June 30, 2026 – A new Bitcoin monetization strategy plan allows up to $1.25 billion in BTC sales. The price still sits below cost.

In Summary

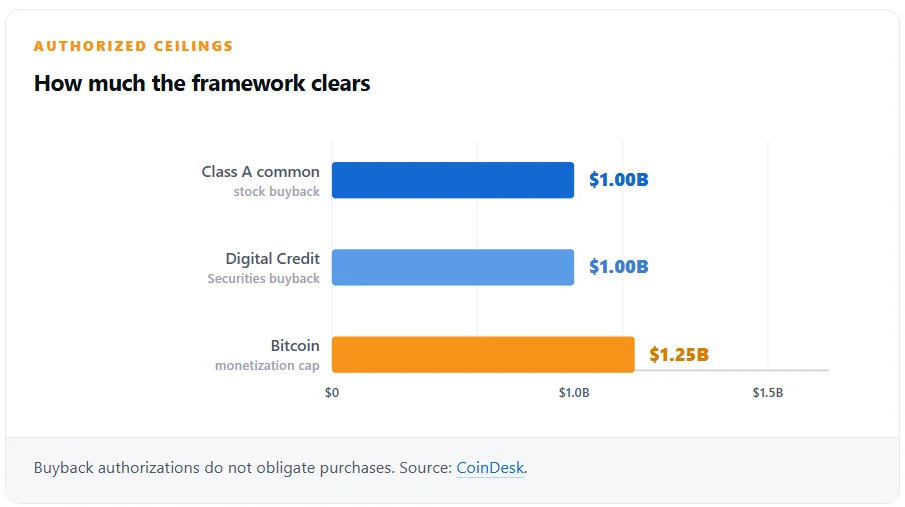

Strategy approved up to $2 billion in common stock and preferred security buybacks.

A new program permits up to $1.25 billion in Bitcoin sales for reserves and dividends.

Bitcoin trades near $59,800, roughly 21% below the firm’s $75,651 average cost.

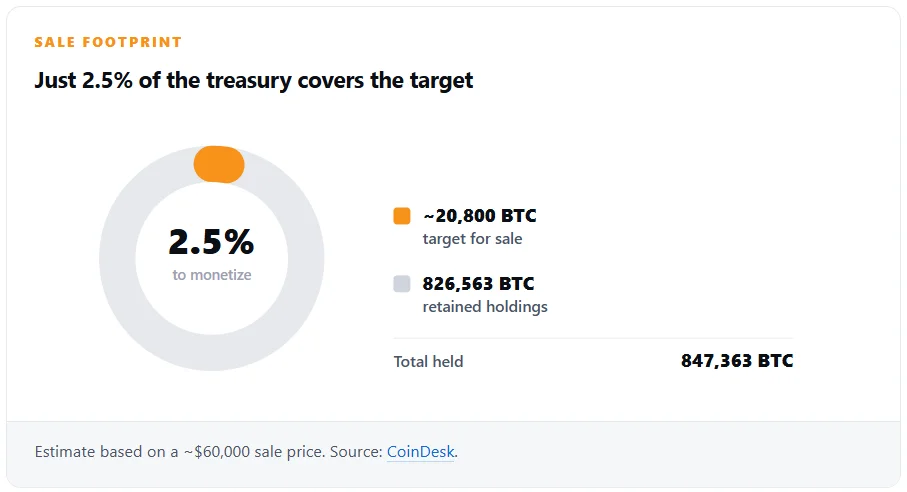

Raising the full target would need about 20,800 BTC, just 2.5% of holdings.

Strategy shifts from holding to managing Bitcoin

Strategy has launched a Bitcoin monetization plan that reshapes how it runs its treasury. The software firm, formerly known as MicroStrategy, revealed the program on Monday. Its new Digital Credit Capital Framework authorizes up to $2 billion in buybacks. Furthermore, it opens the door to up to $1.25 billion in Bitcoin sales.

Michael Saylor framed the move as discipline rather than retreat. He said the company stays committed to Bitcoin as its main reserve asset. However, he added that digital credit now demands active capital management. Therefore, the board built tools to raise cash when conditions favor it.

What the framework approves

The board cleared two separate buyback tracks. First, it authorized up to $1 billion for Class A common stock. Second, it approved up to $1 billion for Digital Credit Securities. Neither program forces the company to act. Instead, management will buy only when purchases look accretive.

