June 25, 2026 – Crypto-backed lending has rebuilt itself since the 2022 collapse. Here is how to evaluate a lender before you pledge your Bitcoin.

In Summary

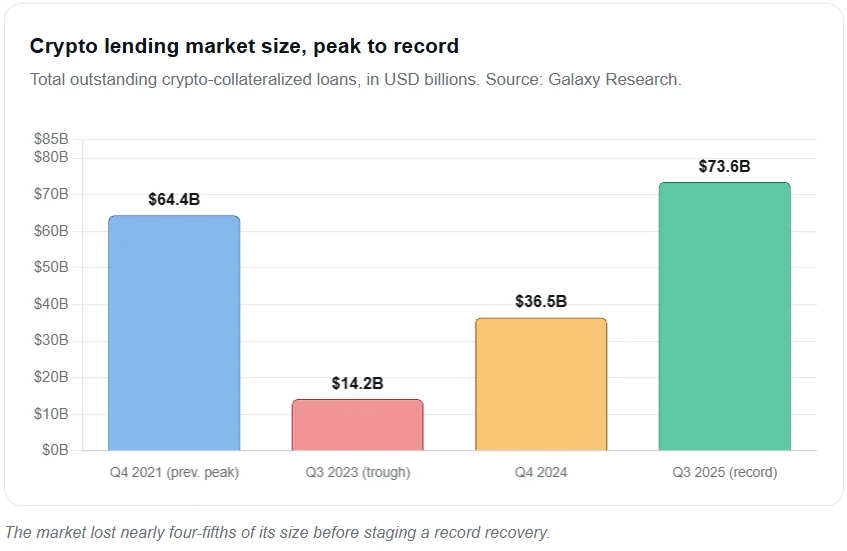

Crypto-backed lending has fully rebuilt since the 2022 collapse, reaching a record $73.59 billion at the end of Q3 2025.

The market then cooled about 10% in Q4 2025, as falling DeFi asset prices pulled down totals.

The recovery was steep, climbing from a $14.2 billion trough in 2023 after a roughly 78% crash.

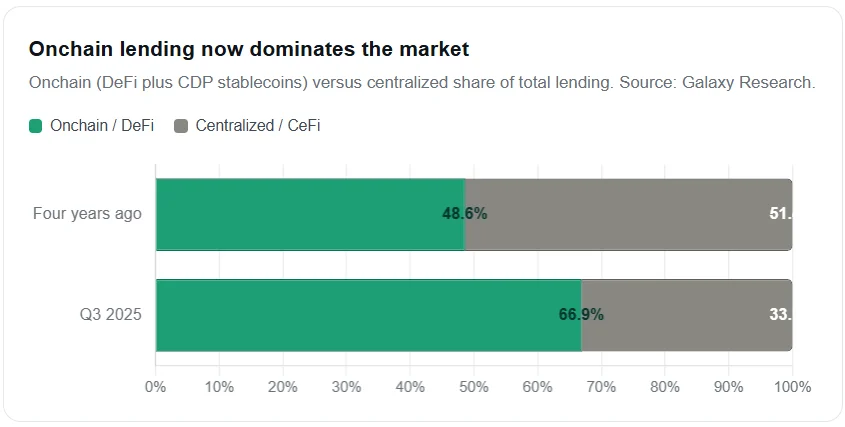

Power has shifted on-chain, with DeFi now holding about two-thirds of all crypto lending.

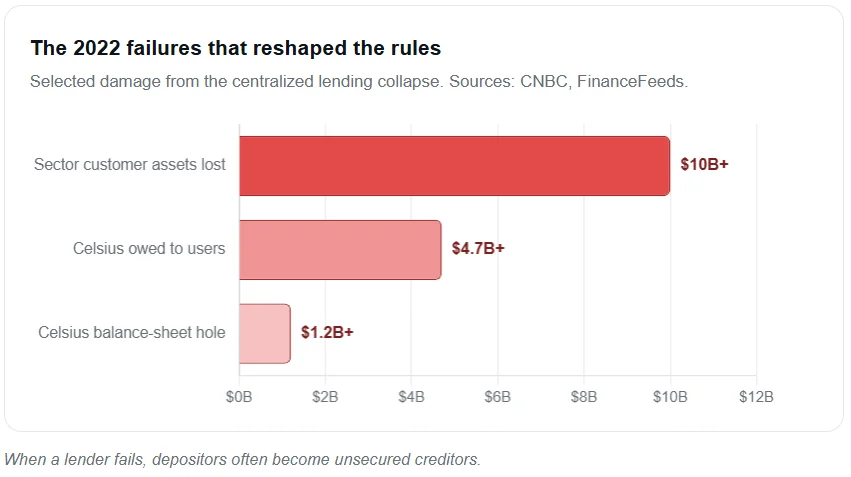

The 2022 failures wiped out more than $10 billion in customer assets across Celsius, BlockFi, Genesis, and Voyager.

Those collapses rewrote the rules around custody, licensing, and collateral protection.

For borrowers, a headline rate reveals little. The all-in APR, custody, cure window, and licensing matter more.

