June 21, 2026 – STRC and SATA slid under their $100 anchor this week. The drop exposed hidden leverage inside a $10 billion market for Bitcoin-linked income.

In Summary

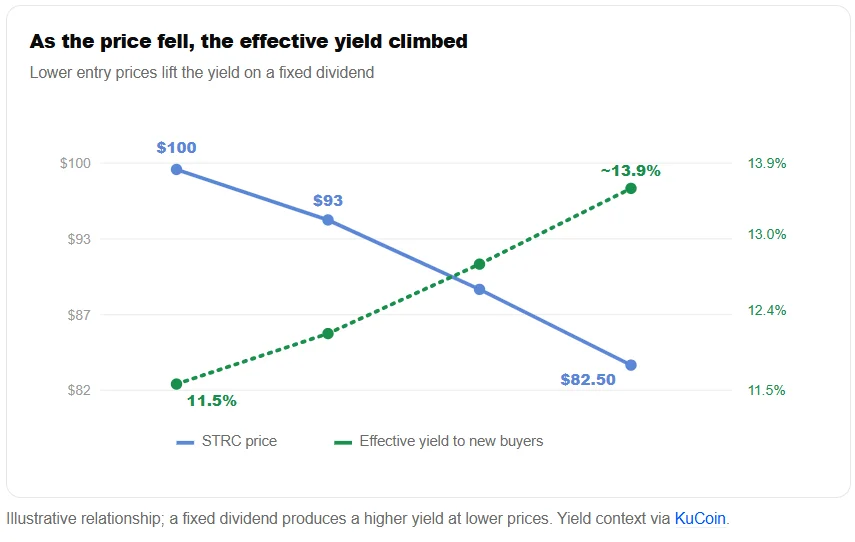

Strategy’s STRC fell to a record low near $82.50 before it rebounded, roughly 15% below its $100 par value.

Strive’s SATA also broke below par, showing how stress spreads across a young and crowded Bitcoin yield market.

Issuers say reserves stayed intact, yet brokers may now tighten margin rules, so the next version of this trade will cost more.

Bitcoin’s newest income trade lost its calm this week. Two preferred shares built around Bitcoin treasury companies slipped below their $100 anchor. The move surprised investors who had treated them as steady payers.

Strategy’s STRC dropped as low as $82.50 on June 18. It then recovered sharply within the same session. Strive’s SATA fell from near par to the low $90s before bouncing back.

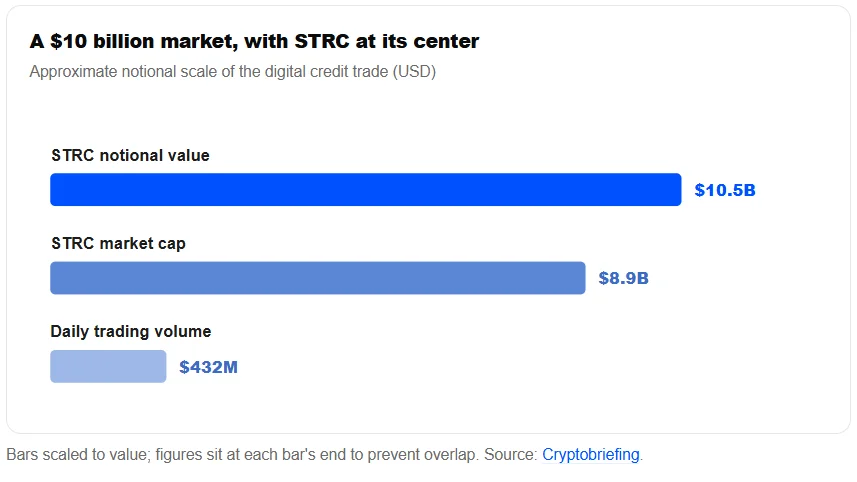

The break jolted a market that grew to roughly $10 billion in under a year. Moreover, it gave investors their first clear look at how these products behave under pressure. A quiet trade met margin calls, and the calm cracked.

A quiet income trade draws borrowed money

STRC and SATA sit in a new corner of the Bitcoin treasury market. Both are perpetual preferred shares. Therefore, they pay recurring dividends but carry no fixed maturity date.

Strategy helped create the category with STRC. Strive followed with SATA. Each issuer used the structure to reach investors who wanted yield from a Bitcoin-heavy balance sheet, rather than direct coin exposure.

The products found demand because Bitcoin itself pays no income. A share yielding roughly 11% to 13% appeals to income buyers. Strategy held STRC’s rate at 11.5% for several months to balance payout cost against cash strain.

The trade grew more attractive while STRC hugged $100. A security that rarely strays from par, yet pays a double-digit dividend, invites investors to treat it as stable. Consequently, some buyers reached for leverage.

They borrowed against the shares to lift exposure and returns. The dividend stayed the same. However, leverage let them hold more shares with less upfront cash. That trade needed one condition. The price had to stay near par.

Liquidations cluster near the lows

Once STRC began to slip, leveraged holders lost their cushion. The price fell, margin pressure increased, and borrowed accounts were forced to sell. As a result, selling fed on itself.

Analysts noted that many buyers had entered near $100. If they used similar margin terms, their risk levels sat near similar prices. Therefore, one shared trigger could unwind many positions at once.

The timing of the volume reinforced that view. Heavy midday trading looked more like broker-driven liquidation than ordinary repositioning. Equity markets usually see peak volume near the open and close, not the middle.

Short sellers may have pressed the move further. A crowded long trade financed with debt makes an obvious target. Bearish traders can push prices down, trigger forced sales, then buy back into the panic.

SATA’s decline followed the same logic. Investors facing margin calls often sell what they can, not only the problem position. Thus, stress spread across a young market where the investor base overlaps heavily.

Strive says reserves were not hit

Strive’s leadership called the episode the hardest day yet for digital credit. Even so, they rejected the idea that prices reflected weaker issuer credit. The cause, they argued, was leverage rather than fundamentals.

When markets move against leveraged holders, forced selling can create a cascade. Prices fall, margin calls increase, more selling occurs, and the cycle feeds on itself.

-Strive Chief Executive Matt Cole, via CoinCentral

Strive said its dividend reserves stayed intact. Supporters of Strategy made a similar case for STRC. They argued the balance sheet had not changed simply because the share traded lower.

The lower price also lifted the yield for new buyers. A preferred share pays the same stated dividend wherever it trades. So an investor buying near $85 earns more than one who bought at par, plus potential upside toward $100.

That math helped pull buyers back after the steepest selling. STRC and SATA both bounced from their lows. Many investors read the move as forced selling rather than a permanent repricing of either issuer.

The next yield trade will cost more

The recovery does not erase the lesson. Brokers, issuers, and investors now have less room to treat these shares as quiet income. Brokerages are likely to review margin rules after the unwind.

Tighter requirements would make large borrowed positions harder to build. That change cuts the risk of another clustered selloff. However, it also reduces the appeal of using the shares to magnify yield.

Issuers may need stronger defenses too. Larger reserves, clearer buybacks, and higher call premiums could reassure buyers. Yet each fix carries a cost, because richer terms make the securities more expensive to run.

The sell-off provided a clearer measure of the risk. A preferred share tied to a Bitcoin treasury can keep paying out while still falling hard. In short, a product built to soften volatility can still transmit panic when leverage builds around it.

Digital Credit is still in its infancy. It is better for the market to experience and learn from these dynamics now, while the market remains relatively small.

Strive Chief Executive Matt Cole, via CoinCentral

For now, both shares trade below par as Bitcoin hovers near $63,000. The trade survived its first real stress test. The price of stability, though, just went up.