July 02, 2026 – Fed Chair Kevin Warsh is pushing markets toward a tougher regime. Investors now get fewer hints, more data risk, and a sharper inflation test.

In Summary

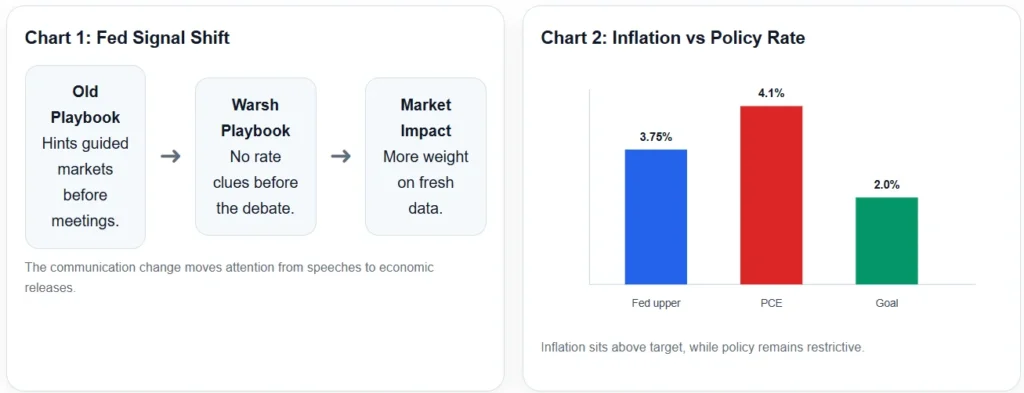

Warsh said he will not provide Fed forward guidance.

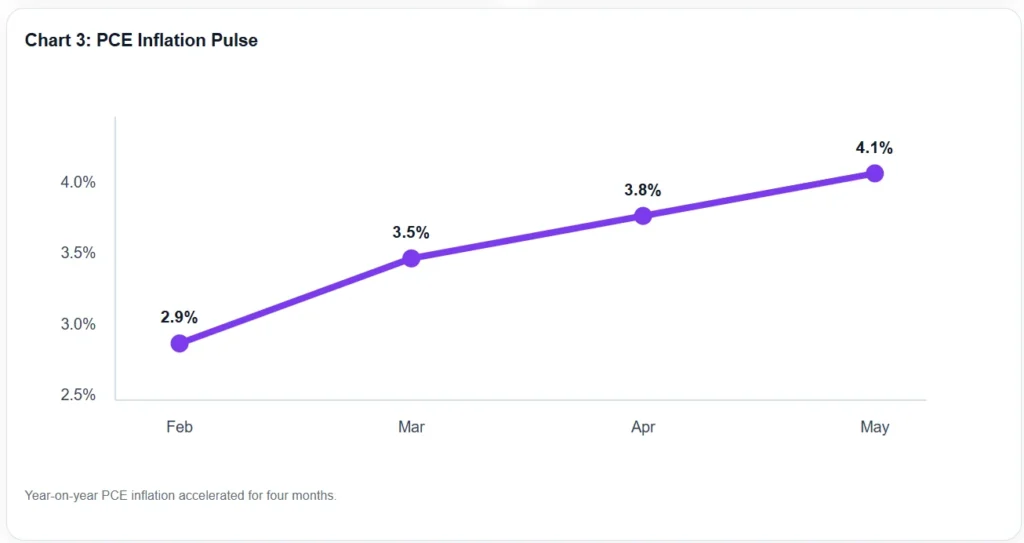

The Fed held rates at 3.50 percent to 3.75 percent in June.

May PCE inflation reached 4.1 percent, above the 2 percent goal.

Markets may face higher rate volatility before each Fed meeting.

Investors should track inflation, jobs, and real-time demand signals.

Fed forward guidance is no longer the market comfort blanket. Kevin Warsh used his latest public appearance to repeat a simple message. He will not tell investors where rates are likely to go next. Instead, he wants markets to make their own judgments based on real economic data.

That shift matters because it changes how traders price every inflation print, payroll report, and policy speech. Warsh said he is not going to give forward guidance. He also stressed that the Fed will stay committed to its 2 percent inflation objective.

Why Warsh Is Changing The Fed Signal

Forward guidance became a powerful tool after the global financial crisis. It helped central banks steer markets when interest rates sat near zero. However, Warsh argues that today’s economy needs a different playbook.

The new approach is data-first. It gives policymakers more freedom before meetings. It also reduces the chance that markets treat every speech as a promise. Therefore, the Fed may become less predictable by design.

This does not mean policy has become random. It means the reaction function carries more weight. If inflation stays hot, the risk of rate hikes can rise quickly. If growth breaks, markets can reprice quickly in the other direction.

