May 27, 2026 – Michael Saylor’s firm paused BTC purchases to retire $1.5B in convertible notes at a discount. The playbook is shifting.

In Summary

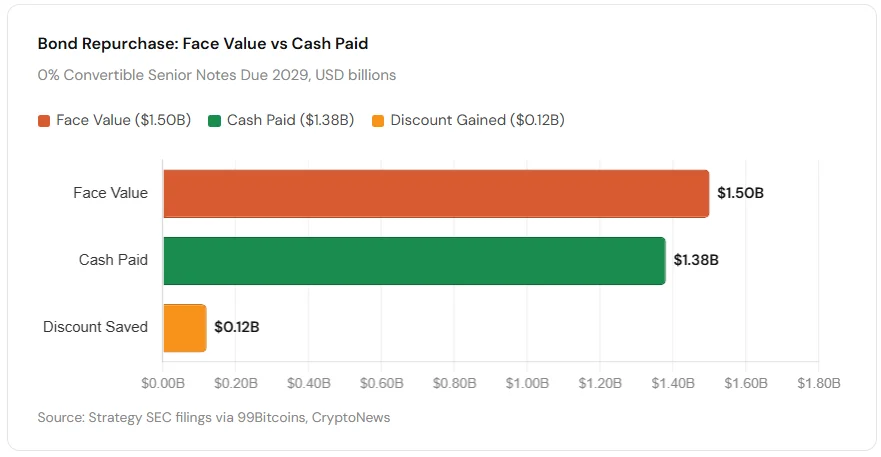

Strategy repurchased $1.5B in face value of convertible notes for $1.38B in cash, saving $120M.

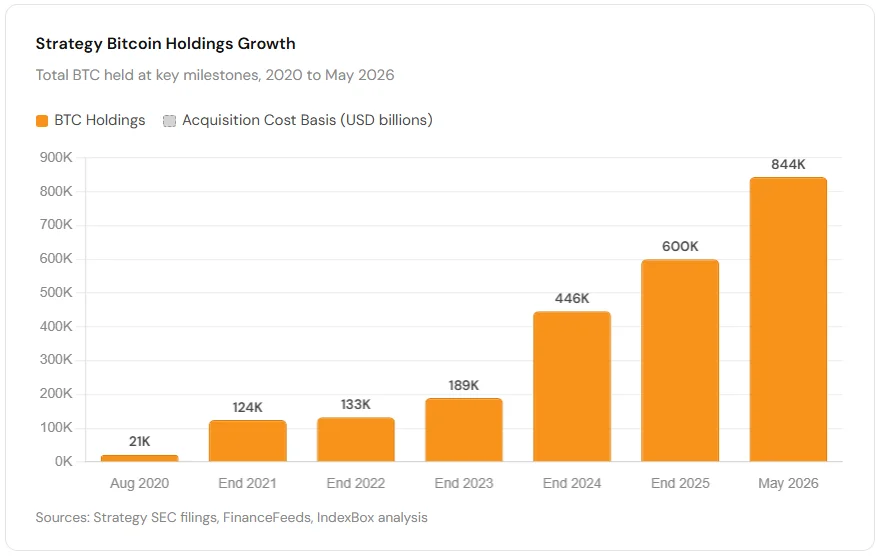

The firm holds 843,738 BTC worth $65.25B. No Bitcoin was sold to fund the bond buyback.

Michael Saylor confirmed the move on X. His message: “This week we bought bonds, not bitcoin.”

The pivot introduces a carry trade model using US Treasury instruments as a yield-generating leg.

A $3B liquidity window opens in June 2028, creating a key structural risk for existing holders.

Strategy made a decisive move this week. The company paused Bitcoin accumulation. Instead, it repurchased its own convertible bonds. This marks a clear strategic evolution for the firm, once known purely as a Bitcoin accumulator.

Chairman Michael Saylor confirmed the pivot on X. His post read: “This week we bought bonds, not bitcoin. The BitVac is charging.” That single message sparked widespread debate in the market.

The Bond Repurchase Explained

Company filings reviewed by FinanceFeeds show that Strategy agreed to repurchase approximately $1.5 billion in face value of its 0% coupon convertible senior notes. These notes mature in 2029. The company paid roughly $1.38 billion in cash for them.

