July 18, 2026 – Morpho is preparing a controlled public launch for Midnight, its new fixed-rate lending protocol. The rollout could reshape onchain credit pricing.

In Summary

Midnight starts with one cbBTC/USDC market on Base and several maturity dates.

Direct lenders and borrowers gain access first, while automation tools arrive later.

Fixed maturities improve payment certainty, although liquidity and liquidation risks remain important.

Morpho Midnight launch narrows the scope

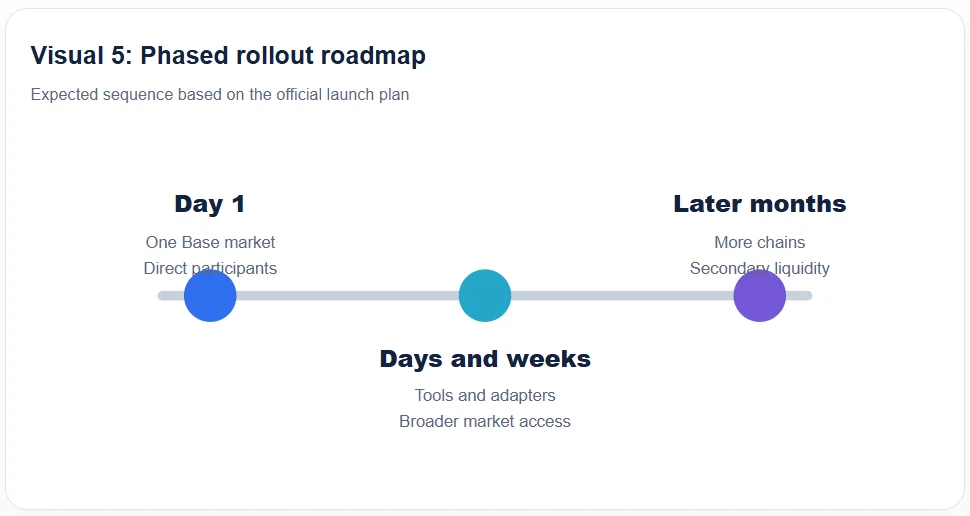

The Morpho Midnight launch follows several months of beta testing and security reviews. Morpho plans a deliberately limited first release.

