July 12, 2026 – The prediction market has filed to register a futures broker arm. Leverage, however, still waits on two separate approvals.

In Summary

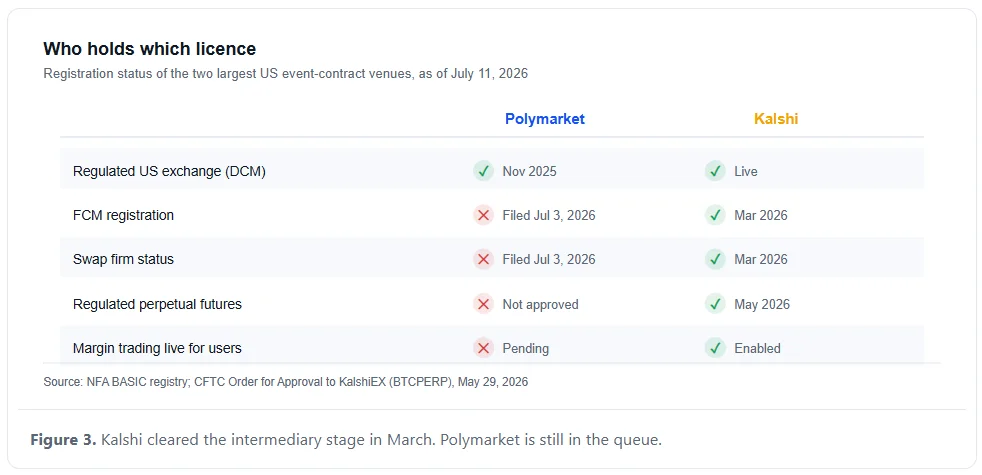

Polymarket filed on July 3 to register an affiliate as a futures commission merchant, an NFA member and a swap firm.

An FCM licence alone will not enable leverage. The CFTC must also clear a rulebook change that would allow part-funded positions.

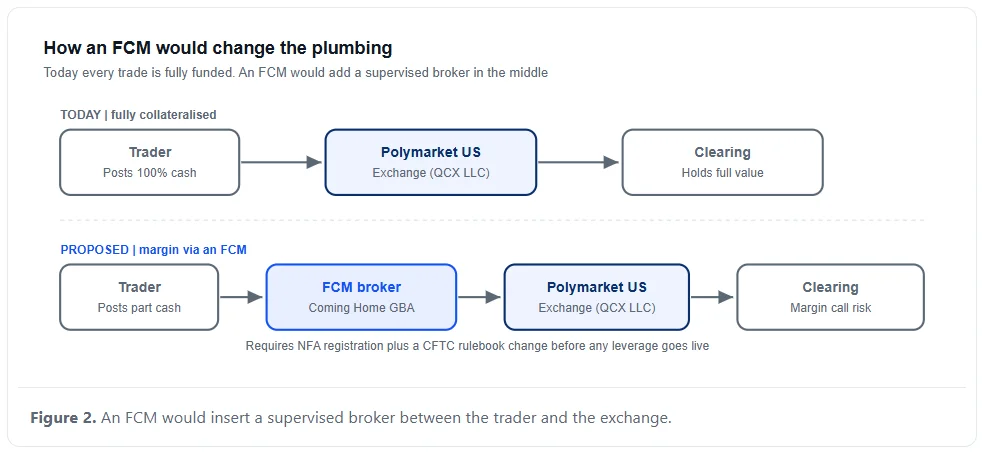

Every position on the US venue is fully collateralised today, which locks up capital that big trading desks want back.

Rival Kalshi cleared the same intermediary stage in March 2026, then won CFTC approval for a bitcoin perpetual in May.

State gambling litigation remains an open risk, so federal clearance would not by itself guarantee nationwide access.

Polymarket margin trading took a step closer this month. Yet the door is still shut. The prediction market filed on July 3 to sign up an arm as a futures broker.

So one day, US traders could put up part of a bet, not all of it. For now, though, the filing changes nothing. Two watchdogs still hold the keys.

