You don’t need to build an exchange. CaaS lets traditional companies plug into the crypto infrastructure while maintaining full control over their brand and compliance.

In Summary

Crypto-as-a-Service (CaaS) is a plug-and-play model. Banks and fintechs add crypto features without running an exchange.

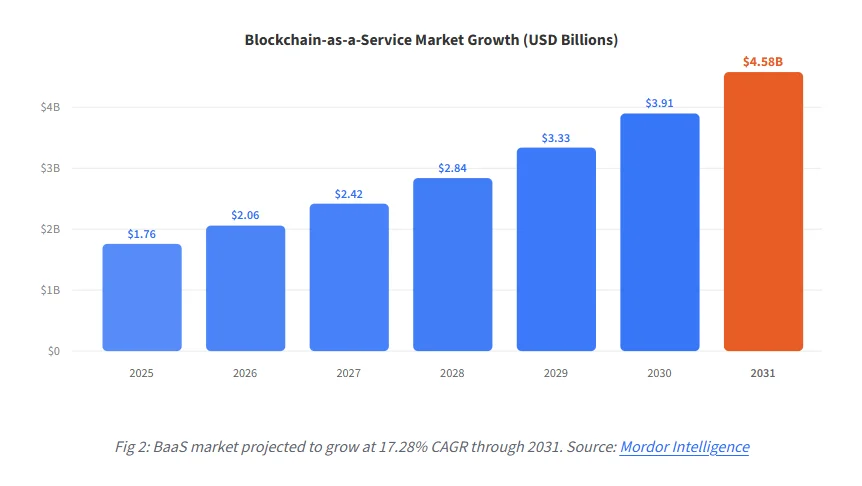

The blockchain-as-a-service market is projected to reach $4.58 billion by 2031, growing at 17.28% CAGR.

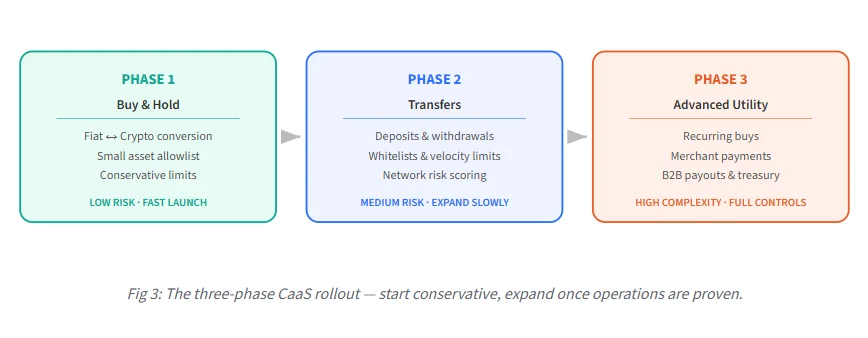

A phased rollout buy/hold first, then transfers, then advanced products, reduces operational risk.

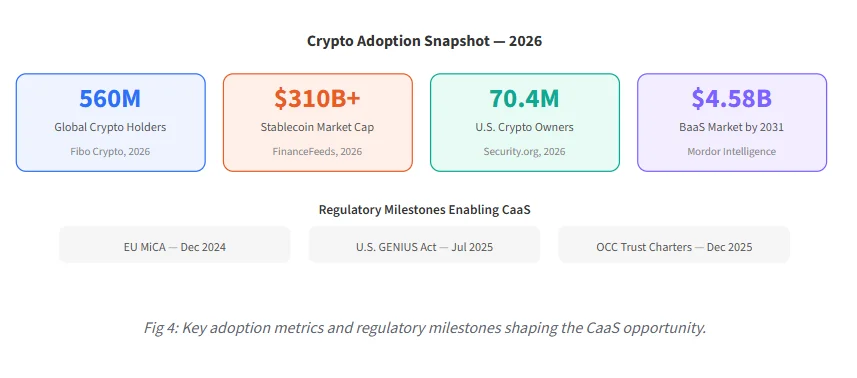

Regulation is enabling adoption. The EU’s MiCA framework and the U.S. GENIUS Act now provide clear guardrails.

Security, custody design, and compliance workflows are the make-or-break factors, not the technology itself.

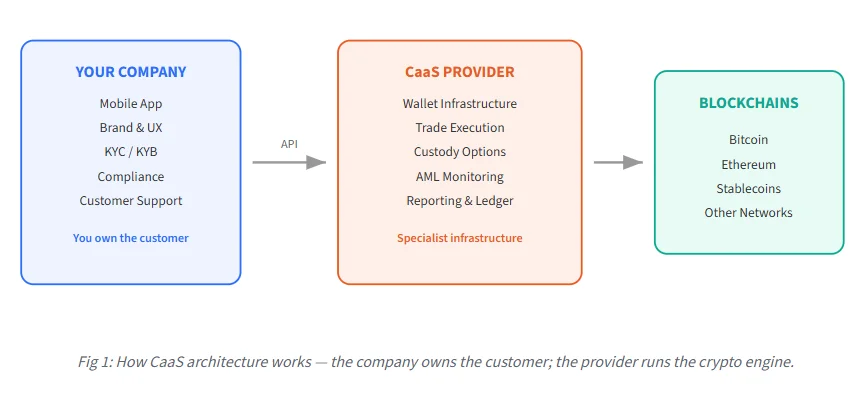

What Is Crypto-as-a-Service?

