July 09, 2026 – The Strive chief points to the 200-week moving average as the floor. His firm’s SEC filings show a treasury built to wait out the storm.

In Summary

Strive CEO Matt Cole sees the Bitcoin bottom forming near the 200-week moving average.

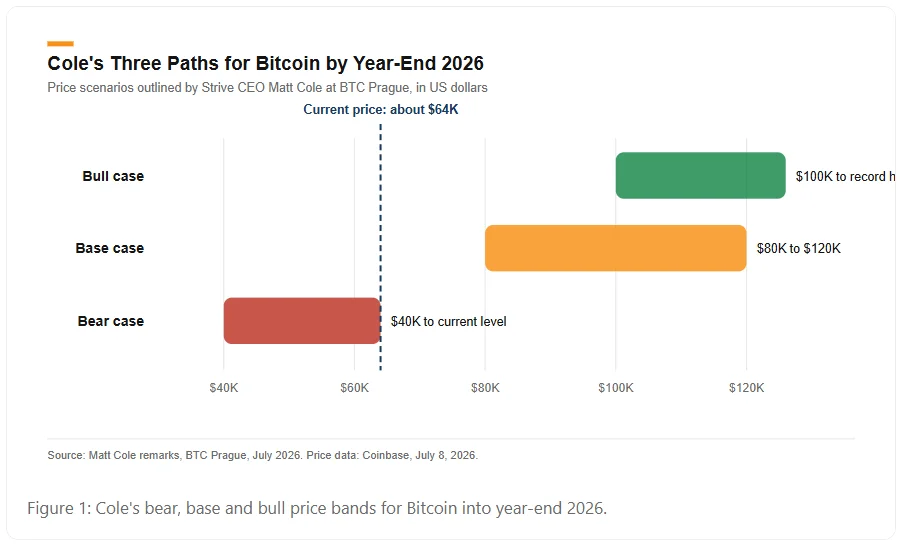

His base case calls for $80,000 to $120,000 by year-end 2026.

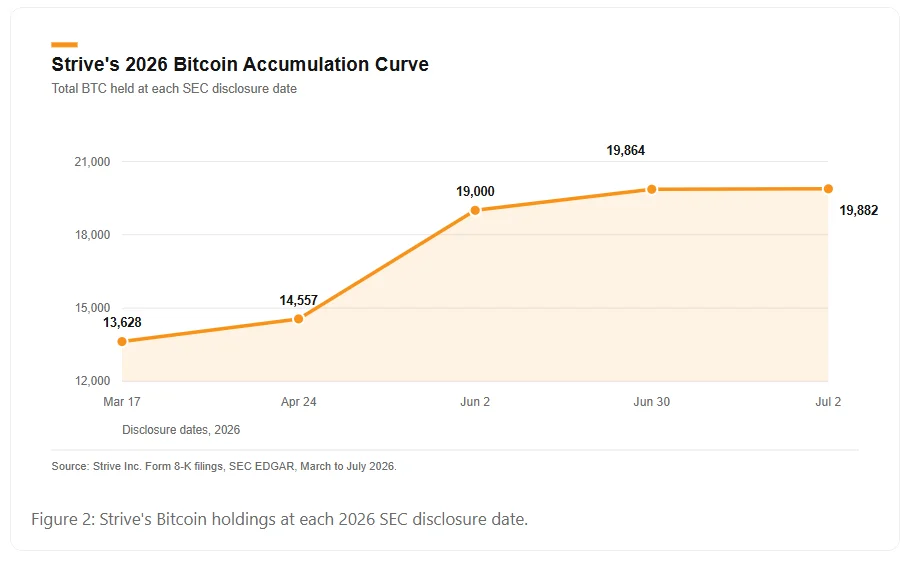

SEC filings show Strive holds 19,882 BTC, the seventh-largest corporate treasury.

Cole bought the 32 coins Strategy sold and calls altcoins overvalued.