The Rate Backdrop Is Still Tight

The Fed kept the federal funds target range at 3.50 percent to 3.75 percent at its June meeting. The vote was 12 to 0. The statement also said inflation remains elevated versus the 2 percent goal.

That matters for risk assets. A no-guidance Fed can raise volatility in bonds, equities, crypto, and the dollar. Investors lose the old map. As a result, each macro release becomes a mini policy event.

Markets continued to search for clues after Warsh spoke. Traders were reported to price a 70 percent chance of a September rate hike. That suggests investors heard a hawkish tone, even without explicit guidance.

Inflation Is The Core Problem

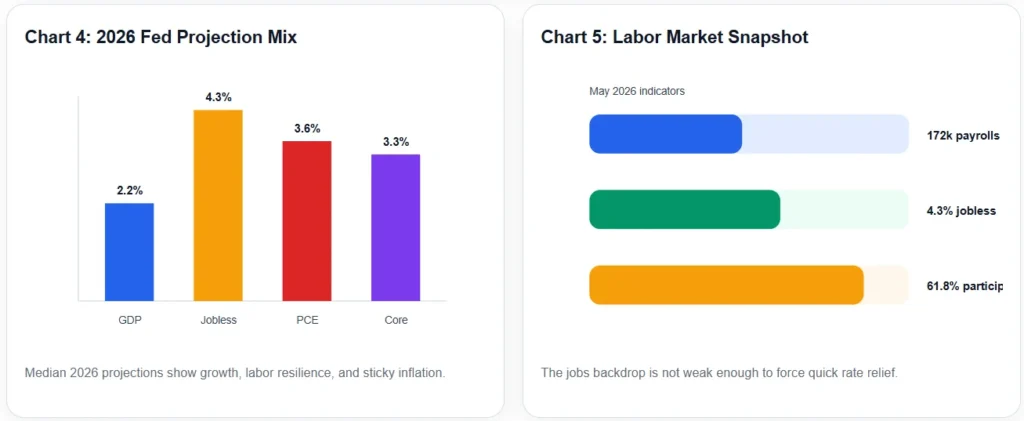

The inflation data explains Warsh’s caution. The PCE price index rose to 4.1 percent in May. It stood at 2.9 percent in February. The move shows a sharp loss of disinflation momentum.

Core pressure also remains uncomfortable. The broader trend tells the Fed that supply shocks and service costs still matter. Therefore, an early easing signal would risk loosening financial conditions too soon.

The June projection materials added to that concern. Policymakers placed 2026 median PCE inflation at 3.6 percent. They also projected core PCE inflation at 3.3 percent. Both numbers sit well above target.

Jobs Give The Fed Room

The labor market does not look broken. May payrolls increased by 172,000 jobs. The unemployment rate held at 4.3 percent. Participation also stayed at 61.8 percent.

Those figures reduce pressure for immediate rate cuts. They also support Warsh’s message that policy should wait for incoming data. However, the labor market still needs close monitoring. Long-term unemployment and hiring breadth can weaken before the headline rate moves.

What It Means For Markets

The immediate market impact is a higher uncertainty premium. Traders can no longer lean on carefully staged comments. Consequently, curves may react more violently to one strong inflation print.

This matters for the dollar. A data-first Fed can support the currency when inflation surprises to the upside. It can also weaken the dollar if growth data cracks. The message is not permanently hawkish. Instead, it is conditional and deliberately flexible.

Crypto and growth equities face the same issue. Liquidity expectations can change before prices adjust to earnings or adoption data. Therefore, risky assets may trade more like macro instruments during Fed-heavy weeks.

Why Real-Time Data Matters

Warsh also wants faster policy intelligence. He said the Fed should rely more on real-time data and less on backward-looking surveys. That goal fits an economy shaped by AI investment, energy shocks, and faster capital flows.

The challenge is execution. Real-time data can detect turning points earlier. However, it can also create noise. A central bank that speaks less must still explain its decisions clearly after each meeting.

What Investors Should Watch Next

Warsh’s Fed has made the next stage clearer, but not easier. The market must now watch the data calendar more closely. PCE inflation, wage growth, jobless claims, and oil prices will matter more than policy hints.

For bond traders, this means term premiums can stay jumpy. For equity investors, discount rates may move sharply around releases. For crypto markets, liquidity expectations may swing faster than before.

The biggest takeaway is simple. Fed forward guidance is fading as a policy crutch. In its place, Warsh wants a central bank that speaks less and reacts more. That creates a cleaner policy framework. However, it also creates a tougher trading environment.

If inflation keeps running above target, the Fed can hold or hike without preparing markets first. If inflation cools quickly, the same data-first framework can turn less restrictive. Until then, investors should expect fewer hints and bigger reactions.