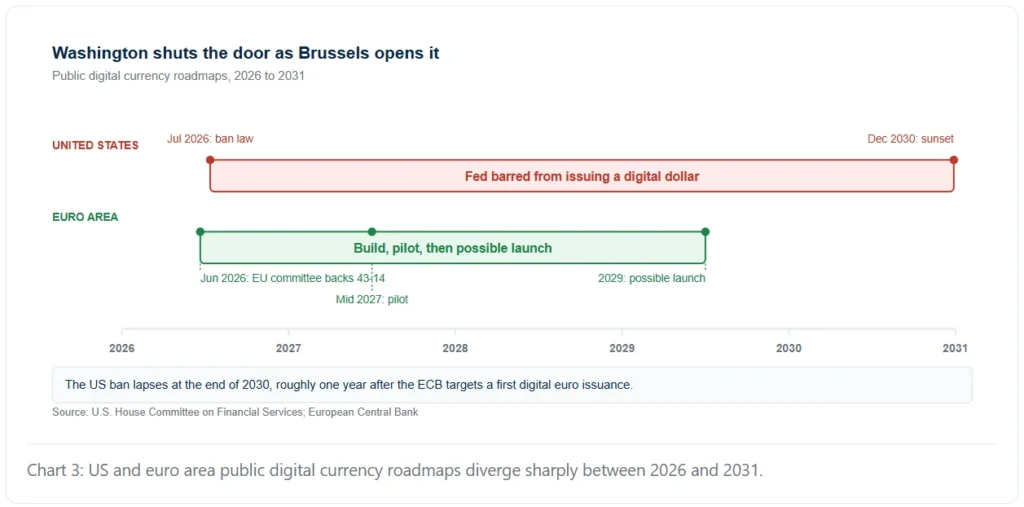

July 11, 2026 – A four-year block on a Federal Reserve digital dollar was enacted into law without a presidential signature, clearing the field for private stablecoin issuers until 2031.

In Summary

A four year block on a Federal Reserve digital dollar became law on Saturday without any presidential signature.