Think of CaaS like a white-label engine. A bank or fintech plugs into a specialist provider’s infrastructure. That provider handles wallets, trading execution, custody, and compliance tooling behind the scenes. The bank keeps its brand, customer relationships, and regulatory accountability.

In simpler terms: your bank app looks and feels the same. But now it can let you buy Bitcoin, hold Ethereum, or send stablecoins. The bank didn’t build a crypto exchange. It partnered with one.

This matters because building from scratch is expensive and slow. CryptoSlate institutional guide notes that most regulated firms fail not on “can we build it?” but on operational risk, custody controls, fraud handling, and post-launch reporting.

Why Now? The Market Opportunity

Institutional crypto adoption has accelerated sharply. Approximately 560 million people worldwide now hold crypto. In the U.S. alone, around 70.4 million adults own cryptocurrency as of 2026. These customers already bank with traditional institutions; they just go elsewhere for crypto.

The regulatory picture has also cleared up. The EU’s MiCA regulation took effect in late 2024, creating the first comprehensive rulebook for crypto service providers across 27 member states. In the U.S., the GENIUS Act was passed in July 2025, establishing federal standards for stablecoins. Meanwhile, the OCC conditionally approved five national trust bank charters for digital-asset firms in December 2025.

Major banks are already moving. JPMorgan is preparing crypto-collateralized loans, PNC partnered with Coinbase for trading access, and Goldman Sachs launched Ethereum-based tokenized money-market funds. CaaS gives smaller institutions a way to compete without building all of this themselves.

The Three-Phase Launch Playbook

Successful institutions don’t launch everything at once. They use a phased approach. Each phase adds complexity only after controls prove stable.

Phase 1: Buy and Hold. Start simple. Let users convert fiat to crypto and hold it. Use a small list of approved assets with conservative limits. This phase tests your onboarding flow, disclosures, reconciliation, and support readiness.

Phase 2: Deposits and Withdrawals. Add deposit addresses and withdrawal capability on approved networks. This is where operational complexity jumps. Chain fees, address errors, and fraud attempts all surface here. Expand networks slowly.

Phase 3: Advanced Utility. Recurring buys, merchant payments, B2B payouts, and treasury workflows come last. These features are valuable. But they also multiply compliance and operational demands.

Security and Compliance: The Real Make-or-Break

Technology is not the bottleneck. Operations are. The crypto security market is valued at roughly $4 billion in 2026 and is growing at 21.7% annually. Why? Because $3.4 billion was stolen through hacks in 2025 alone, with the Bybit breach accounting for $1.5 billion of that.

For any institution using CaaS, the non-negotiable controls include withdrawal whitelisting, multi-approver transactions, role-based access, incident-response playbooks, and audit-grade logging. CaaS does not outsource accountability. Your firm still owns customer outcomes, complaint handling, and relationships with regulators.

On the compliance side, this means KYC/KYB alignment, sanctions screening, transaction monitoring, and audit-ready recordkeeping from day one. As B2Broker’s institutional analysis notes, brokers and fintechs are now expected to deliver institutional-grade execution, reporting, and compliance, not just trading access.

Build vs. Buy vs. Partner: Choosing Your Path

Institutions typically weigh three options. Building in-house gives full control but requires deep crypto engineering, 24/7 operations, and much longer timelines. Buying point solutions (separate custody vendor, separate analytics tool, separate payment rail) offers flexibility but creates integration headaches and unclear incident ownership.

Partnering via CaaS offers the fastest route. You get a tested stack, shared processes, and shorter time-to-market. The tradeoff? You must negotiate strong service-level agreements, confirm jurisdictional permissions, and plan an exit strategy in advance.

For most mid-sized banks, neobanks, and fintech platforms, CaaS is the pragmatic middle ground. As CB Insights research shows, crypto-native firms like Circle, Ripple, and BitGo are receiving U.S. bank charters and competing for full-stack banking relationships, making CaaS partnerships increasingly strategic.

Analytical Insight: Who Benefits Most?

CaaS is not equally valuable for every organization. The model delivers the most benefit to mid-tier banks seeking crypto revenue without heavy R&D spend; neobanks and super-apps that want to bundle crypto alongside traditional banking features; telcos with large user bases in markets where mobile money and crypto overlap; and payment service providers expanding into merchant crypto acceptance.

The global cryptocurrency market reached $3.35 billion in 2026, growing at 17% annually. Stablecoin supply now exceeds $310 billion, a signal that crypto is being used for actual transactions, not just speculation. For institutions, this shift from speculation to utility is exactly what makes CaaS viable in the long term.

The Bottom Line

Crypto-as-a-Service removes the heaviest barriers to entry. You don’t need to understand blockchain at the protocol level. You don’t need to hire a team of 50 crypto engineers. What you do need is a clear product vision, strong compliance workflows, and the right partner.

The firms that launched phase by phase, with controls tested at each step, are the ones reporting sustainable crypto revenue today. With over 70% of global jurisdictions now providing some form of stablecoin or crypto regulatory clarity, the window to move from planning to launch has never been wider.

CaaS won’t make crypto risk-free. But it makes crypto achievable, even for institutions that wouldn’t dream of building an exchange.