June 16, 2026 – The Fundstrat founder reframes ETH as infrastructure rather than a trade. His firm, BitMine, now holds 5.54 million ETH and stakes most of it.

In Summary

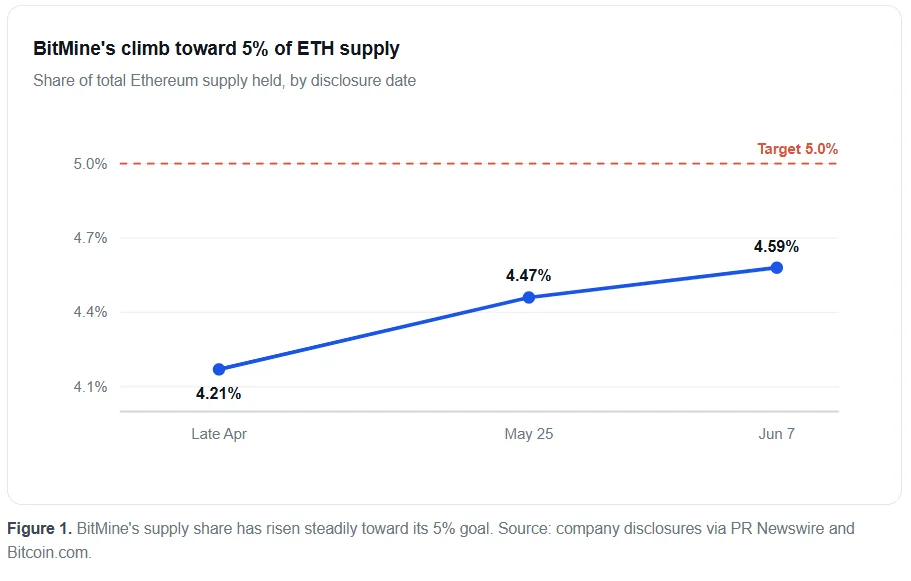

BitMine holds 5,543,872 ETH, roughly 4.59% of Ethereum’s total supply.

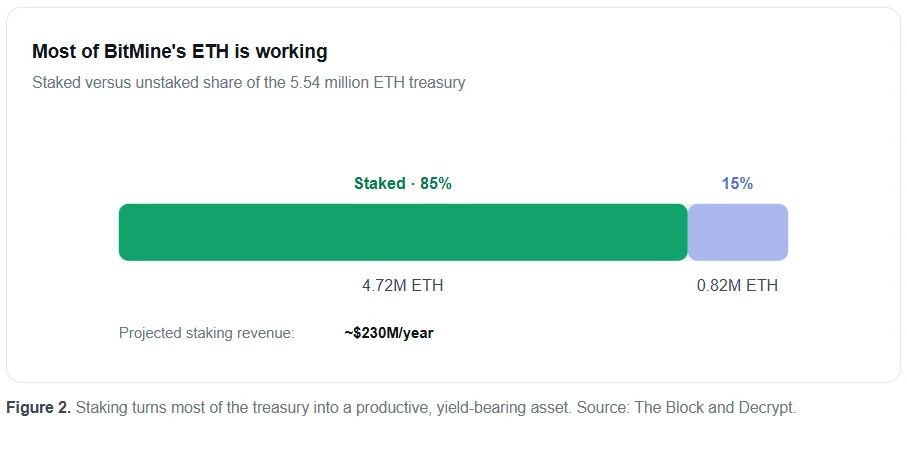

About 4.72 million ETH is staked, or close to 85% of the treasury.

Staking points to roughly $230 million in projected annual revenue.

Total crypto, cash, and equity holdings reached $9.6 billion on June 7, 2026.

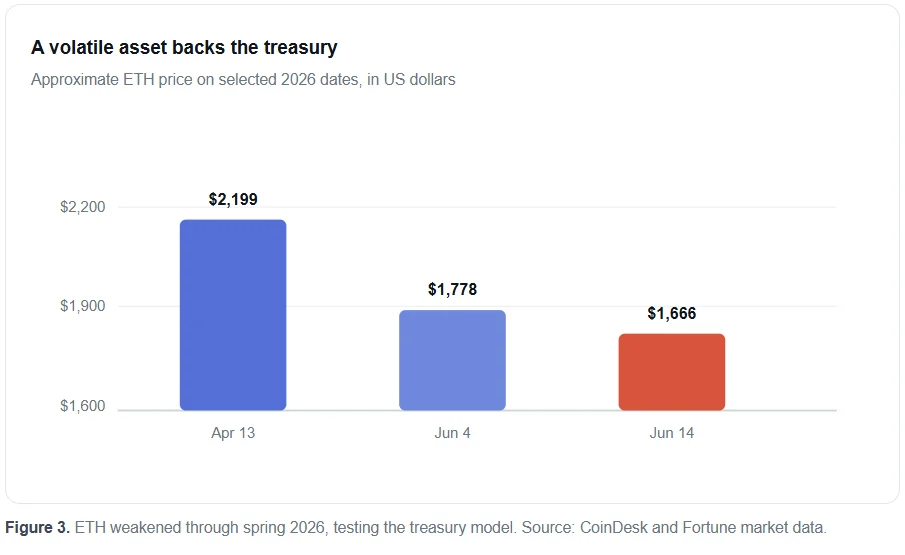

The strategy ties BitMine’s value tightly to a volatile ETH price.

