April 21, 2026 – The Middle East conflict has derailed a 3.4% growth trajectory. Trade volumes are nearly cut in half. Inflation is climbing. Yet Wall Street just posted its best quarter in years.

In Summary

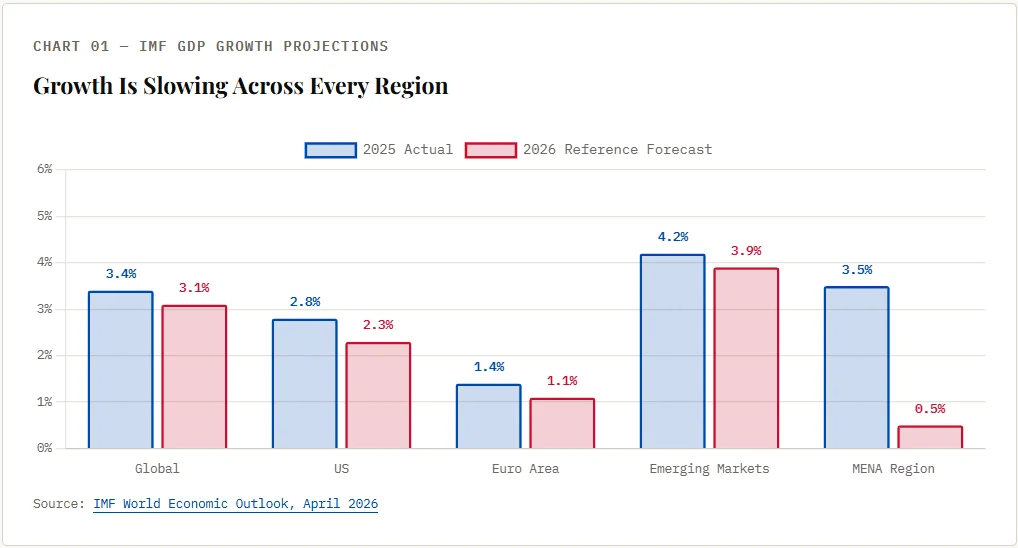

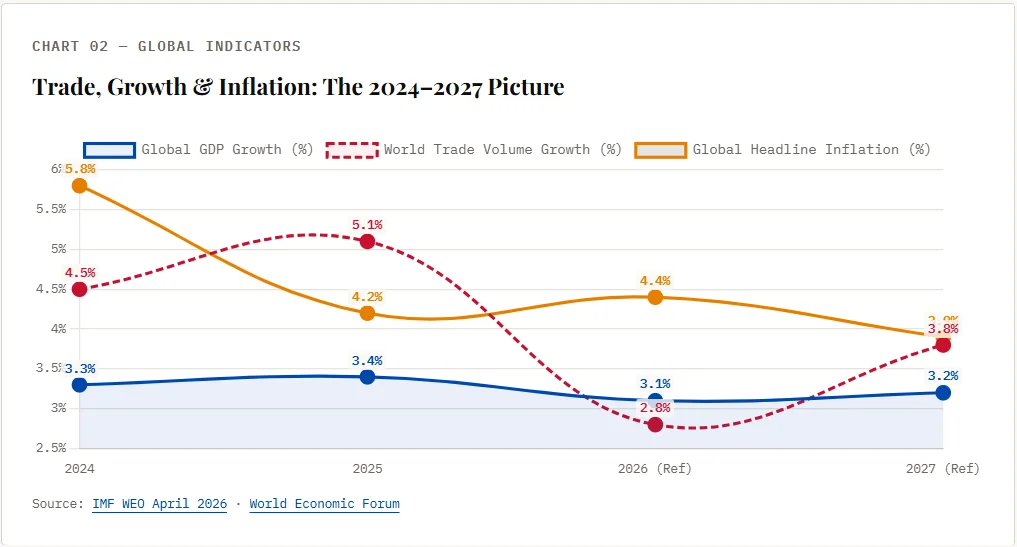

IMF cuts 2026 global growth to 3.1%, down from 3.4% in 2025 and 3.3% in January 2026

World trade volume growth nearly halved: from 5.1% in 2025 to just 2.8% in 2026

Global headline inflation rises to 4.4%, reversing a year-long decline

Defence spending surges by 2.7% of GDP on average; public debt to rise 7+ percentage points