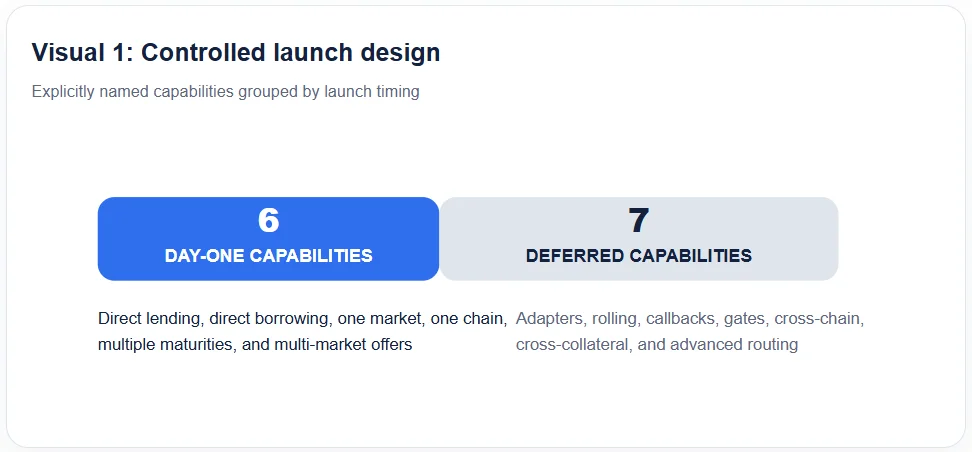

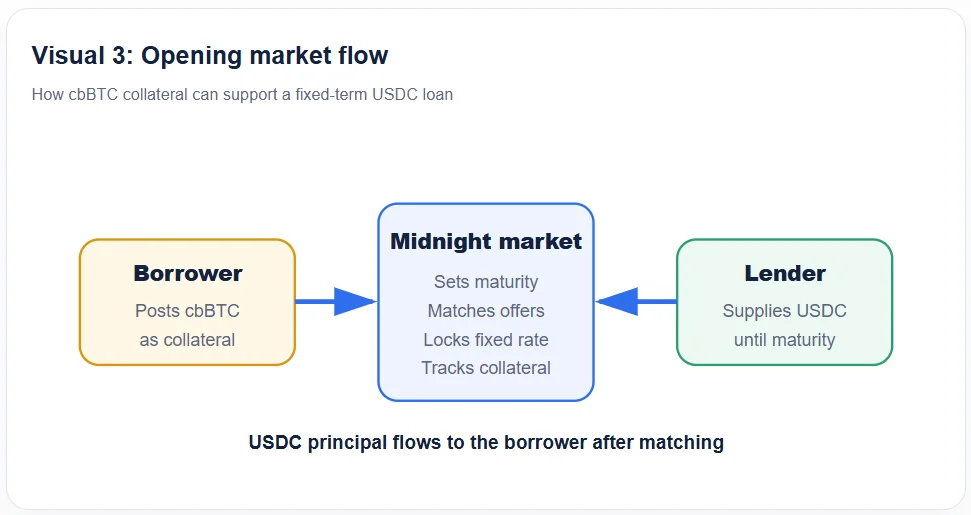

The protocol will initially support one market on one blockchain. Users can lend USDC or borrow it against cbBTC collateral.

Several maturity choices will create separate fixed-term markets. Therefore, users can select exposure that better matches their liquidity needs.

Multi-market offers will operate from the first day. This feature lets lenders quote across isolated markets without manually dividing capital.

However, the first release excludes vault adapters, auto-rolling, callbacks, gates, cross-chain functions, and cross-collateral markets. Morpho plans phased additions.

This narrow design reduces operational complexity. It also limits the liquidity channels available during the earliest trading period.

Fixed rates change the borrower equation

Midnight uses market units that settle at a price below their maturity value. That discount produces the implied fixed return.

Morpho’s documentation gives a clear example. A unit bought for 0.95 loan tokens returns one token at maturity.

The simple return equals 5.26% before fees and losses. Yet annualised returns vary sharply across different maturity periods.

A one-month maturity annualises that return to 63.16%. Six months produces 10.53%, while one year remains 5.26%.

Therefore, headline annualised rates may appear extreme for short maturities. Investors should compare actual cash returns and remaining duration.

Borrowers gain clearer funding costs. Lenders gain defined maturity dates, which can support treasury planning and duration management.

Why cbBTC and USDC matter

The opening market links tokenised Bitcoin collateral with a dollar-denominated loan asset. Coinbase states that cbBTC holds 1:1 Bitcoin backing.

That structure gives Bitcoin owners access to dollar liquidity without selling their underlying exposure. Still, wrapped assets introduce dependence on custodians.

USDC provides a large settlement base. Circle reported $77.0 billion in circulation at the end of the first quarter.

The company also recorded $21.5 trillion in quarterly onchain transaction volume. That figure increased 263% from the prior-year period.

Consequently, Midnight begins with two assets already used across major decentralised finance markets. This choice may help early price discovery.

Scale supports the experiment

Morpho’s dashboard reported $11.13 billion in deposits on July 17, 2026. Active loans reached $3.98 billion.

Total value locked stood at $7.15 billion, while total supply reached $4.58 billion. Those figures show an established lending network.

However, the existing scale does not guarantee deep fixed-rate liquidity. Separate maturities can fragment demand across several order books.

Multi-market offers may reduce that problem. Yet market makers still need reliable pricing, hedging tools, and sufficient borrower demand.

Risks remain visible

Fixed rates remove rate uncertainty, but they do not remove credit risk. Collateral values can fall before liquidators close positions.

Oracle failures may also trigger harmful liquidations or bad debt. Moreover, early users face smart contract and liquidity risks.

The delayed vault adapter may keep initial liquidity modest. Conversely, the gradual rollout could reduce systemic stress during price discovery.

Market outlook

Midnight represents a shift from protocol-set rates toward market-set term pricing. That model resembles a digital yield curve for secured credit.

Success will depend on repeat borrowing, competitive spreads, and active secondary liquidity. The first cbBTC/USDC maturities will provide the earliest evidence.

A stable launch could expand fixed-rate DeFi beyond specialist traders. A weak launch may reveal how difficult onchain duration markets remain.