The $120 million gap between face value and cash paid is significant. Retiring debt at a discount improves the balance sheet immediately. It also removes future dilution events. Fewer convertible notes means fewer potential conversions into MSTR shares.

Furthermore, existing stockholders benefit directly. Each note that disappears increases the Bitcoin-per-share metric for those already holding MSTR equity.

Analyst View

Crypto analysts widely frame this bond repurchase as bullish for MSTR equity. The move reduces dilution risk and strengthens the balance sheet ahead of any future Bitcoin acquisitions, according to FinanceFeeds reporting.

The Carry Trade Model

Strategy’s financial architecture has become more complex. The company raises capital through three channels: equity sales, convertible notes, and perpetual preferred shares. STRC is its primary preferred share instrument.

However, the model goes further than simple fundraising. A portion of raised capital now flows into short-duration US Treasury instruments. These generate yield while Strategy evaluates the conditions for Bitcoin accumulation.

This creates what analysts call a macro barbell. One side holds Bitcoin, a high-risk, high-reward asset. The other side holds Treasuries, a yield-generating safe leg. Together, they form a carry trade structure.

“Strategy borrows at ultra-low cost and earns spread against Treasury returns and Bitcoin appreciation.”

-CryptoNews Analysis, May 2026

The carry trade logic is straightforward. The 2029 notes carry a 0% coupon. STRC pays fixed dividends. Therefore, the cost of capital is minimal. Treasury yields then service those obligations and build reserves for future Bitcoin purchases.

Bitcoin Holdings Remain Intact

According to CryptoNews, Strategy currently holds 843,738 BTC. The portfolio is worth approximately $65.25 billion. The total acquisition cost stands at $63.88 billion. This leaves roughly $1.50 billion in unrealised profit.

Critically, no Bitcoin was sold to fund the bond repurchase. The BitVac metaphor holds: the machine is pausing to recharge, not to liquidate.

Additionally, FinanceFeeds notes that earlier this year, Strategy executed its largest single-week BTC purchase of 2026. The company acquired 22,337 BTC for $1.57 billion through preferred stock sales. This context underscores that the bond pivot is tactical, not permanent.

The 2028 Liquidity Risk

Not all signals are positive, however. A critical risk looms on the horizon. Strategy carries approximately $3 billion in convertible notes with attached put rights.

Noteholders can demand cash repayment starting June 2028, according to 99Bitcoins analysis. If capital markets tighten at that point, or MSTR trades below conversion prices, those obligations could force Bitcoin sales.

This is precisely why the front-loaded debt retirement makes strategic sense. Strategy now retires notes at a discount. It does so before the 2028 put window opens. This reduces the total size of that liquidity event.

Structural Risk

According to Decrypt, Strategy’s mNAV (market cap as a multiple of its Bitcoin NAV) dropped below 1x in early 2026. This occurred during a period when MSTR shares fell approximately 70% over six months. It demonstrates how quickly macro conditions can change this structure’s risk profile.

MSTR Is No Longer a Simple BTC Proxy

MSTR stock now demands a multi-dimensional analysis. It is no longer a pure Bitcoin proxy. Investors must consider three variables simultaneously.

First, there is Bitcoin price exposure. Second, there is rate sensitivity from the Treasury carry leg. Third, there is equity volatility from the convertible note structure. Each factor interacts with the others.

VanEck research approximately 9%. This is the lowest level since the company began its Bitcoin strategy in 2020. That suggests the balance sheet is healthier than it appears at first glance.

What Comes Next for Strategy?

The key question is timing. When will Strategy resume Bitcoin accumulation? The answer depends on several converging conditions.

Capital market conditions must remain open. Bitcoin’s price trajectory must support a favourable entry point. Moreover, liquidity risk in 2028 must remain manageable.

Saylor’s BitVac framing suggests confidence. The pause is temporary. The infrastructure is being strengthened. Furthermore, retiring discounted debt now frees borrowing capacity for future Bitcoin acquisitions.

Therefore, this week’s move is not a retreat from the Bitcoin thesis. It is a recalibration. Strategy is evolving from a one-directional accumulation machine into a sophisticated macro carry vehicle. The Bitcoin position remains at its core. However, the capital structure around it is growing more resilient.