Strive Inc. chief executive Matt Cole believes the Bitcoin bottom has likely already formed. Speaking at the BTC Prague event, he set a base case of $80,000 to $120,000 by year-end. Moreover, he called the zone near the 200-week moving average the best place in history to take risks.

His view carries real weight because Strive has real money on the line. According to a July 6 SEC filing, the Dallas-based firm holds 19,882 Bitcoin. As a result, it now ranks as the seventh-largest corporate Bitcoin treasury in the world. Cole also managed about $70 billion in bonds at CalPERS before joining Strive. The timing gives his call extra bite, since Bitcoin trades at roughly half its record high.

Why Cole Says the Bitcoin Bottom Is In

Cole framed his year-end outlook around three clear paths. First, his bear case puts Bitcoin between current levels and $40,000. He called that outcome unlikely but real. Second, his base case sits between $80,000 and $120,000. Finally, his bull case runs from $100,000 toward fresh all-time highs.

History anchors this framework. Bitcoin currently trades near $64,000, close to its 200-week moving average. Past touches of that trendline in 2015, 2018 and 2022 marked major cycle lows. Therefore, Cole argues that buyers near this level have caught the best long-term entries in each cycle.

A Treasury Built to Survive a Crash

Strive built its balance sheet for exactly this kind of slump. The company reported $153.4 million in cash as of July 2. In addition, it holds Strategy preferred shares worth about $44.4 million. Cole says these reserves cover 18 months of costs, even if Bitcoin falls to $40,000 through 2027.

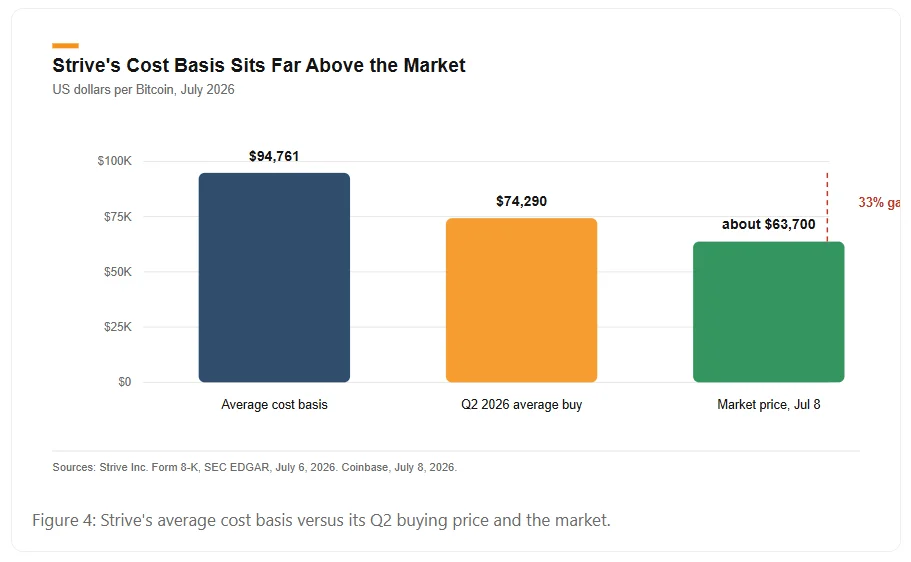

The buying pace has also stayed fast despite falling prices. During the second quarter alone, Strive bought 6,236 Bitcoin at an average cost of $74,290 per coin. So its total stack grew by almost 46 percent in three months. Its average cost basis is $94,761 per Bitcoin, well above the current market price.

The same filing shows a 24 percent Bitcoin yield for the quarter. That metric tracks the number of coins held per diluted share. So shareholders gained coin exposure even while the dollar value of the stack fell.

The 32 Coins That Sparked a Debate

Strategy, the largest corporate Bitcoin holder, sold 32 Bitcoin in late May to fund preferred dividends. That sale, the company’s first since 2022, rattled parts of the market. However, Cole rejected the bearish reading and bought the same 32 coins that week. He then publicly told Chairman Michael Saylor that those coins would cost more to buy back later.

