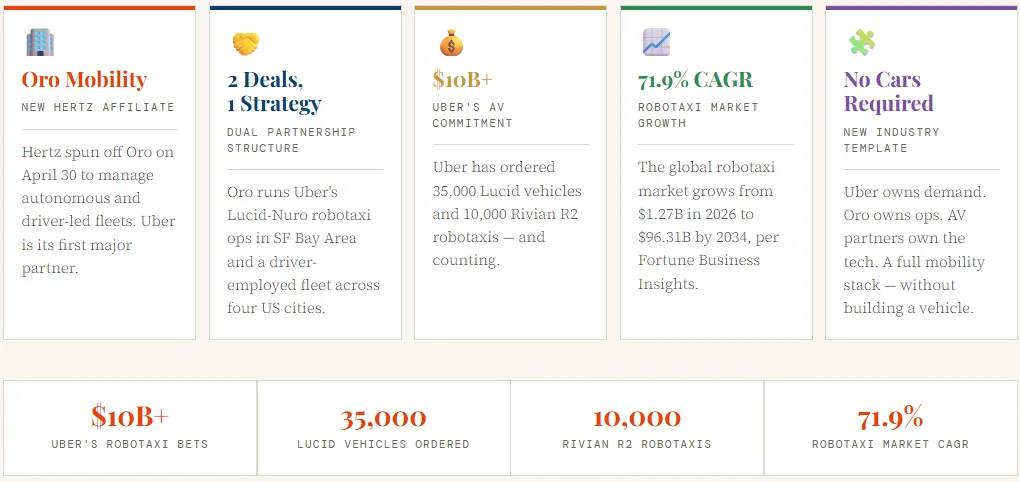

May 03, 2026 – Hertz spun off Oro Mobility on April 30. It now manages Uber’s autonomous and driver-led fleets. The deal positions both companies in a market expected to reach $96 billion by 2034.

Hertz and Uber announced two strategic fleet partnerships on April 30, 2026. The partnerships operate through Oro Mobility, a newly formed Hertz affiliate. Oro will manage Uber’s autonomous robotaxi fleet. It will also operate a driver-led rideshare service. This dual mandate reflects Uber’s push to build a hybrid mobility network at scale.

