May 13, 2026 – Banks enjoyed falling funding costs through 2025. Now, a historic FOMC vote split, rising Gen Z churn, and AI-powered rate hunting are rewriting the deposit competition playbook.

In Summary

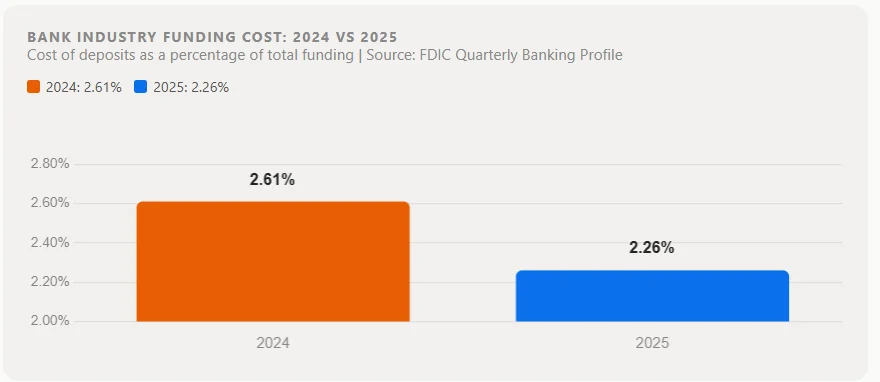

Bank funding costs fell from 2.61% (2024) to 2.26% (2025) per FDIC data, but the relief is plateauing.

The April 29 FOMC voted 8-4 to hold rates, the most divided since October 1992, adding policy uncertainty.

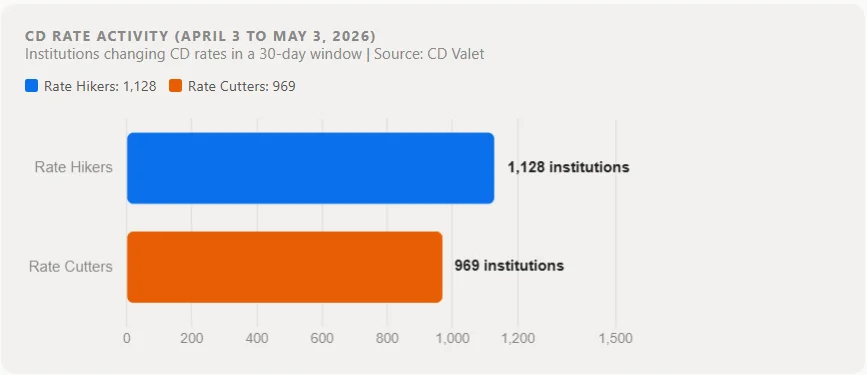

Between April 3 and May 3, 1,128 institutions raised CD rates versus 969 that cut them.

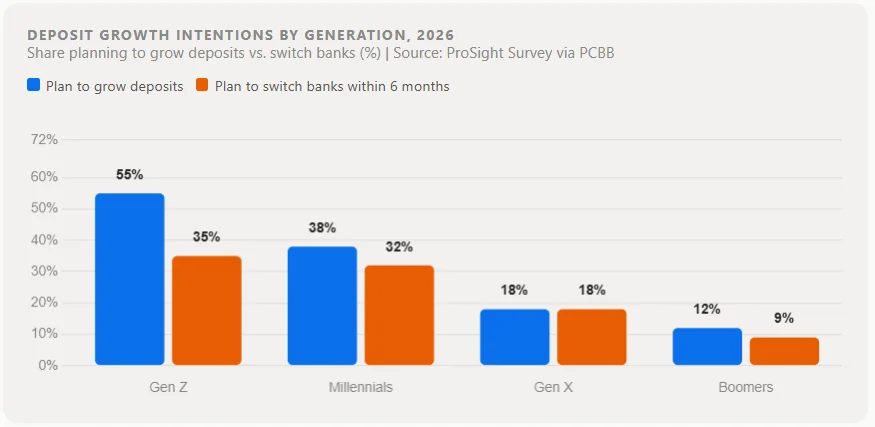

Gen Z leads deposit growth intentions: 55% plan to grow deposits in 2026, but 35% also plan to switch banks.

AI tools are accelerating rate-hunting behavior among savers, raising churn risk across all age groups.

The Federal Reserve’s April 29 FOMC meeting produced the most divided policy vote in over three decades. The committee held rates at 3.5% to 3.75%. But four officials dissented, for different reasons. That fracture signals prolonged uncertainty. With Kevin Warsh set to become Fed chair on May 15, rate policy is entering uncharted territory. Banks cannot count on near-term relief. The fight for deposits is intensifying on multiple fronts.

⚠ Policy Alert

The April 2026 FOMC 8-4 vote is the most divided since October 1992. One member pushed for a cut. Three others opposed any future cut in language. This split leaves the rate path deeply uncertain for the rest of 2026.

The Funding Cost Relief Is Fading

The FDIC’s Quarterly Banking Profile shows the industry’s funding cost fell from 2.61% in 2024 to 2.26% in 2025. Three Fed rate cuts in late 2024 enabled banks to quickly reprice deposits. That improvement was swift and meaningful. But analysts say the window is now largely closed.

“Banks have done a really strong job capturing the repricing tailwind. The incremental is hard, and you heard it from most every bank this quarter.”