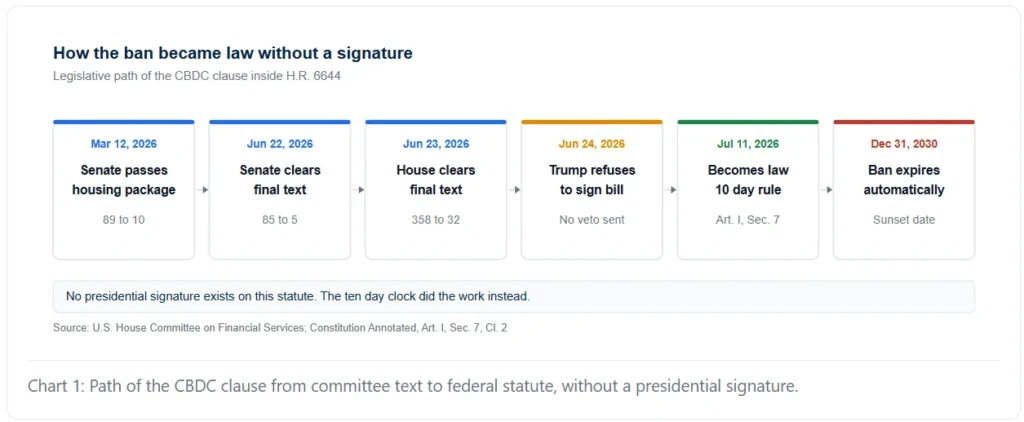

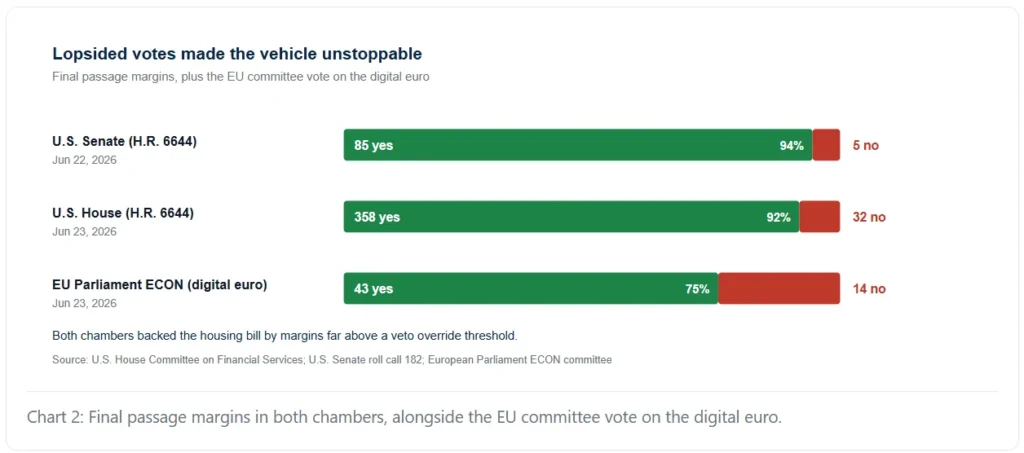

The clause rode inside the 21st Century ROAD to Housing Act, which cleared the House 358 to 32 and the Senate 85 to 5.

Article I of the Constitution turns an unsigned bill into law after ten days while Congress sits.

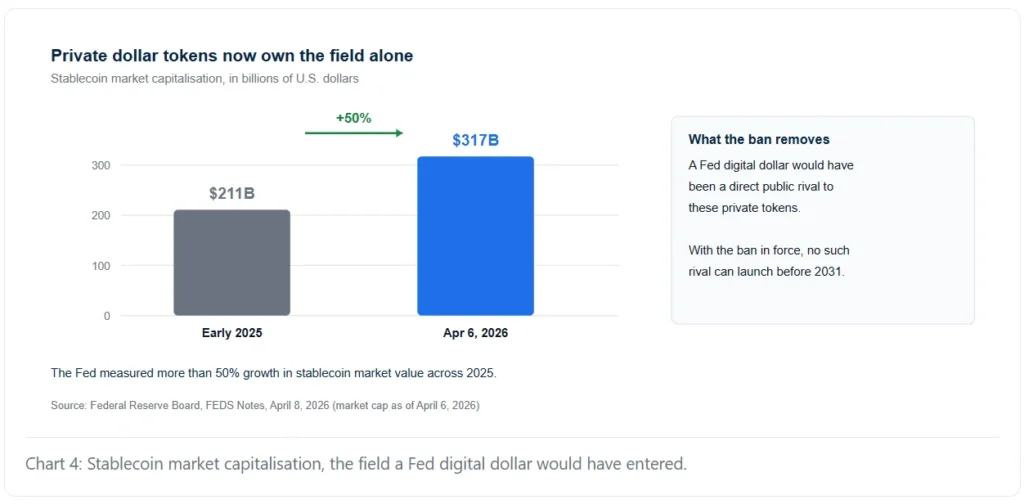

Private stablecoin issuers, a market the Fed valued at 317 billion dollars, now face no public rival before 2031.

Europe moved the other way in the same week, with EU lawmakers backing a digital euro aimed at a 2029 launch.

The US CBDC ban is now law, and no one signed it. President Donald Trump refused to sign the housing bill that carries it. Yet the clause took effect at the first moment of Saturday. Therefore, the Federal Reserve can no longer issue a digital dollar.

The ban runs through December 31, 2030. Moreover, it stops any Fed bank from making a similar asset. Lawmakers had buried the clause deep in a housing bill.

How the US CBDC ban cleared Congress

Republicans never had the votes for a stand-alone digital dollar ban. So they bolted the text onto a bill that had to pass. The 21st Century ROAD to Housing Act gave them that ride.

That bill held more than 45 clauses on housing supply and permits. Because of its reach, it drew broad support from both parties. The House cleared the final text by a vote of 358 to 32. Meanwhile, the Senate had backed the same text 85 to 5 a day earlier.

Few members treated the money clause as a sticking point. Indeed, most of them came to vote on homes, not on tokens. That is exactly why the tactic worked.

The quirk that sealed the outcome

Trump then staged a late protest. He asked the Senate to pass a separate elections bill first. Yet he never sent back a formal veto.

That gap proved fatal. Article I gives the president ten days to return a bill he dislikes. If he neither signs nor sends it back, the bill becomes law anyway. So his protest shifted the mood but not the law.

Traders should note the rule with care. A pocket veto works only when Congress goes home. Since both chambers still sit, the clock simply ran out.

