April 22, 2026 – Two Wall Street giants are taking different paths to capture a market that could reach $4 trillion by 2030.

In Summary

JPMorgan’s Kinexys platform now clears more than $5 billion in tokenised transactions daily.

Citigroup is expanding Citi Token Services through a partnership with Coinbase, set to take effect in October 2025.

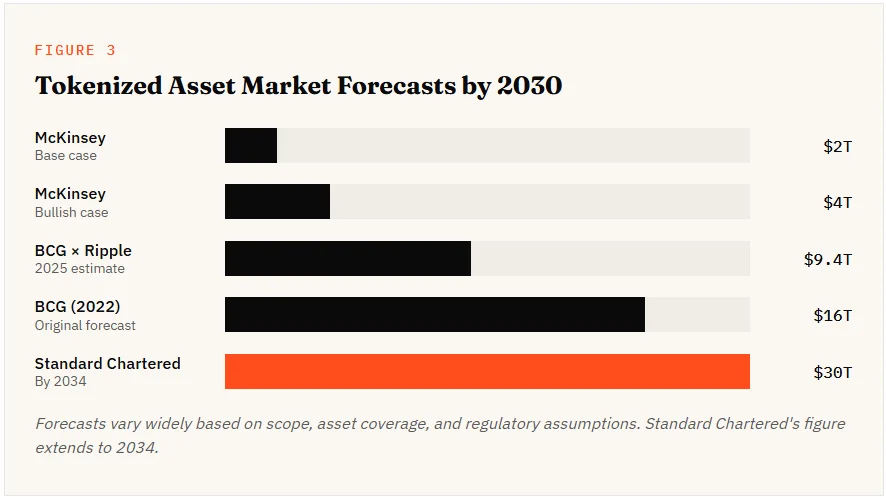

McKinsey projects the tokenized asset market could reach $2 trillion by 2030, or $4 trillion in a bullish case.

America’s two largest banks are locked in a fresh rivalry. This time, the battleground is blockchain infrastructure. JPMorgan Chase and Citigroup are racing to dominate tokenized payments. Both want to redefine how trillions of dollars move globally.

A Bloomberg News report, highlighted by PYMNTS, detailed their diverging strategies on April 20. Each bank is chasing the same prize through different routes. The prize is a 24/7 payment system.

JPMorgan Doubles Down on Kinexys

JPMorgan’s strategy centers on its in-house platform, Kinexys. The platform now processes more than $5 billion in daily transactions. It has handled over $3 trillion in cumulative volume since inception. Payment transactions on Kinexys have also grown 10x year over year.

Kinexys powers JPM Coin, the bank’s tokenized deposit product. In June 2025, JPMorgan launched a new deposit token called JPMD. The token went live on Base, a public blockchain built by Coinbase. This marked a major shift toward public blockchain rails.

JPMD is available only to institutional clients. Unlike most stablecoins, it can pay interest to holders. It also integrates seamlessly with the bank’s legacy systems.

Umar Farooq leads JPMorgan Payments globally. He told Bloomberg he remains cautious about private stablecoins. Farooq argued that issuers “should be regulated more like banks.” He warned that some issuers take a “lightweight” approach to compliance. He flagged weaker KYC controls as a particular risk.

“If you’re taking the same sort of risk, you should have the same sort of regs.

-“Umar Farooq, Global Co-Head of JPMorgan Payments

Citi Bets on Open Partnerships

Citigroup is pursuing a more open, partnership-led strategy. The bank has expanded Citi Token Services to handle 24/7 flows. In October 2025, it announced a major deal with Coinbase. The partnership targets digital asset payment rails for institutions.

The initial phase streamlines fiat payments. Future plans include faster cross-border settlement using stablecoins. The tie-up extends Citi’s “network of networks” strategy.

Citi already banks 90% of the world’s top e-commerce firms. It also serves 15 of the 20 largest global fintechs. The bank operates across 94 markets and 300 payment networks. That distribution gives Citi a broad reach for new tokenized products.

Shahmir Khaliq heads Citi’s global services division. He said Citi’s goal is seamless 24/7 cross-border money movement. Khaliq believes the partnership approach gives Citi a “leg up.”

Two Models, One Market

The two strategies reflect a deeper industry debate. JPMorgan favors permissioned, bank-controlled rails with tight compliance. Citigroup prefers open collaboration with crypto-native firms. Both models serve institutional clients first.

Stablecoins remain the dominant on-chain cash today. Their combined market cap topped $265 billion in mid-2025. Cross-border payments alone represent a $40 trillion annual market. Banks see tokenized deposits as their path back to relevance.

Tokenized deposits can offer interest and full banking protections. Stablecoins typically do not offer either benefit. Farooq noted that bank-led tokens also carry decades of compliance infrastructure.

The Market Is Small but Growing Fast

Tokenized payment volumes remain tiny next to traditional rails. Global payments still flow mostly through Fedwire and SWIFT. However, the growth projections are striking.

McKinsey estimates the tokenized asset market will reach $2 trillion by 2030. In a bullish scenario, it could hit $4 trillion. Some analysts push projections even higher. Standard Chartered sees up to $30 trillion by 2034.

Both executives see AI-driven “agentic commerce” as the next catalyst. In this world, AI agents transact autonomously on behalf of users. Khaliq said the coming years will “change radically.”

What It Means for Banks

The JPMorgan-Citi rivalry signals a broader shift on Wall Street. Banks no longer view crypto infrastructure as peripheral. They now treat it as core payments infrastructure.

Regulation will shape the eventual winner. New stablecoin rules in 2025 raised compliance bars across the sector. Banks hope their legacy compliance muscle will prove decisive.

For corporate treasurers, the choice matters immensely. Programmable, 24/7 money can unlock capital efficiency. It can also reduce cross-border settlement risk.

JPMorgan’s walled garden may win, or Citi’s open platform may prevail. The outcome remains uncertain. What is clear is that tokenized payments are no longer experimental. They now sit at the heart of global banking strategy.