June 07, 2026 – America’s largest lenders plan a shared blockchain payment system for 2027. However, analysts suggest the timing signals defense more than innovation.

In Summary

JPMorgan, Bank of America, Citigroup, and Wells Fargo are building a joint tokenized deposit network.

The Clearing House will operate the infrastructure, targeting an H1 2027 launch.

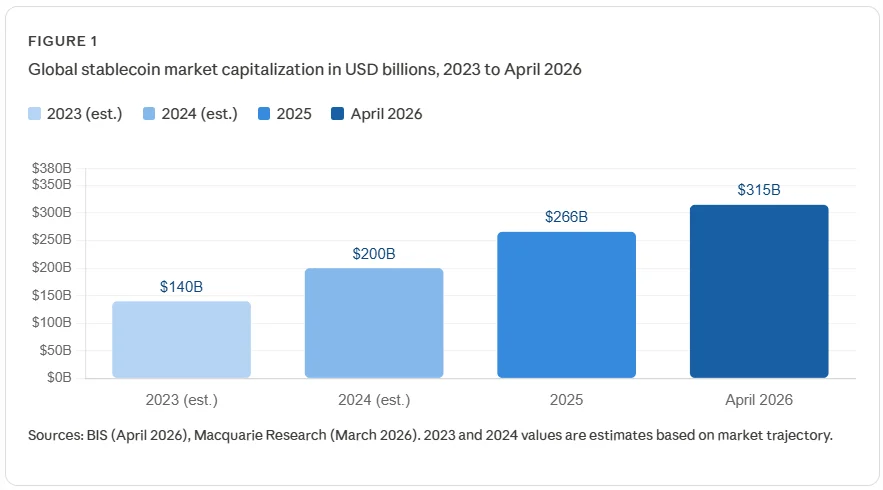

The global stablecoin market cap exceeded $315 billion in April 2026, up 50% year-over-year.

Standard Chartered warns stablecoins could drain $500 billion from bank deposits by 2028.

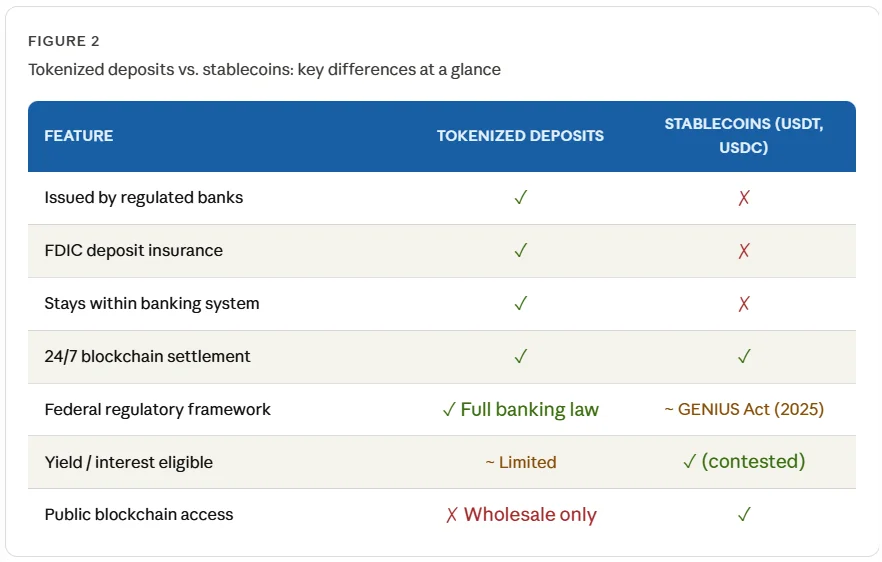

Tokenized deposits are insured by the FDIC and differ fundamentally from private stablecoins.

America’s largest banks are striking back at stablecoins. JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo are jointly building a tokenized deposit network. The system targets a launch in the first half of 2027. The Clearing House, a bank-owned payments company, will operate the infrastructure. These institutions represent the core of U.S. commercial banking. However, the urgency behind this move reveals deeper competitive pressure. Crypto firms are pushing into core banking territory under a favorable regulatory climate.

How the new network will work

The network digitizes traditional bank deposits on a shared blockchain ledger. It connects existing payment rails with digital asset infrastructure. Therefore, tokenized deposits will settle instantly and continuously, 24 hours a day. Large multinational corporations will likely dominate early adoption. Key use cases include programmable treasury operations and real-time liquidity management. Furthermore, cross-border payments represent a major commercial target for the system.