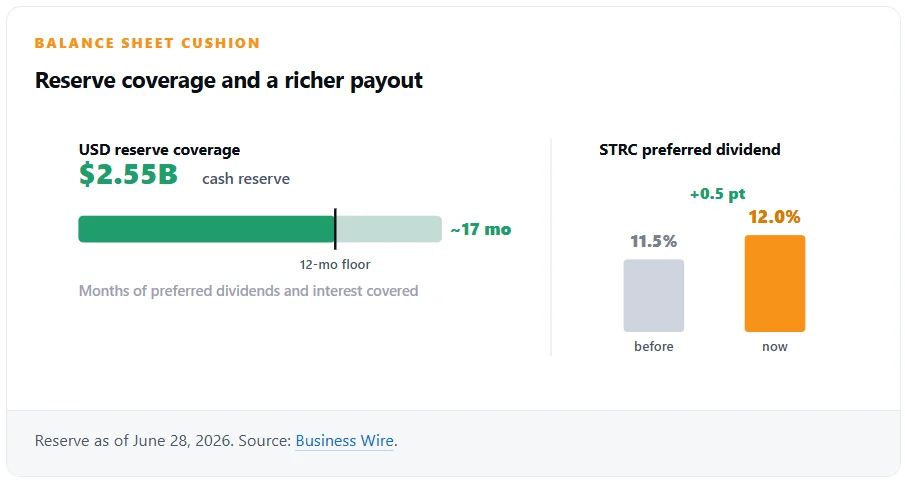

The monetization program adds a third lever. Strategy may sell coins to fund its dollar reserve, dividends, or buybacks. Moreover, any sale beyond those goals needs fresh board approval. The reserve policy also sets a firm rule. Strategy must hold at least 12 months of dividend and interest cover.

Why selling below cost matters

The timing carries real weight. Bitcoin traded near $59,800 on June 29, well under Strategy’s average entry. The firm holds 847,363 BTC bought for about $64 billion. That equals roughly $75,651 per coin. Consequently, the treasury now sits about 21% underwater.

At current prices, the paper loss approaches $13 billion. Selling now would therefore crystallize losses on any coins sold. Even so, the framework hands Strategy the flexibility it previously lacked.

The market has pressured the stock, too. Strategy’s enterprise value recently slipped below its net asset value. That rare gap signals cooling investor enthusiasm. Furthermore, it weakens the firm’s ability to issue accretive equity. Cash from Bitcoin sales can now replace some of those raises.

A small slice of a large stash

The potential sales look modest against total holdings. To raise the full $1.25 billion, the company would sell about 20,800 BTC. That figure represents only 2.5% of its reserve. As a result, the plan preserves the bulk of its long-term exposure.

Dividends, reserves, and market reaction

Strategy also strengthened its income commitments. The board lifted the STRC preferred dividend to 12%, up from 11.5%. Meanwhile, its USD reserve reached $2.55 billion as of June 28. That cushion covers roughly 17 months of preferred dividends and interest.

Investors welcomed the news quickly. MSTR shares climbed between 3% and 7% after the announcement. Additionally, the company raised about $1.15 billion through its at-the-market equity program. It sold 12.67 million Class A shares during the reporting week. Notably, it bought no new Bitcoin in that period.

These steps aim to reassure preferred shareholders. A higher payout and a cash floor support credit quality. In turn, that should steady demand for future offerings.

What it signals for corporate treasuries

The framework marks a clear evolution in Saylor’s playbook. For years, Strategy mostly bought and held. Now it treats Bitcoin as a working capital tool. This pivot also follows a tougher market backdrop. Bitcoin has slid sharply since mid-June amid heavy ETF outflows.

The shift matters because Strategy long modeled the buy-and-hold treasury thesis. Other firms copied that template during the last bull run. Therefore, a move toward active selling could ripple across the sector. Smaller treasury companies may face tougher questions about their own cushions.

Critics still question whether the model adds lasting value. Supporters counter that flexibility protects the dividend and the credit profile. Either way, the plan gives Strategy room to defend its balance sheet.

Analysts will watch the cadence closely. A single small sale could calm nerves. A larger one might unsettle the wider market. After all, Strategy ranks as the largest corporate Bitcoin holder. Its trades therefore move sentiment far beyond its own books. The next weekly filings should reveal whether it acts. For now, the option exists, yet the trigger stays unpulled.