Table of Contents

- Table of contents will be generated automatically when the page loads.

In Summary

1. Bonds are a natural fit

Fixed terms, regular payouts, and clear legal rules make them ideal for smart contracts.

2. Fractional ownership opens doors

Minimums can drop from $100K+ to as low as $10, letting more people take part

3. Settlement goes from days to seconds

Atomic settlement (T+0) replaces the old T+2 cycle, cutting risk and freeing up capital.

4. Costs drop sharply

Studies show up to 41% savings by removing middlemen and manual checks.

5. Major players are already on board

EIB, HSBC, Hong Kong, and the UK have issued billions of tokens in bonds.

6. It’s evolution, not revolution

The bond stays a bond. Tokenisation simply removes the friction around it.

The global bond market is worth over $140 trillion. It funds governments, corporations, and infrastructure worldwide. Yet, buying and selling bonds still rely on slow settlement cycles, layers of intermediaries, and high minimum investments. Bond tokenisation is changing that equation.

In Stories 1 through 5, we explored why tokenisation matters, what it is, how it works, the infrastructure behind it, and the different types of tokens. Now, let’s look at the first real-world use case gaining serious institutional traction: tokenised bonds.

Why bonds are ideal for tokenisation

The global bond market is worth over $140 trillion. As a result, it funds governments, businesses, and major projects worldwide. However, buying and selling bonds still rely on slow settlement, multiple middlemen, and high entry costs. That is why bond tokenisation is changing the game.

In Stories 1 through 5, we covered why tokenisation matters, what it is, how it works, the tech behind it, and the different types of tokens. Now, let’s look at the first real-world use case gaining serious traction: tokenised bonds.

Why bonds are a perfect fit

Bonds have fixed terms, regular payouts, and clear legal structures. Because of this, they are a natural match for smart contract automation. Tokenised bonds could enable near-instant settlement, cutting delays and risk, while programmable platforms boost market trust. Bank for International Settlements

Think of it this way. A standard bond is like a paper contract locked in a filing cabinet. In contrast, a tokenised bond is the same contract stored on a shared digital ledger that updates in real time. In other words, the rights stay the same. Only the delivery method improves.

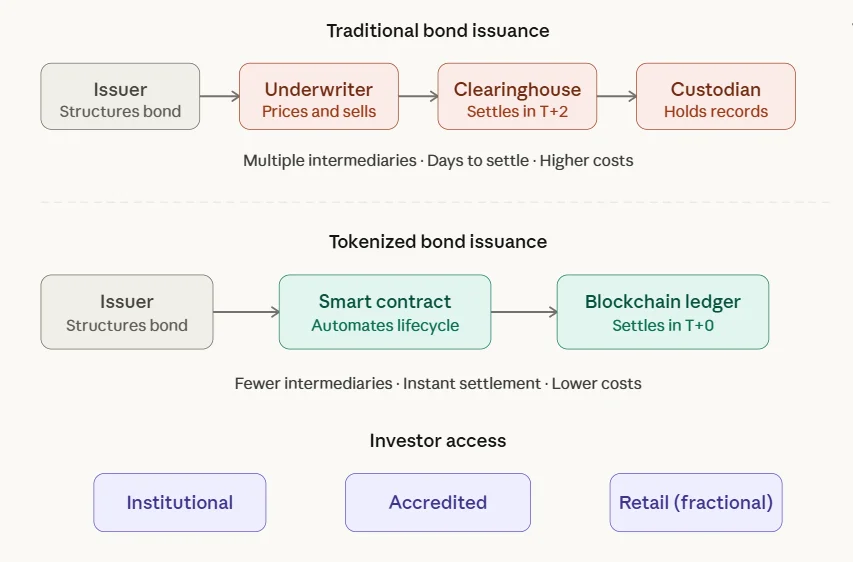

Here’s how the old process compares with the new approach:

Four pillars of bond tokenization

Four pillars of bond tokenization

First, fractional ownership. Standard corporate bonds often need a minimum buy-in of $100,000 or more. As a result, most small investors are shut out. In Singapore, however, OCBC became the first bank to offer tokenised bonds to accredited investors, dropping the minimum from S$250,000 to just S$1,000. Investax. This means more people can now take part in fixed-income markets.

Second, faster settlement. Standard bond markets settle trades on a T+2 basis, meaning it takes two business days to close a deal. Tokenised bonds, on the other hand, can settle almost immediately via atomic settlement on the blockchain. As a result, this cuts risk and frees up capital much faster.

Third, lower costs. A study of the ODDO BHF bond found that tokenisation reduced costs by 41.5% by eliminating manual checks and middlemen.

Finally, built-in openness. Smart contracts handle coupon payments and payouts at maturity on their own. Moreover, every trade is logged in real time on the blockchain, giving a full, clear record of who owns what.

Who is already doing this?

Bond tokenisation is not just a theory. In fact, major players are already issuing tokenised bonds at scale.

According to the Bank for International Settlements, more than 60 tokenised bonds have been issued so far, adding up to $8 billion in total value. For instance, the European Investment Bank has led the way by launching several digital bonds, including a landmark £50 million sterling bond on the HSBC Orion platform. Similarly, Hong Kong issued the world’s first government-backed tokenised green bond worth HK$800 million, blending green finance goals with blockchain.

Furthermore, HSBC Orion has powered over $3.5 billion in digital bonds worldwide and was recently chosen as the platform for the UK’s Digital Gilt pilot. On top of that, by March 2026, tokenized U.S. Treasuries alone reached $11 billion, nearly three times the year before.

DLT-based fixed-income issuance hit €3 billion in 2024, a 260% jump from the prior year. Clearly, the trend has moved from testing to real-world use.

What does this mean for you?

Bond tokenisation is not about tearing down the bond market. Instead, it is about making it work better. Because of these changes, smaller investors gain access to assets once held only by large firms. At the same time, settlement gets faster, costs drop, and records become clearer.

As the BIS notes, tokenisation can boost market speed, reduce settlement risk, broaden investor access, and spur new financial products. Bond tokenisation is about making things faster and fairer, not about causing upheaval. The bond stays a bond. The technology simply removes the friction around it.

Next in the series, Story 7: We’ll explore another powerful use case: Real Asset Tokenisation.