May 07, 2026 – Canada’s largest fintech partners with Visa Canada on a stablecoin settlement pilot. The move makes Wealthsimple the first Canadian institution to use USDC for institutional-grade payment settlement.

In Summary

Wealthsimple is Canada’s first financial institution to settle obligations with Visa using USDC stablecoin.

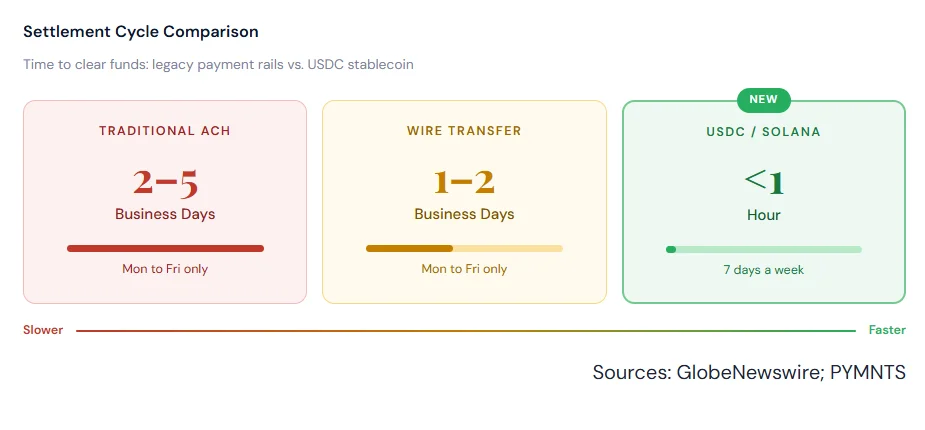

The pilot enables 7-day settlement, breaking the traditional 5-day banking cycle.

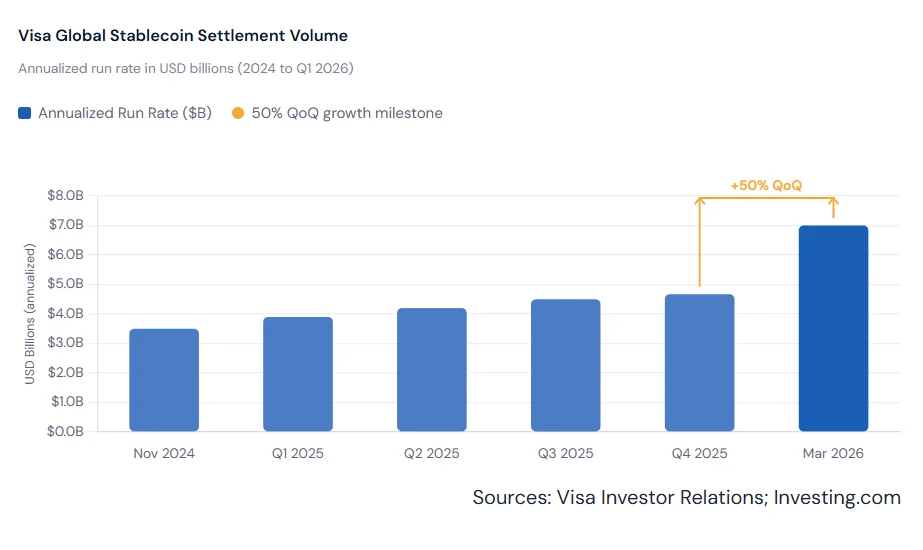

Visa’s global stablecoin settlement hit a $7B annualized run rate in March 2026, up 50% in one quarter.

Wealthsimple manages $100B in assets and serves 4 million Canadians, providing a significant scale test.

Canada’s planned stablecoin regulations, announced in the 2025 federal budget, are still pending.