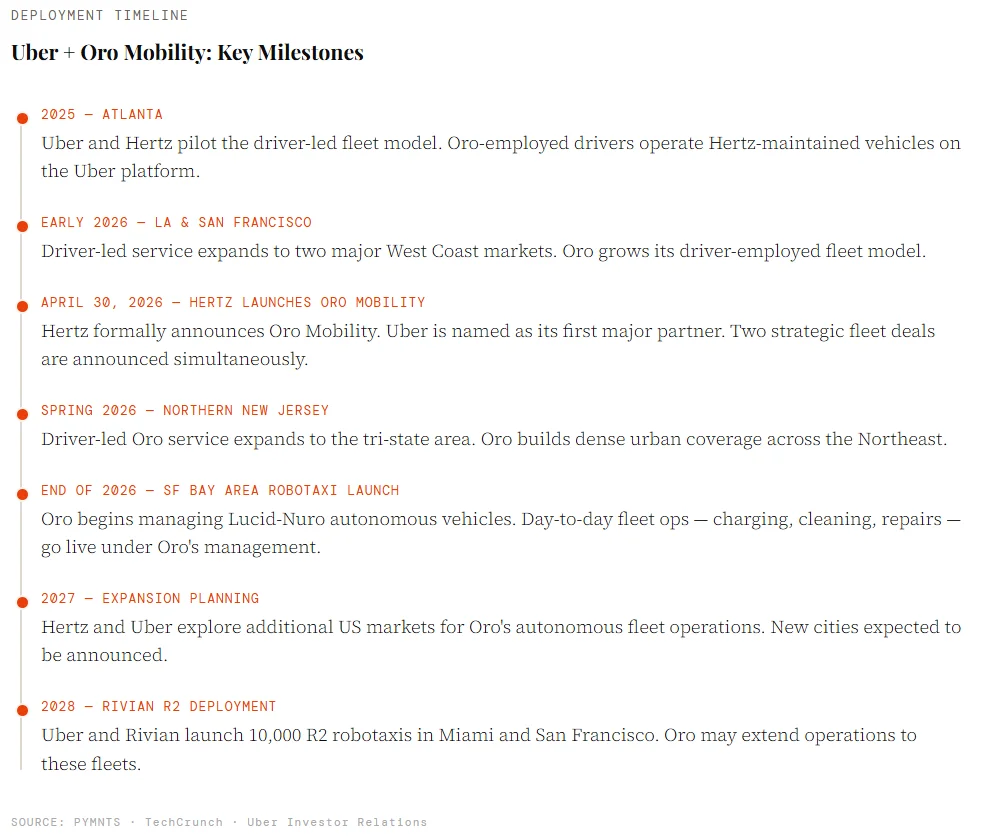

The autonomous arm is the headline act. Oro will handle charging, maintenance, repairs, cleaning, and depot staffing. The vehicles are Lucid Gravity SUVs equipped with Nuro’s Level 4 autonomous driving technology. Commercial launch is set for the San Francisco Bay Area by year-end 2026.

What Is Oro Mobility and Why Does It Matter?

Hertz created Oro to fill a specific gap. Traditional rental operations do not scale well for autonomous fleets. Robotaxis require constant charging, rotations, and remote depot staffing. They require precision maintenance schedules. Oro is designed around these demands from day one.

Hertz CEO Gil West framed this shift clearly. “This partnership establishes Oro as an integrated solution that connects demand with scalable fleet management services,” he said in the official press release. Hertz is not just a rental company anymore. It is becoming the operational backbone for autonomous mobility.

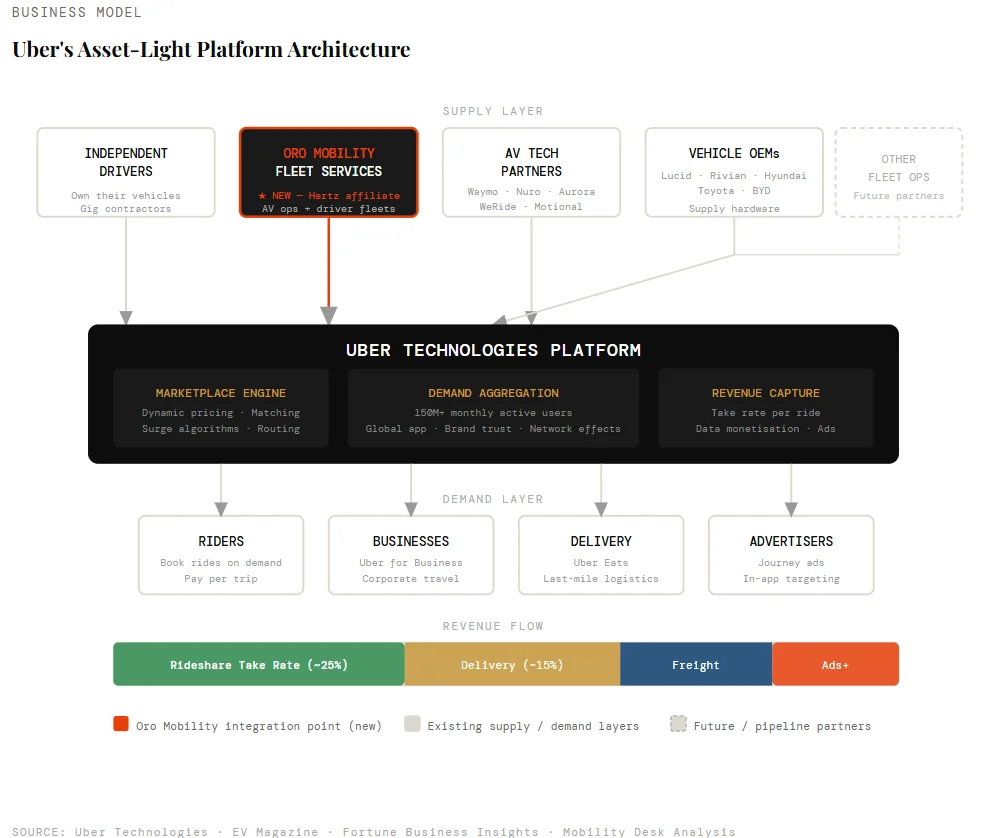

For Uber, the logic is equally sharp. Running physical fleet operations is expensive and distracting. Outsourcing this to a specialist lets Uber focus on its platform, pricing, and demand aggregation. Uber President and COO Andrew Macdonald said the goal is a “seamless, high-quality rider experience across the entire mobility ecosystem.”

By combining Uber’s global platform leadership with Oro’s dedicated fleet expertise, we are well equipped to meet rising rideshare demand.