-Christopher McGratty, Head of US Bank Research, Keefe Bruyette and Woods

Rohan Shah of Simon-Kucher says funding costs are likely to “plateau” if the Fed holds steady. Larger banks may absorb this better. Their branch networks and product suites attract customers beyond rate offers alone. Rate competition, Shah advises, is ultimately a losing strategy. Building sticky, multi-product relationships is the more durable path.

CD Battles Heat Up Across the Sector

CD Valet tracks yields across thousands of lenders. Between April 3 and May 3, 1,128 institutions raised CD rates. In that same period, 969 cut them. That 159-institution gap shows the clear direction of travel. The median 12-month APY stood at 3.19% on May 5, down from 3.5% one year earlier. Some lenders still offer yields above 4%.

Research from the Federal Reserve Bank of Dallas finds that depositors are primarily seeking better rates rather than measures of bank-specific risk. In 2026, the Dallas Fed notes, banks may have more success advertising high rates than high capital ratios. Deposit consultant Neil Stanley of The CorePoint agrees. AI tools are making rate comparison faster and easier. In a 3.5% rate world, no responsible saver should accept near-zero interest on their cash.

The Gen Z Deposit Wildcard

A new front is opening in the deposit wars: generational competition. Younger depositors represent the largest growth opportunity in 2026. But they also bring the highest risk of switching. According to a ProSight survey reported by PCBB, 55% of Gen Z consumers expect to increase deposits in 2026. That compares with 38% of Millennials. Gen X and Boomers were far more subdued in their intentions.

Yet the same cohort carries serious churn risk. Some 35% of Gen Z and 32% of Millennials plan to switch their primary bank within the next six months. Promotional money market accounts tripled for Millennials and doubled for Gen X in the past six months. Promotions attract younger savers. But without a built-in retention strategy, those gains evaporate quickly.

The digital dimension matters here. Some 86% of Gen Z use mobile banking monthly. Only 14% of Gen Z trust traditional banks “a lot.” Digital-only banks saw 37% year-over-year growth in their Gen Z user base in 2025. Winning this cohort requires a mobile-first experience, personalized offers, and a seamless account-opening process. A competitive rate is necessary but not sufficient.

Non-Interest Deposits Settle at a New Level

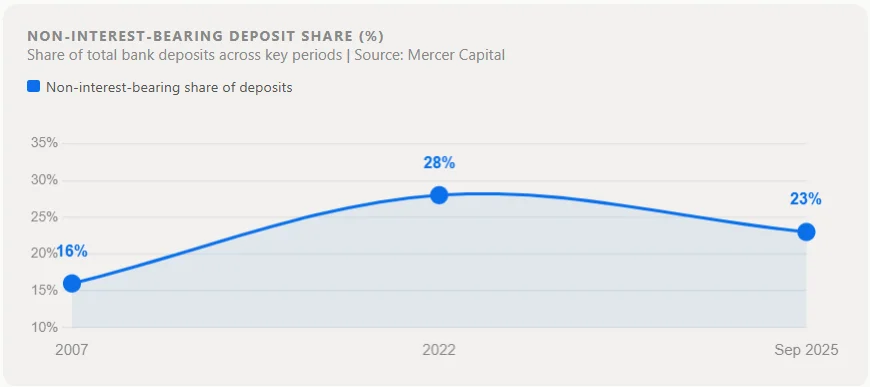

Mercer Capital’s analysis shows that non-interest-bearing deposits accounted for just 16% of all deposits in 2007. The post-2008 low-rate era pushed that share to 28% by 2022. Banks were flush with cheap, passive funding. The Fed’s post-pandemic rate hikes sharply reversed that trend. The share fell to roughly 23% by September 2025.

Analysts at KBW believe this mix has now reached a stable floor. Fitch Ratings senior director Theresa Paiz Fredel describes it as a “new steady state.” Consumers and businesses will always need on-demand deposits for day-to-day transactions. That baseline is unlikely to vanish. Fitch’s Mark Narron adds that the pressure has led to greater credit discipline across the sector.

Bank Executives Are Already Bracing

Regional bank leaders are not waiting to see how this plays out. East West Bancorp CFO Christopher Del Moral-Niles told analysts that deposit pricing pressure is “real and coming.” The $82.9 billion-asset Pasadena-based lender views a no-cut Fed outlook as a direct threat to margins.

WaFd, a $27.6 billion-asset Seattle bank, reports competition for low-cost deposits is “robust and growing.” People’s Bancorp CEO Tyler Wilcox summed up the community bank stance bluntly: “We do not chase stupid.” The bank stays focused on margin protection over volume.

Bank Director’s 2026 State of Commercial Banking analysis adds further context. Deposit growth outpaced commercial and industrial loan growth in 2025. That left many institutions with excess liquidity but intensified competition for quality borrowers. Spread compression is now visible across both floating- and fixed-rate credits.

The Silver Lining in the Loan Market

The picture is not entirely bleak. Loan demand is growing strongly. Banks are partly competing for deposits to fund that expansion. Higher long-term yields mean new loans generate strong interest income. That provides a meaningful cushion against rising funding costs.

“It is a good lending environment,” McGratty said. “Banks can make a decent amount of money in this kind of yield curve.” Some 82% of banks expect to grow deposits in 2026. Growth remains the dominant goal. But execution now requires genuine discipline and a stronger strategy around customer retention.

Bottom Line

The Fed’s rate pause is refiring bank deposit competition on multiple fronts. The historic 8-4 FOMC vote deepens policy uncertainty. Gen Z brings deposit growth but also record switching intent. AI tools are training savers to automatically chase the best rate. Winners will be lenders who compete on relationships, digital experience, and product depth, not rate alone.