Wealthsimple and Visa Canada announced on May 5, 2026, the launch of a stablecoin settlement pilot. This makes Wealthsimple the first Canadian financial institution to use USD Coin (USDC) for institutional settlement. The program runs on Visa’s existing network. It allows Wealthsimple to meet certain payment obligations using stablecoin instead of fiat.

The pilot does not change how consumers pay. Cardholders continue using their Visa cards normally. Only the back-end transfer mechanism changes. This distinction matters for understanding the true scope of the program.

A New Way to Move Money in Canada

Traditional payment settlement between financial institutions takes two to five business days. Banks do not process transfers overnight, on weekends, or during holidays. This delay creates real friction. Businesses must wait days to access funds needed for operations.

Canada has also struggled to build a modern, real-time rail system. The country’s fast-payments infrastructure has faced repeated delays. Stablecoin settlement offers a practical workaround. Under this pilot, settlement occurs seven days a week. Transactions are completed near-instantly on the blockchain infrastructure.

“Stablecoins represent a fundamental shift in how money moves, faster, smarter, and without the constraints of legacy systems.

-“Hanna Zaidi, VP Payments Strategy and Chief Compliance Officer, Wealthsimple

Wealthsimple conducted the pilot using virtual US-dollar credit cards. A small group of volunteer employees made real purchases. Settlement occurred between Visa and Wealthsimple in the USDC. All transactions cleared instantly. No delays occurred, even during weekend testing hours.

Visa’s Stablecoin Momentum Is Growing Fast

Visa is not a newcomer to stablecoin settlement. The company first experimented with USDC on its network in 2021. It expanded into a Solana-based settlement in September 2023, adding partners such as Worldpay and Nuvei.

In December 2025, Visa officially launched USDC settlement in the United States. Cross River Bank and Lead Bank were the first US partners. Since then, volume has grown sharply. Visa’s global stablecoin settlement volume reached a $7 billion annualised run rate as of March 2026, up more than 50% from the prior quarter.

Settlement Cycles: Old vs New

The efficiency gains from stablecoin settlement are measurable. Traditional Visa settlement runs on a five-day cycle and is limited to standard banking hours. Stablecoin settlement expands this to seven days. It also removes the hard stop at 5 PM on Fridays.

Fewer intermediaries are involved in each transfer. This reduces both cost and risk of processing errors. For a company like Wealthsimple, faster settlement directly improves liquidity. The company can manage funding across its platform more efficiently.

Compliance Was Central to the Design

One concern around stablecoin adoption is regulatory risk. Wealthsimple addressed this directly. The company ran the pilot under its standard compliance and risk-management processes. No new frameworks were created for the test.

“We wanted to show that regulated financial institutions could transact using stablecoins,” said Zaidi. “There is a lot of scepticism in the space. Here is Visa and Wealthsimple engaging in this pilot, and it was successful.” The compliance-first approach is significant. It shows other Canadian institutions a viable path to adoption.

“We expect that other Canadian banks and fintechs will absolutely start to follow. This lays the framework and the foundation for them to do that.”

– Chris Ferron, VP Fintechs, Enablers and Merchants, Visa Canada

What Comes Next for Canada

The Canadian pilot is not an isolated event. Visa operates active stablecoin settlement pilots across Latin America, Europe, Asia Pacific, and the Middle East. The Canada launch extends a proven model to a new market.

The broader rollout in Canada depends on two factors. First, regulatory clarity from Ottawa is needed. The government announced plans for stablecoin regulation in the fall 2025 federal budget. Rules are not yet final. Second, market appetite among other Canadian banks will determine scale.

Visa has more than 14,000 financial institutions in its global network. The Canadian pilot sets a template. If Wealthsimple’s results hold up, Canadian banks face a clear choice. They can adopt stablecoin settlement early or risk falling behind on efficiency.

For consumers, the benefits are indirect but real. Faster settlement means faster fund availability. Lower operational costs for institutions can translate to lower fees. The path from pilot to mainstream is long. However, Wealthsimple and Visa have taken the first step.