— Andrew Macdonald, President & COO, Uber

Uber’s $10 Billion Robotaxi Bet By the Numbers

This partnership does not exist in isolation. Uber has committed over $10 billion to autonomous vehicle ventures. This figure includes more than $2.5 billion in equity stakes and over $7.5 billion earmarked for robotaxi fleet orders.

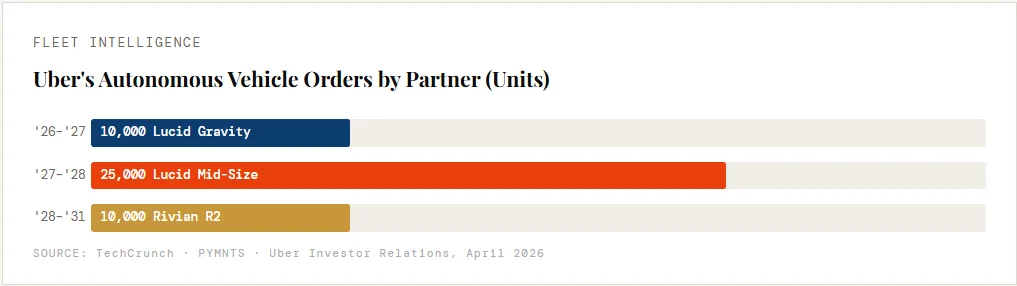

The Lucid relationship alone is massive. Uber has ordered at least 35,000 robotaxi-ready vehicles from Lucid Motors. It starts with 10,000 Gravity SUVs. Another 25,000 units will use Lucid’s upcoming mid-sized platform. Nuro provides the Level 4 autonomous stack for these vehicles.

Separately, Uber and Rivian announced a deal in March 2026. They will deploy 10,000 fully autonomous Rivian R2 robotaxis. Launch cities are Miami and San Francisco in 2028. Expansion to 25 cities by 2031 is on the roadmap.

The Robotaxi Market: Why the Stakes Are This High

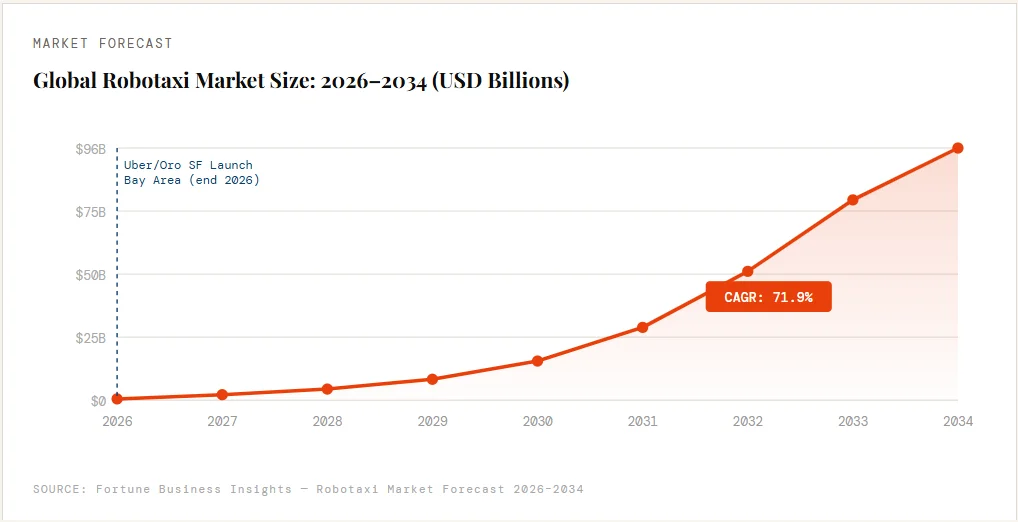

These deals are not speculative bets. They track a market that analysts expect to explode. The global robotaxi market is valued at $1.27 billion in 2026. It is projected to reach $96.31 billion by 2034. That is a compound annual growth rate of 71.9%.

North America currently dominates. It held a 54% market share in 2025. The US cities of San Francisco, Phoenix, and Austin are the key proving grounds. Waymo leads commercial deployments. But Uber is the platform that enables multiple AV partners to reach consumers at scale.