Tom Lee has placed Ethereum back at the center of the institutional crypto debate. His latest framing is simple. Investing in blockchain, he argues, resembles holding prime real estate.

The logic follows a clear chain. Real estate gains value when people, businesses, and capital flow through it. Likewise, a blockchain may gain value when stablecoins, tokenized assets, and smart contracts depend on it. Lee first applied this analogy to Bitcoin. He told Bitwise it is better to own the land under a franchise. Now he extends the same thesis to Ethereum.

This view explains the aggressive strategy at BitMine Immersion Technologies. Lee chairs the company, and it treats ETH as long-term digital infrastructure. Therefore, BitMine keeps accumulating, staking, and building validator systems rather than trading short-term.

BitMine’s 5% supply target explained

BitMine’s plan centers on one goal. The firm wants to hold about 5% of all Ethereum. It calls this target the “Alchemy of 5%”. Its current position sits very close to that line.

According to the Company’s June 8 disclosure, BitMine holds 5,543,872 ETH worth billions of dollars. That equals 4.59% of the 120.7 million ETH supply. As a result, the firm ranks as the world’s largest Ethereum treasury.

The position carries real weight for investors. It gives public-market buyers indirect ETH exposure through a listed stock. Moreover, it lets BitMine earn staking rewards on a very large balance. Consequently, the firm has built a clear identity as an Ethereum-focused treasury.

Why Lee calls blockchain digital real estate

Lee’s comparison helps investors view Ethereum through a long-term lens. Instead of a volatile token, he frames it as a network where financial activity can compound. Several forces support that case.

Networks behave like infrastructure

Real estate gains value from location and demand. Ethereum, by contrast, gains value from network activity. It supports smart contracts, stablecoins, and around-the-clock global settlement. Therefore, more usage can lift the network’s strategic value.

Stablecoins and tokenization add real demand

Stablecoins remain one of crypto’s clearest real-world uses. Traders, lenders, and payment firms move digital dollars across Ethereum every day. Furthermore, tokenization could bring stocks, bonds, and funds on-chain. Each new asset class adds settlement demand to the network.

AI could open a new demand layer

Lee also links demand for blockchain to artificial intelligence. Future AI agents may need to pay, verify ownership, and settle deals automatically. Public blockchains suit that task because they stay programmable and always available. Still, this remains a long-term thesis rather than a sure outcome.

Inside the treasury: ETH, staking, and yield

BitMine does more than hold Ethereum. It actively stakes most of its balance to earn protocol rewards. This is where Lee’s rental-income comparison gains force.

The company has staked 4,718,677 ETH, about 85% of its holdings. That staked pile points to roughly $230 million in projected annual revenue. At full deployment, BitMine estimates the figure could climb toward $270 million.

This yield marks the key split from Bitcoin treasuries. Bitcoin usually sits idle as a reserve asset. Ethereum, however, can pay protocol rewards through proof-of-stake. So BitMine gains access to two potential sources of income: price appreciation and staking income.

BitMine routes much of this through MAVAN, its Made in America Validator Network. The platform began as in-house infrastructure for the firm’s own treasury. The company is now opening it to institutions, custodians, and partners. In effect, BitMine wants to own and operate the digital infrastructure, not just rent space on it.

The risk behind the conviction

The upside is clear, yet the risks are equally sharp. BitMine’s value tracks Ethereum’s price very closely. When ETH falls, the Company’s balance sheet and stock feel immediate pressure.

That pressure is not hypothetical. ETH traded near far higher levels earlier in the year before sliding through 2026. The token changed hands at around $1,666 on June 14, down sharply over the past 12 months. BitMine’s stock fell roughly 31% in the month to June 7.

Several other risks deserve attention. Financing needs may force the company to lean on capital markets. New equity could dilute existing shareholders. Meanwhile, staking adds technical, custody, and slashing risks. Regulatory scrutiny of crypto treasuries may also grow over time.

What it means for investors

BitMine offers a clean read on a bigger shift. Public companies increasingly treat ETH as a strategic, productive asset. The firm combines accumulation, staking yield, and validator infrastructure into a single bet.

The thesis rests on adoption. If stablecoins, tokenization, and on-chain settlement continue to grow, the strategy could pay off. If adoption stalls or ETH keeps sliding, the same concentration becomes a liability. For now, BitMine stands as the clearest public proxy for Lee’s digital real estate idea. Readers should treat it as analysis, not investment advice, and weigh the volatility carefully.