Importantly, these digital tokens are not stablecoins. These are standard bank deposits represented on a blockchain in digital form. Additionally, they carry the same regulatory protections as ordinary bank accounts. The banks have not yet selected a blockchain vendor for the project. The Clearing House CEO David Watson described the move as “a big move for the banks.” He told The Wall Street Journal that the industry now faces a “radically different” future around on-chain payments.

The stablecoin threat is real

The stablecoin market has grown at a remarkable pace over three years. Macquarie confirmed the global stablecoin market cap reached approximately $312 billion in March 2026. That figure represents roughly 50% growth year-over-year. Furthermore, the Bank for International Settlements confirmed the market stood at around $315 billion in early April 2026. Adjusted stablecoin transfer volume hit an estimated $11 trillion in 2025 alone. Additionally, Accenture’s 2026 Banking Trends report found stablecoin volumes now surpass Visa’s. Therefore, banks face genuine and growing competitive pressure.

The threat extends well beyond market size. Standard Chartered warns that stablecoin growth could drain $500 billion in bank deposits by 2028. The bank estimates roughly one-third of total stablecoin value will come at the direct expense of traditional deposits. Regional banks face the steepest risk to their profit margins. Moreover, the GENIUS Act, signed into law in July 2025, provided crypto firms with a clear federal path to mainstream payments. Consequently, banks moved quickly to develop a structured response.

“The industry faces a radically different future around on-chain payments and finance.”

-David Watson, CEO, The Clearing House

Tokenized deposits vs. stablecoins

Many observers confuse tokenized deposits with stablecoins. However, they are fundamentally different instruments. Stablecoins, such as Tether’s USDT, are issued by private companies. These operate entirely outside the traditional banking system. Tokenized deposits, by contrast, remain inside the banking system. They carry FDIC deposit insurance and have an identical credit risk profile to ordinary deposits. Furthermore, they follow the same accounting standards as conventional bank accounts.

The regulatory distinction matters considerably. Pending legislation has left room for interest-like yield structures on stablecoins. Banks strongly oppose that feature. Therefore, tokenized deposits offer a cleaner regulatory position for traditional lenders. Citi’s head of services, Shahmir Khaliq, described the network as a step that effectively cements banks’ role in financing and capital markets.

JPMorgan’s head start

JPMorgan already operates an internal tokenized deposit system called JPM Coin. Recently, the bank extended a version of that system to Base, a public blockchain connected to Coinbase. JPMorgan designed that extension specifically for institutional clients. Therefore, it enters the Clearing House network with proven real-world experience. The new shared network will bring similar capabilities to banks across the entire United States.

Nevertheless, Bank of America’s head of global payments, Mark Monaco, offered a measured view. He acknowledged that clients are not “beating down the door” for tokenized deposits today. However, Monaco argues that banks must be positioned when demand eventually builds. “With any sort of new adoption, it takes time,” he said. The broader launch signals institutional intent, not immediate consumer demand.

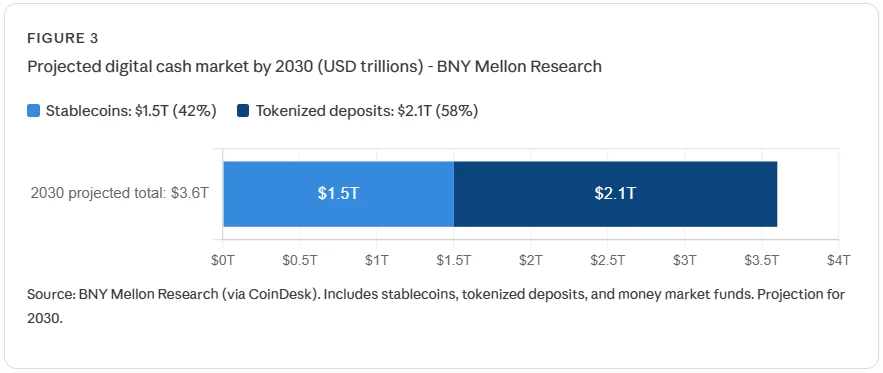

What the market looks like in 2030

BNY Mellon projects the combined stablecoin and tokenized cash market will reach $3.6 trillion by 2030. That forecast includes $1.5 trillion in stablecoins and approximately $2.1 trillion in tokenized deposits and money market funds. Furthermore, analysts widely expect coexistence rather than a single dominant winner. Tokenized deposits will likely serve wholesale and institutional payment markets. Stablecoins will likely lead in retail payments and decentralized finance. Therefore, banks and crypto firms may ultimately occupy complementary lanes rather than compete head-to-head.

The banks have not ruled out issuing stablecoins themselves if market demand grows large enough. For now, the tokenized deposit network represents the industry’s opening move in a rapidly changing landscape. Consequently, the race to define the future of digital money is accelerating faster than most expected.