Two Partnerships, One Unified Strategy

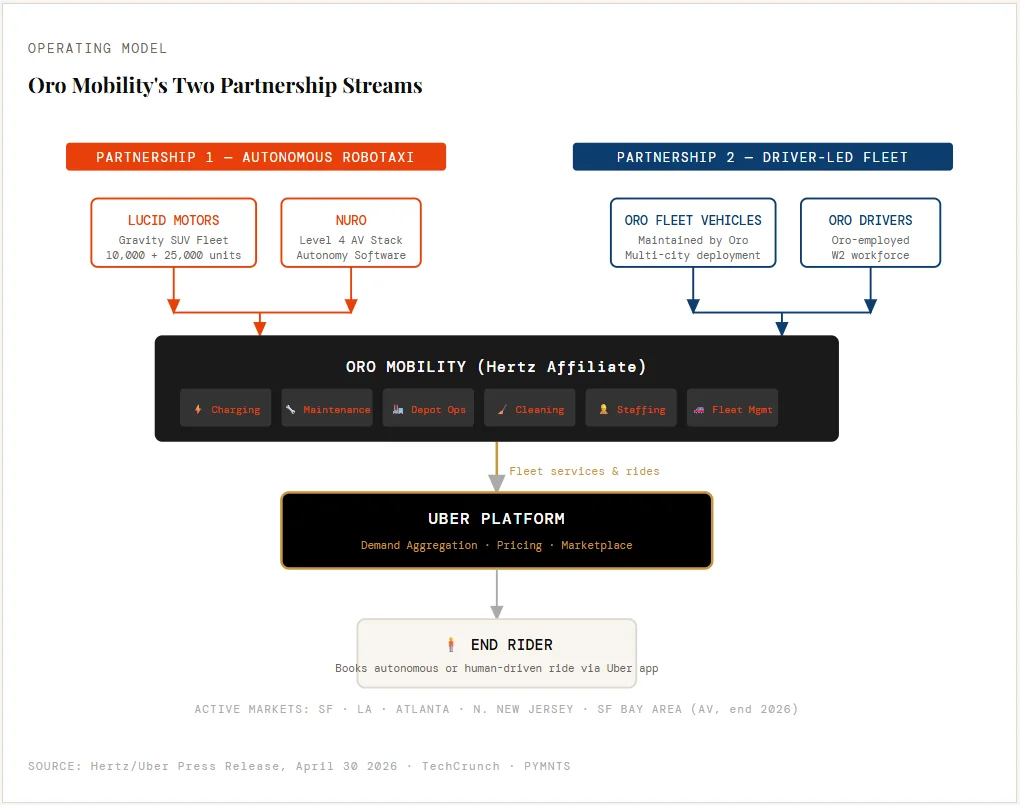

The Oro-Uber arrangement actually covers two distinct services. Understanding both is key to grasping Hertz’s pivot.

Partnership One: Autonomous Robotaxi Operations: Oro manages the physical lifecycle of Uber’s self-driving Lucid vehicles. This includes daily charging cycles, scheduled maintenance, and on-demand repairs. Depot staffing is also Oro’s responsibility. The San Francisco Bay Area is the pilot market.

Partnership Two: Driver-Led Fleet Services: Oro employs its own drivers. These drivers operate Oro-maintained vehicles on the Uber platform. This model was already piloted in Atlanta in 2025. It has since expanded to Los Angeles and San Francisco. Northern New Jersey is next, launching this spring.

Visualising the Oro Operating Model

The two partnerships have distinct supply chains. Both feed into one outcome: rides on the Uber platform. The diagram below maps how each stream works from the vehicle and technology supplier through to the end rider.

Uber’s Platform Business Model, Visualised

Uber does not own cars. It does not employ most drivers. Its power is in the marketplace. The diagram below shows how Uber’s asset-light model connects supply partners, fleet operators, and riders and where Oro now fits inside this structure.

What This Means for the Industry

The Uber-Oro partnership creates a new template for autonomous fleet operations. Ride-hailing platforms need more than algorithms. They need physical infrastructure maintenance hubs, charging depots, and trained staff. Oro proves that legacy vehicle companies can evolve into this role.

Hertz’s transformation is remarkable. The company emerged from bankruptcy in 2021. Now it is engineering a future as the operational engine of autonomous mobility. The Oro structure separates this high-growth business from Hertz’s legacy rental operations. This gives it room to move faster and attract dedicated investment.

For Uber, the hybrid network model is now a concrete reality. Human-driven and autonomous vehicles will coexist on the platform. Oro enables both. As autonomous technology matures, the balance will shift. But Uber’s platform captures the revenue regardless of who or what is driving.

Competitors will take note. Lyft, Waymo, and traditional automakers now face a vertically coordinated rival. Uber controls demand aggregation. Oro controls fleet operations. Partners like Lucid, Nuro, and Rivian supply the vehicles and autonomy stack. This is a full-stack mobility supply chain assembled without building any cars.