July 14, 2026 – The company raised $466.7 million in stock and bought no bitcoin. Instead of coins, the cash went into a reserve that pays its preferred dividends.

In Summary

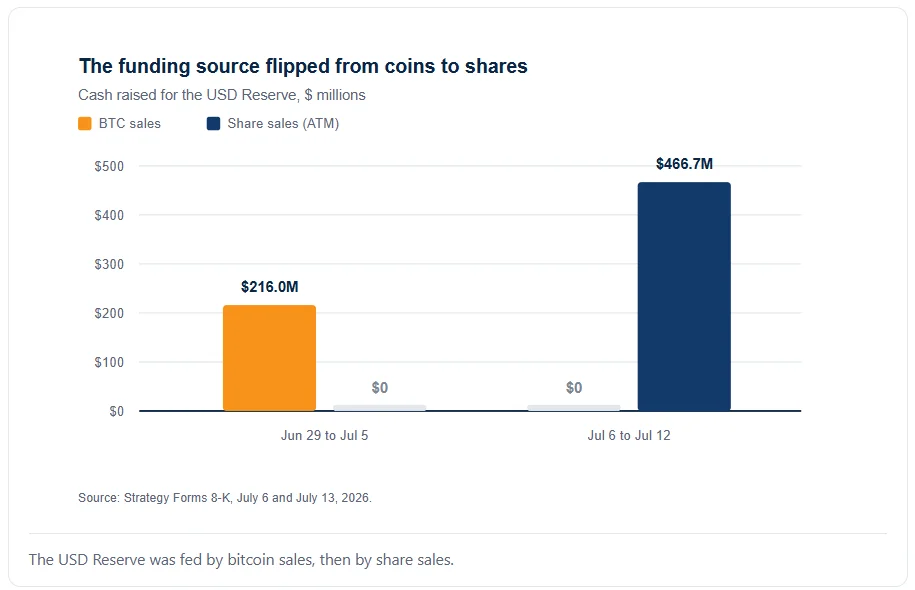

Strategy raised $466.7 million by selling 4,818,781 common shares, and bought no bitcoin.

Holdings stayed flat at 843,775 BTC, ending two weeks in which it sold 3,588 coins.

The USD Reserve climbed to $3.0 billion, a jump of nearly 18% in one week.

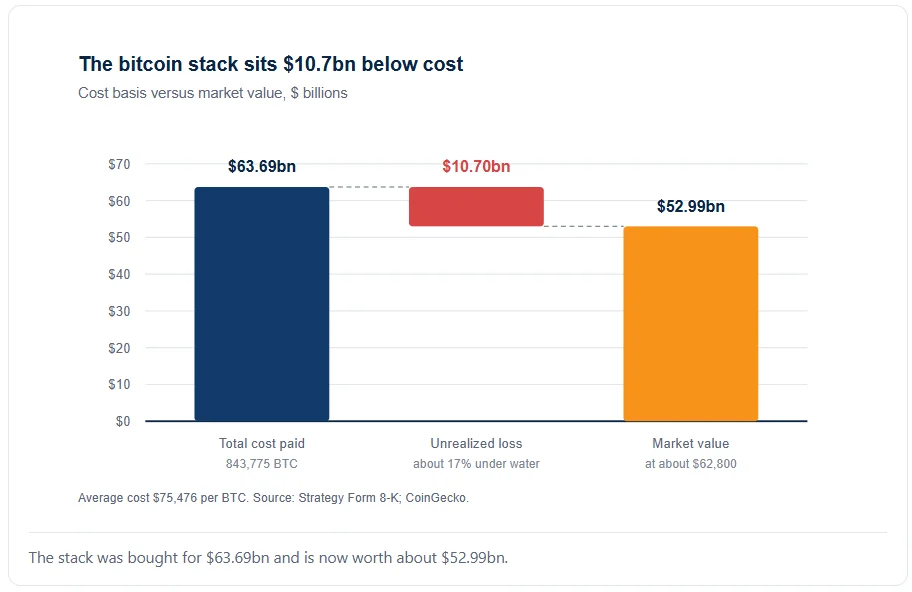

At about $62,800 a coin, the stack sits roughly $10.7 billion below its $75,476 average cost.

The $1.25 billion bitcoin sale facility remained fully undrawn, and no buybacks occurred.

A flat week that hides a sharp turn

Strategy bitcoin holdings ended last week flat at 843,775 BTC. Yet the firm still raised $466.7 million. It sold 4,818,781 Class A common shares through its at-the-market plan. Moreover, it sent every dollar into cash, not coins. Its USD Reserve now sits at $3.0 billion.

But that flat count hides the real turn. Two weeks back, Strategy was a seller. It sold 1,363 BTC on June 29 and June 30. Then it let go of 2,225 more coins from July 1 to July 5. Those sales raised about $216 million in all.

So last week marked a stop, not a lull. Strategy swapped coin sales for share sales. It also left its bitcoin sale facility fully unused.

Why the cash source matters

The USD Reserve does one job. It pays preferred dividends and interest on debt. Four preferred series now trade on Nasdaq. They carry coupons from 8% up to 12%. So the cash drain runs every month, regardless of what Bitcoin does.

In June, the board lifted the STRC dividend rate to 12%. That change took effect for record dates from July 1. Thus, the monthly bill grew just as Bitcoin fell. Timing, in other words, made the squeeze worse.