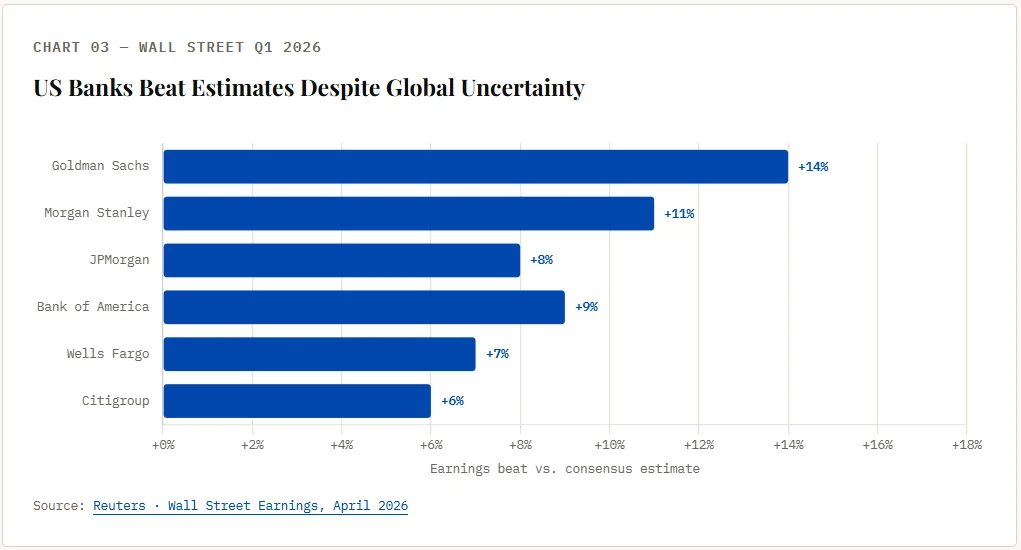

Hedge funds bought a record $86 billion in equities over five trading sessions

The Downgrade, Explained

The International Monetary Fund has issued its starkest assessment of the year. It cut its 2026 global growth forecast to 3.1%. That is down from 3.3% projected in January 2026. It also falls well below the 3.4% growth recorded in 2025.

The driver is clear: war in the Middle East. The IMF’s April World Economic Outlook is titled Global Economy in the Shadow of War. Chief Economist Pierre-Olivier Gourinchas confirmed the conflict “stopped the momentum” of what had been a steady global recovery.

“The global economy was on a steady growth trajectory. The war has stopped that momentum, with inflation rising to 4.4%, a sharp departure from the previous trend.”

— Pierre-Olivier Gourinchas, Chief Economist, IMF · April 14, 2026

The fund constructed a “reference forecast”, not a traditional baseline. It assumes the conflict stays limited in duration and scope. But it also models two darker paths.

Trade Takes the Hit

One number stands out above all others. World trade volume growth drops from 5.1% in 2025 to just 2.8% in 2026. That is a near-halving in a single year.

Three forces are driving this. Energy costs are surging. Shipping routes near the Strait of Hormuz are disrupted. US-China trade friction remains high.

The impact is deeply uneven. Emerging market economies see their 2026 growth forecast cut by 0.3 percentage points. The Middle East and North Africa face a cumulative 3-percentage-point revision. Advanced economies see more modest, though still subdued, adjustments.

Lower-income, energy-importing nations face the sharpest pain. Cumulative growth over 2026–27 is revised down 0.5 percentage points. Their fiscal buffers are thin. Their exposure to higher food and energy prices is large.

The Defence Spending Trap

War is expensive, and not just in lives lost. Military budgets are rising fast. The IMF finds defence outlays are climbing by an average of 2.7 percentage points of GDP. Roughly two-thirds is deficit-financed.

This creates what economists call “fiscal dominance.” Debt obligations begin to constrain monetary policy. Public debt rises by 7 percentage points within three years. In wartime scenarios, that jumps to 14 percentage points. Social spending takes the hit.

The short-term multiplier is close to 1. One dollar of defence spending adds roughly one dollar to output. But that temporary boost fades. The long-term fiscal cost is far larger.

Wall Street Bucks the Trend

While global forecasts darken, major US banks posted Q1 profits above estimates. All six of the largest US lenders beat forecasts. Goldman Sachs reported its best quarter in five years.

Morgan Stanley’s equity traders benefited from surging market volatility. Bank of America saw strong earnings growth. Higher trading revenues drove results across the board.

S&P 500 earnings growth is projected at 12.6% year-on-year. Analysts point to a weaker dollar and supportive fiscal policy as key tailwinds. Corporate America is, for now, proving resilient.

The buying frenzy is equally striking. Hedge funds purchased a record $86 billion in equities over five sessions, per Goldman Sachs data. That is among the fastest accumulation surges ever recorded. Analysts estimate funds could add another $70 billion if peace talks advance.

AI: The Productivity Gap

Artificial intelligence is everywhere in the data, and mostly a cautionary note. Investment in AI infrastructure remains strong. But the IMF warns productivity gains are arriving too slowly to offset current shocks.

The infrastructure bottleneck is real. Nearly 40% of US data centre projects due in 2026 face delays. Permitting hurdles, labour shortages, and power grid strain are the causes. Some projects have already slipped by months.

Regulators add another layer of risk. Senior financial officials warn that advanced AI models could expose weaknesses in banking cyber-defences. The pace of development is outrunning current safeguards. The Financial Stability Board has flagged stretched asset valuations and elevated non-bank financial leverage as amplifying risks.

What to Watch

The IMF’s risk register leans firmly to the downside. A longer or broader conflict could push growth below 2%. New trade tensions would worsen the picture. A reassessment of AI’s productivity upside would remove a key pillar of medium-term optimism.

But positive paths exist. A swift resolution to the Middle East conflict would restore confidence rapidly. Faster-than-expected AI adoption could lift growth. Easing US-China friction would unlock significant trade recovery.

For investors, the signal is mixed but actionable. US banks are thriving on volatility. Hedge fund flows are recovering. But the macro floor is fragile. The global economy is not in crisis, but the margin for error has rarely been this thin.