President Trump once touted balances above $100,000 by 18. That bolder claim, though, needs large yearly deposits to hold up.

Contributions Matter More Than the Seed

Still, these accounts can build real wealth over long spans. The true key lies in steady deposits, not the seed. Morningstar found that added money drives most account growth. For seed-only holders, the average age-18 balance hit just $3,324. That small sum shows the limits of a one-time gift.

Early cash-outs pose another big risk to results. Researchers call these early withdrawals account leakage. Holders gain full control of the money at 18. Many young adults may pull cash for school or a home. In several test cases, that leakage left balances at $0. As a result, timing and discipline shape success as much as returns. Steady savers, by contrast, kept far larger sums by age 55.

Trump Accounts also carry a subtle tax catch. Gains face tax as ordinary income once withdrawn. By comparison, a taxable fund would be subject to lower capital gains rates. So the tax break can prove thinner than it first seems. Families should weigh this rule before they pour in cash.

What Investors Should Watch

Inflation now sits at the heart of this policy fight. Consumer prices rose 4.2% in May 2026. That reading marked the steepest yearly pace since April 2023. Additionally, the war with Iran pushed energy costs sharply higher. Such pressure quietly erodes the real value of long-term savings.

Giving from the wealthy could still tilt results for poorer families. The Michael and Susan Dell Foundation pledged $6.25 billion. That single gift adds $250 to about 25 million young accounts. Employers such as Chipotle and Bank of America have joined, too. The Dalio Foundation has also pledged fresh money to the plan. These top-ups aim to lift the smallest accounts first. Nevertheless, experts stress one steady and sober message. Compounding rewards patience, steady deposits, and honest math over hype.

For many families, other accounts may still deserve first claim. A couple with two kids might fund $100,000 in other plans first. College savings and their own retirement often come before this seed. A 529 plan, for instance, can offer richer perks for school costs.

Trump Accounts still offer a genuine head start for many kids. Yet the smartest savers will read past the bold numbers. They will plan around inflation, taxes, and the long road ahead.