Paying that bill with coins creates a nasty loop. The stack has an average cost of $75,476. Any sale below that mark locks in a loss. Indeed, the recent sales cleared near $59,256 and $60,773. Meanwhile, new shares avoid that loss on the books.

The dilution trade-off

Shares are not free money, though. The firm minted 4.82 million of them in five sessions. Net proceeds imply about $96.85 per share after fees. So current holders took dilution to pay a dividend bill.

Once, Strategy sold stock mainly to buy more bitcoin. That engine worked while shares traded well above net asset value. Each raise then lifted Bitcoin per share. But the premium has thinned sharply this year. Now fresh stock pays bills instead of growing the stack.

There is a further twist here. On June 29, the board cleared $2 billion of buybacks. That plan covers $1 billion of common stock. Two weeks later, the firm sold common stock instead. It brought back nothing at all.

The gap between those two plans looks stark. Buybacks shrink the share count, while ATM sales swell it. Consequently, the firm leaned against its own authorisation. Cash needs, quite simply, won the argument.

A $10.7 billion paper hole

The math is harsh. Strategy paid $63.69 billion for its bitcoin. At about $62,800 a coin, the stack is worth nearly $53 billion. So the paper loss runs to roughly $10.7 billion. In short, the trade sits about 17% underwater.

The books already show the pain. For the June quarter, Strategy booked an $8.32 billion loss on digital assets. It also carried $49.67 billion of digital assets as of June 30. Because cost topped fair value, the firm set aside a valuation allowance. That step wiped out the linked deferred tax asset in full.

Such losses do not drain cash on their own. Yet they shrink the equity base. Furthermore, they make each new share harder to sell.

How the reserve grew

The reserve stood at $2.55 billion on July 5. One week later, it reached $3.0 billion. That is a jump of nearly 18% in five sessions. Almost all of it came from the share sale.

Strategy frames the reserve as a shield. It covers dividends and interest without touching a single coin. Therefore, preferred holders gain comfort, and Bitcoin stays put. Common holders, however, foot the bill. Anyone can track the balance on the company dashboard.

Dry powder still on the shelf

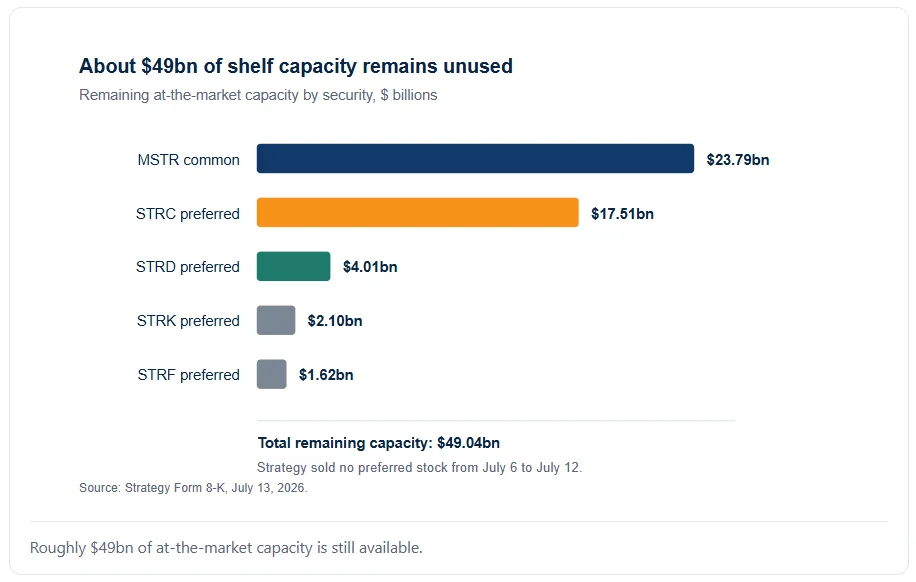

Strategy still has room to move. Its common ATM shows $23.79 billion of space left. The four preferred plans hold about $25.24 billion more. Altogether, roughly $49 billion of shelf capacity stays live.

Yet the firm sold no preferred stock last week. It used the common tap alone. That choice hints at where demand looks strongest.

Liquidity looks fine for now. The $3.0 billion reserve sits beside $1.25 billion of unused sale capacity. Together, they provide about $4.25 billion in coverage.

How the market reads it

MSTR shares slipped about 3% before Monday’s open. Bitcoin also drifted lower over the weekend. It traded near $62,800 as the filing landed. Thus, traders saw no rescue in the news. Cash, after all, does not compound like coins.

What the pivot signals

Michael Saylor built the firm on a plain vow. Bitcoin went in, and none came out. June broke that vow. July has now bent it again.

Read the order of events with care. First, Strategy sold coins to pay dividends. Next, it stopped and diluted holders instead. Both moves fix the same cash gap. Yet each one shifts the cost to a different group.

Three signals to watch

Watch the Bitcoin sale facility first. Any draw on it would suggest that stock buyers have stepped back. Second, track the preferred taps, since STRC alone holds $17.51 billion of room. Third, follow Bitcoin against the $75,476 cost line.

A firm move above that line would revive the old growth story. But a long slump would force harder calls. For now, Strategy buys time with shareholder equity. The clock keeps running.