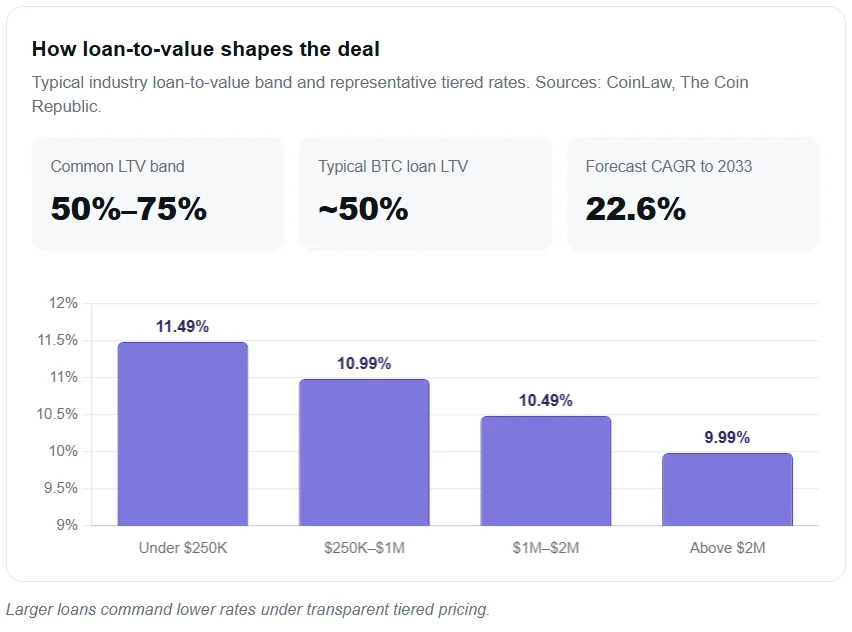

Loan-to-value ratios still cluster between 50% and 75%, with Bitcoin loans commonly near 50%.

The market is projected to grow at a 22.6% annual rate through 2033.

The crypto-backed loan market in 2026 looks nothing like the one that froze in 2022. Borrowers now pledge Bitcoin, Ethereum, or Solana for cash. Moreover, they keep their position and often defer a taxable sale.

The category has matured fast. However, that maturity hides a new trap. Offers now look alike, yet a headline rate reveals very little. Therefore, smart borrowers ask sharper questions first.

A market rebuilt from the rubble

The numbers tell a striking recovery story. Crypto-collateralized lending reached a record $73.59 billion at the end of Q3 2025, according to Galaxy Research. That figure topped the previous peak of $69.37 billion from late 2021.

The journey there was brutal. The market had peaked near $64.4 billion in Q4 2021. Then it crashed roughly 78% to a $14.2 billion trough by Q3 2023. Afterward, it clawed back to $36.5 billion and then surged again.

The rebound was not perfectly smooth, though. Galaxy later reported a roughly 10% quarter-on-quarter decline in Q4 2025. Falling DeFi asset prices drove most of that dip. Still, centralized lending continued to grow throughout the period.

Why on-chain lending pulled ahead

The recovery changed who controls the market. On-chain venues now hold about 66.9% of total lending. By contrast, that share sat near 48.6% four years earlier, Galaxy data shows.

This shift matters for borrowers. DeFi protocols survived the last cycle because their loans stayed overcollateralized and transparent. Meanwhile, many centralized lenders collapsed under opaque, undercollateralized bets.

The 2022 lesson borrowers cannot ignore

The 2022 failures were structural, not technological. Unlicensed lending, commingled assets, and hidden leverage did the damage. Consequently, regulators and borrowers now demand cleaner structures.

The cost was enormous. The sector lost more than $10 billion in customer assets as Celsius, BlockFi, Genesis, and Voyager froze withdrawals, FinanceFeeds reported. Celsius alone owed users about $4.7 billion and hid a $1.2 billion balance-sheet hole, CNBC found.

Depositors learned a painful truth. When a lender fails, customers often become unsecured creditors. As a result, they wait in line behind other claimants for whatever remains.

A headline rate tells you almost nothing about the loan you are actually signing.

A framework for evaluating any 2026 loan

The rate is where most comparisons begin and end too early. DeFi protocols advertise variable rates that float with pool demand. By contrast, centralized lenders quote fixed rates, usually from high single digits to the mid-teens.

The real cost hides inside the all-in figure. Origination fees, protection add-ons, and the loan-to-value tier all move the true number. Therefore, borrowers should ask for the APR, not the rate.

Custody decides your worst-case outcome

Custody answers one question. What happens to your collateral if the lender fails? There are three broad models, and each carries a different risk.

Centralized custody puts your crypto on the lender’s balance sheet. You hold a claim, not the asset. Non-custodial protocols lock collateral in a smart contract instead. Nobody can spend it, yet nobody answers for it either.

Hybrid models split the difference. A licensed lender services the loan while collateral sits in a segregated, on-chain wallet. Consequently, borrowers can verify the location of their assets directly on the blockchain.

Liquidation, licensing, and rehypothecation

Every crypto loan can liquidate collateral if the value drops. However, the cure window differs sharply. DeFi protocols sell instantly when a line is crossed. Centralized lenders usually issue a margin call and a grace period.

Licensing matters just as much. In the US, a crypto loan remains a loan. So it should sit inside a named entity with state licenses you can verify.

Finally, ask the question that few borrowers raise. Can the lender lend out your collateral? This practice, called rehypothecation, quietly preceded several past failures. The protection is segregation, backed by explicit no-reuse language in the agreement.

What the numbers mean for you

Loan terms still follow predictable patterns. Industry loan-to-value ratios typically range between 50% and 75%, CoinLaw data shows. Bitcoin loans commonly sit near 50%, which buffers against sharp price swings.

Scale also rewards larger borrowers. Established lenders publish tiered rates that fall as loan size rises. Ledn, for example, originated $1.4 billion in loans during 2025 and claims about 30% of the bitcoin-backed market.

The trajectory points up despite the recent wobble. Analysts project the crypto-backed lending market to grow at a 22.6% compound annual rate through 2033. Borrowers should still treat platform choice as a risk decision before a rate decision.

The bottom line

Ask the hard questions before you need the answers. Probe the rate, the custody, the licensing, and the cure window. Above all, confirm your collateral stays segregated and yours. The market spent three years rebuilding that discipline, so borrowers should match it.