Furthermore, Cole noted that the sale looked tiny relative to Strategy’s own buying. The firm bought 24,869 coins for $2.01 billion in a single week in May, per its SEC filing. Strategy therefore stayed a heavy net buyer during the month of its headline-grabbing sale. “Those fears are going to age really poorly,” Cole said.

Bearish on Everything Except Bitcoin

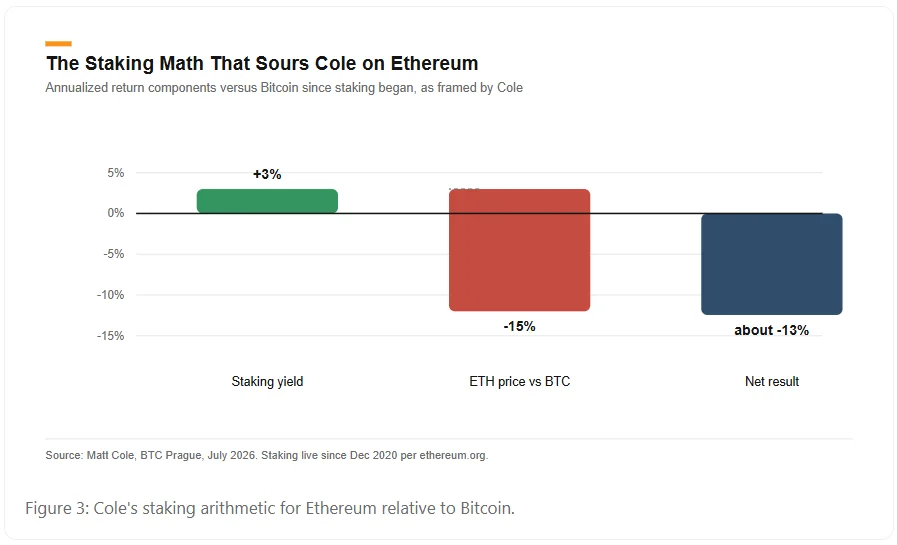

Cole offered no such hope for the rest of the crypto market. He called Ethereum, Solana and other altcoins “insanely overvalued” at current prices. Notably, he argued the popular staking yield thesis fails on simple math.

Ethereum staking went live with the Beacon Chain in December 2020. Since then, Cole says, Ethereum has lagged Bitcoin by about 15 percent per year. A 3 percent staking yield cannot offset a 15 percent yearly price slide, he explained. In effect, the net return works out to roughly minus 13 percent a year. For that reason, he views leveraged altcoin treasury firms as bigger bets on a losing trade.

Digital Credit’s Trillion-Dollar Horizon

Beyond price targets, Cole sketched a larger structural thesis. He expects digital credit, meaning Bitcoin-backed yield products, to grow into a multi-trillion-dollar asset class by 2030. Strive’s own SATA preferred stock anchors that bet. The security pays cash dividends every business day at a 13 percent yearly rate.

Demand for that yield has funded most of Strive’s Bitcoin buys this year. Interestingly, Cole said the average SATA buyer is around 60 years old with a net worth in the low millions. These investors want steady income first, not direct coin exposure. In other words, digital credit turns cautious retirement money into demand for corporate Bitcoin.

What the Numbers Say

The market still has to close a wide gap before Cole’s base case lands. Bitcoin must rise about 25 percent to reach $80,000 and nearly 88 percent to touch $120,000. Meanwhile, Strive’s own stack sits about 33 percent underwater against its average cost. Skeptics will also note that treasury bosses rarely publish bearish calls on their core asset.

Still, the framework is testable and refreshingly precise. Cole attached odds, price bands and a clear failure level to his call. Few Wall Street forecasts offer that much to shoot at. His floor thesis rests on a single line on a single chart, which anyone can track. A weekly close far below that trendline would break the pattern he cites. By December, the 200-week moving average will either confirm his thesis or bury it.