April 28, 2026 – Prediction markets and CME futures converge on one outcome. The Fed will stand pat on April 29 and likely through the summer. Elevated inflation and a softening jobs market are keeping policymakers frozen.

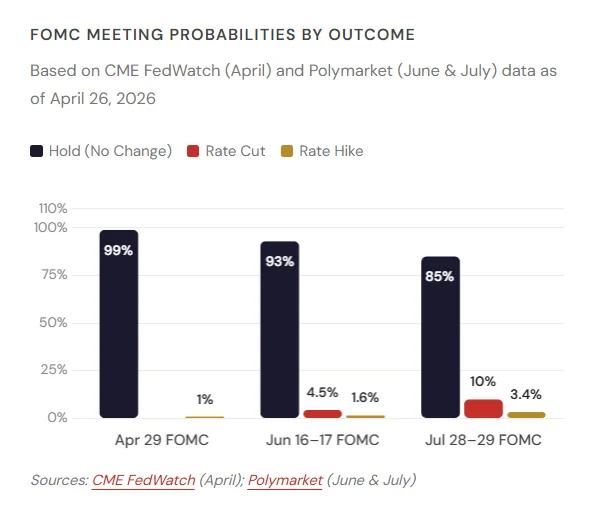

The Federal Reserve will hold interest rates steady on April 29, 2026. That is the near-unanimous view of financial markets. The CME FedWatch Tool puts the probability of a hold at 99%. Just one month ago, there was a 6.2% chance of a rate hike. That hike risk has since vanished entirely.

The current target range sits at 350 to 375 basis points, or 3.50% to 3.75%. The remaining 1% in CME futures reflects a slim possibility of a 25-basis-point hike. There is zero probability of a rate cut at this meeting.

CME FedWatch Signals a Frozen Fed

The CME FedWatch Tool tracks futures contracts tied to the federal funds rate. It reflects real money positions. It is not simply a survey or an opinion poll.

One month ago, some traders hedged against the risk of unexpectedly strong economic data. That concern has since faded. The April 29 FOMC meeting is now a near-foregone conclusion. The CME Tool shows no traders are positioning for a rate cut at this meeting. The consensus has held firm for at least a week.

Traders are not just pricing out an April cut. They are pricing out the entire 2026 easing cycle.

Prediction Markets Confirm the Trend

Prediction markets are telling the same story. Polymarket’s June FOMC contract shows 93% odds for no change. A 25-basis-point cut carries just 4.5% probability. A hike comes in at 1.6%. More than $10.5 million has traded on that single contract.

The July outlook shows slightly more uncertainty. Polymarket puts the hold probability at 85% for the July 28–29 FOMC meeting. A 25-basis-point cut carries 10% odds. The hike probability rises modestly to 3.4%. That market has attracted $3.9 million in trading volume since launching in March 2026.

Kalshi’s parallel July contract closely mirrors these numbers. It places an 84% probability on the Fed holding in July. A 25-basis-point cut carries 12% odds. A hike sits at 4%. Total volume on that Kalshi contract stands at $79,441.

What the Data Says: Inflation and Jobs

The macroeconomic backdrop explains the Fed’s caution. March 2026 CPI came in at 3.3% year-over-year. That figure remains meaningfully above the Fed’s 2% inflation target. Inflation is elevated but not spiralling. The Fed has little justification to move rates in either direction.

On the labour side, the U.S. unemployment rate stands at 4.3%. That is modestly above the historical long-run average. The labour market is softening, but it is not collapsing. These two data points have anchored the Fed’s pause. The dual mandate of price stability and full employment is in a delicate balance.

The 2026 Rate Cut Debate

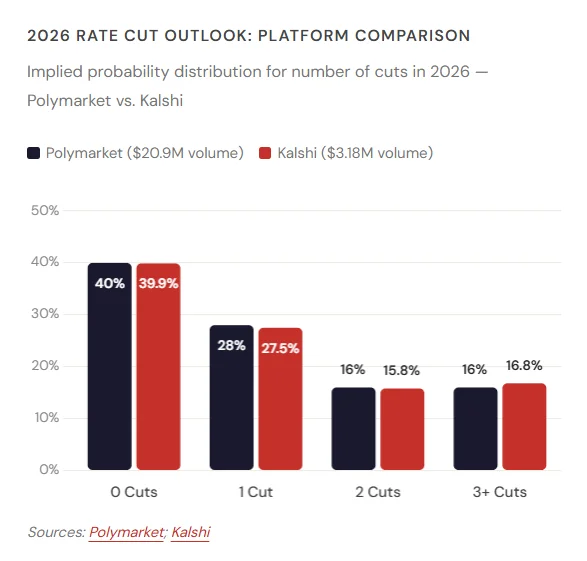

The deeper question is whether any cuts will arrive in 2026 at all. Polymarket’s annual rate-cut market has generated $20.9 million in trading volume since launching in September 2025. The leading outcome is zero cuts, priced at 40%. One cut follows at 28%. Two cuts carry just 16% odds.

Kalshi’s equivalent annual market echoes that view. Zero cuts lead at 39.9%. One cut stands at 27.5%. Two cuts are priced at 15.8%. Kalshi’s contract has attracted $3.18 million in total volume. Together, these figures paint a unified picture.

What to Watch Next

Two events could shift these market probabilities. The first is the April jobs report. A sharp rise in unemployment could quickly revive cut expectations. The second is the May CPI reading. A sustained drop toward 2% would meaningfully change the policy calculus.

Until either of those numbers arrives, the market’s base case holds firm. The Federal Reserve stays on hold. Rate cuts remain a distant prospect for 2026. The April 29 FOMC meeting is expected to confirm what traders have already priced in.