Why stablecoin issuers gain the most

The Fed was never building a digital dollar. Past chairs said the job would need clear consent from Congress. Still, the ban hands private issuers real value.

Context explains the prize. Washington had already blessed private dollar tokens in 2025. A federal stablecoin law set reserve and licence rules that year. Now the state has ruled out its own rival product. As a result, the policy stack points in only one direction.

It strips a rival, even a theoretical one, out of the dollar payments race. Private tokens now hold that ground alone. Fed staff estimated the stablecoin market at $ 317 billion in April 2026. Furthermore, they logged nearly 50% growth throughout 2025.

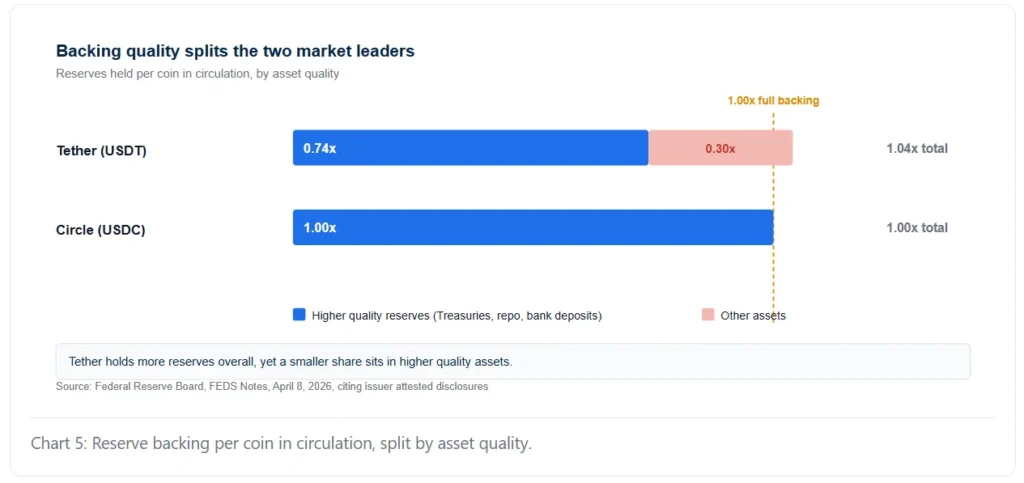

Backing quality sharply divides the two leaders. Tether reports about 1.04 times the reserves for each coin it issues. However, only 0.74 times counts as a higher quality cover. Circle, by contrast, backs USDC in full with higher-quality assets.

That gap matters more now. Because no public option exists, users must judge issuer risk on their own. Fed staff warn that the risk still sits in the system.

Europe drives the other way

The split with Europe could hardly look sharper. EU lawmakers backed the digital euro text by 43 votes to 14. That vote landed within hours of the Senate ban.

The European Central Bank plans a pilot from mid 2027. In addition, it aims to launch in 2029. Build costs run near 1.3 billion euros. Yearly running costs would add some 320 million euros.

Europe casts the plan as control of its own money. Foreign card firms process most euro-area card payments. Therefore, Brussels sees reliance where Washington sees reach. Both sides claim privacy, yet they land in opposite camps.

What the ban actually covers

Read the limits with care. First, the clause binds the Fed and nothing else. Second, it leaves private stablecoins free under current law. Third, it lapses on its own at the end of 2030.

Nothing here curbs banks or tokenised deposits. Similarly, it does not touch the FedNow instant payments rail. Wholesale research also runs on without a block.

A future Congress could stretch the window. Instead, lawmakers could simply let it die. Either route needs a new bill and new votes.

The precedent is worth watching

The wider signal is about process, not money. Trump has shown he will hold a passed bill hostage to other demands. Consequently, the pending Digital Asset Market Clarity Act now faces the same risk.

That bill would split crypto oversight between two agencies. Industry groups have chased it for years. However, a win in Congress no longer means a signing ceremony.

Markets barely moved on the news. Bitcoin traded near 64,000 dollars this week. Most desks had priced the ban in weeks ago. Traders knew the votes back in June.

The real effect lands on planning. Payment firms that build dollar rails face no public rival before 2031. For long vendor bets, that clarity carries weight.

Still, the sunset date earns a diary note. Four years pass fast in payments. Meanwhile, Europe may well have a live digital euro by then.