The paper’s name is Coming Home GBA LLC. They also name PM Derivatives LLC. Moreover, the firm asked for three tags at once. It wants FCM status, swap firm status, and NFA membership.

Why the FCM tag matters

An FCM sits in a set spot in the futures chain. The NFA defines an FCM as an entity that takes orders to buy or sell futures, options, or swaps.

It also takes cash and assets from clients to back those orders. Furthermore, each FCM must join the NFA. It must also name a chief compliance officer.

In short, the tag turns a crypto venue into a regulated broker. Client cash must sit apart. Margin calls must go out. Reports must reach the CFTC.

Therefore, the FCM path buys trust. However, it costs speed.

Two locks, one door

Polymarket already runs a US exchange. It bought QCX LLC and its clearing arm to get there. The CFTC then signed an amended order in November 2025.

That order let the venue run with brokers in the middle. It also set full exchange rules. As a result, brokers can sign up clients and route flow through old-school rails.

The firm said the nod aligned with the trust the US market demands. Still, an exchange licence does not add leverage. Each bet must be paid in full.

To trade on margin, Polymarket needs two green lights. First, the NFA must clear the FCM bid.

Second, the CFTC must clear rule changes that allow part-paid bets. Until both locks turn, the margin stays a plan. It is not yet a product.

The 2022 shadow

Watchdogs recall the old model well. In January 2022, the CFTC fined the firm $1.4 million. At that time, the venue had no US licence at all.

Regulators also told it to wind down bets that broke US law. Staff have counted more than 900 event markets since 2020.

So each new filing now lands with a long paper trail. The firm rebuilt by buying licences, not by fighting.

Indeed, that choice is why this filing looks dull. Dull is the point.

The registry shows a bid. It does not show a licence.

Kalshi set the pace

Kalshi got there first. Its arm, Kinetic Markets, won FCM and swap firm status in March 2026.

That lead then paid off fast. In May 2026, the CFTC signed off on BTCPERP. It is a perpetual futures deal tied to spot bitcoin.

That order came under Section 5c(c)(4) of the law. Notably, it was the first true perp on a US venue with rules.

The CFTC also warned that the design may not suit every asset class. Other perps must now pass a case-by-case check.

Kalshi thus holds a four-month lead on broker plumbing. Polymarket, by contrast, waits in line.

Meanwhile, both chase the same prize. Big funds want margin, and margin needs an FCM.

What Polymarket margin trading would change

Full cash cover eats capital. A $10,000 bet ties up $10,000 today. Margin would cut that cash up front. Traders could then spread capital more widely.

Funds and market makers price that gap with care. Accordingly, margin is less a retail toy. It is an entry ticket for big money.

Event contracts are simple. They pay out based on a yes-or-no outcome. Big desks, however, rarely trade with full cash down. They hedge, they net, and they lean on credit.

Margin is thus the bridge between a betting app and a trading desk. Yet leverage cuts both ways. Losses grow as fast as gains.

Furthermore, an FCM must guard client cash and chase margin calls. Those jobs need staff, capital, and audited books.

NFA rules ask for certified accounts and a net capital review. So the wait is rarely short.

Risks that could stall the plan

Three snags stand out. First, the review has no fixed clock.

Second, state gambling suits still test how far US law reigns. Third, Kalshi keeps moving. It now wants perps on more assets.

Traders should read the filing as intent, not arrival. The registry shows a bid. It does not show a licence.

The bigger picture

Event markets keep drifting toward old-school market plumbing. Brokers, clearing, split accounts, and margin desks now populate the roadmap.

Big exchange groups have noticed. Their cash has followed. Intercontinental Exchange, which owns the NYSE, backed Polymarket with a $2 billion deal in 2025.

That kind of money does not chase grey markets. It chases licences. In the end, the sector swaps open rails for legal reach.

Polymarket margin trading is the sharpest sign of that swap yet. Whether the payoff beats the friction rests on one thing.

The CFTC must say yes. It has said no before.