April 29, 2026 – A landmark Juniper Research report reveals cross-border B2B stablecoin payments will leap from $13.4 billion in 2026 to $5 trillion by 2035. Correspondent banking faces its biggest disruption yet.

In Summary

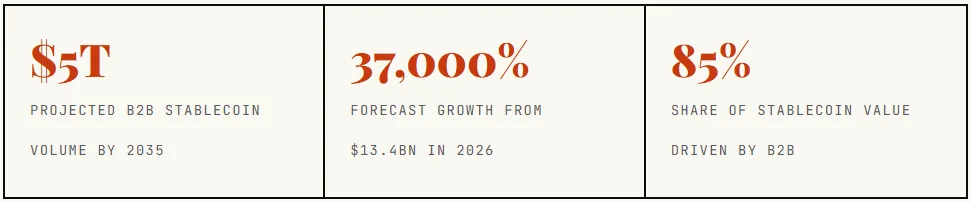

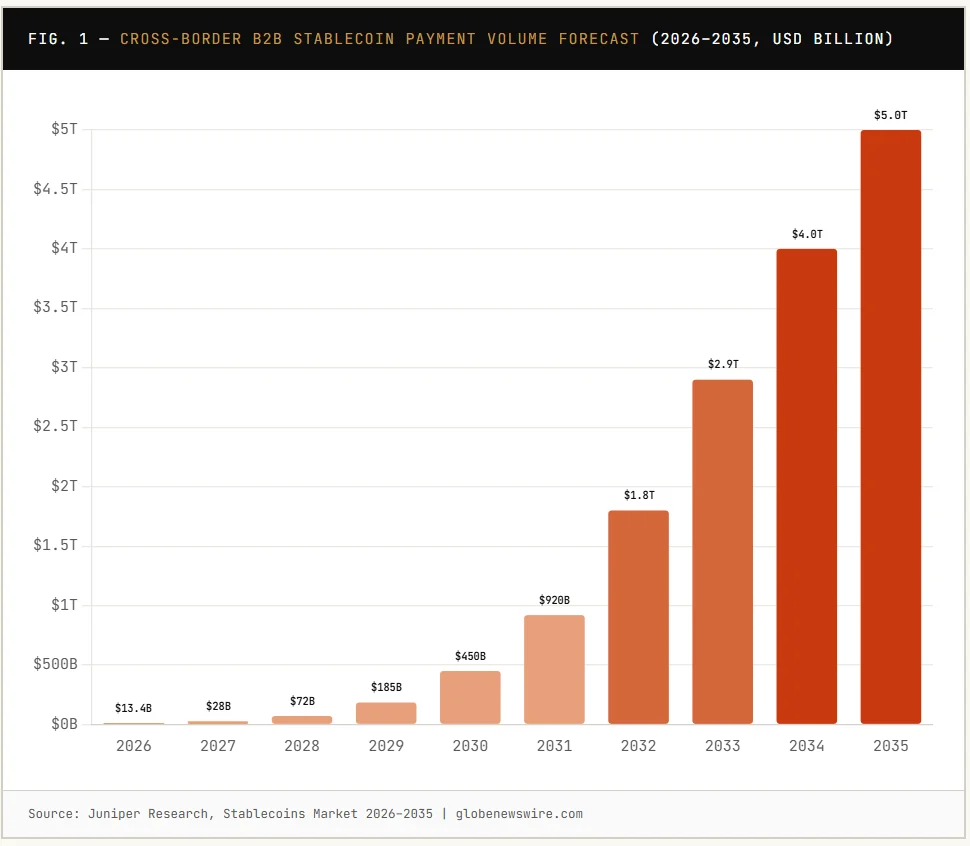

37,000% growth in nine years. Cross-border B2B stablecoin payments will surge from $13.4 billion in 2026 to $5 trillion by 2035, per Juniper Research.

B2B dominates the stablecoin economy. By 2035, 85% of all stablecoin transaction value will come from business-to-business use cases, not retail trading.

Correspondent banking is being disrupted. Stablecoins settle near-instantly, 24/7, with no intermediary fees, a direct structural advantage over SWIFT-based rails.

Chainalysis puts total stablecoin volume at $719 trillion by 2035. In an accelerated scenario, that figure climbs to $1.5 quadrillion, rivalling Visa and Mastercard combined.

Institutions are already moving. Stripe acquired Bridge for $1.1 billion. Mastercard acquired BVNK for up to $1.8 billion. Stablecoin infrastructure is becoming core payments plumbing.

Cross-border stablecoin payments are no longer a fringe experiment. A major new study from Juniper Research projects that business-to-business cross-border stablecoin transactions will reach $5 trillion by 2035. That compares to just $13.4 billion in 2026, a staggering 37,000% increase over nine years.

Moreover, the report, titled “Stablecoins Market 2026–2035,” covers over 39,000 data points across 61 countries. Consequently, it stands as the most comprehensive stablecoin market assessment to date. The findings arrive at a pivotal moment for global finance.

Why B2B? The Structural Case for Stablecoins

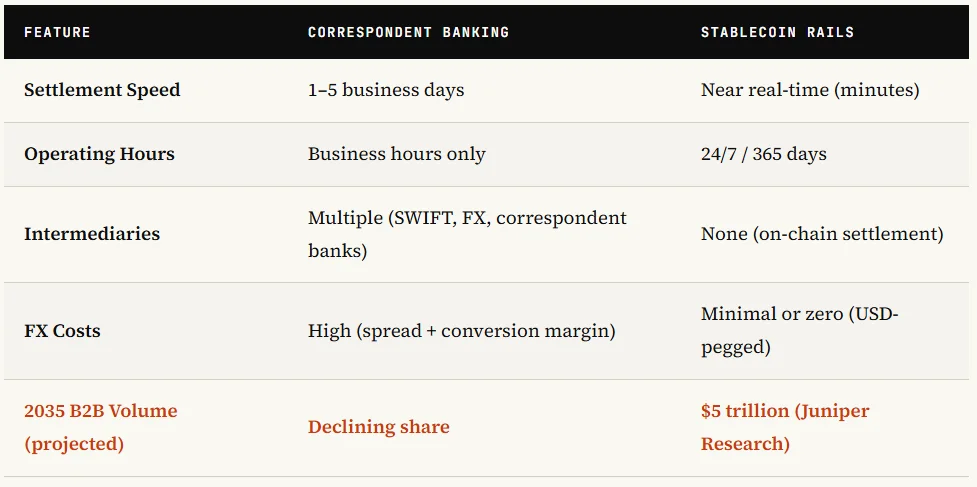

The traditional correspondent banking system is slow. In addition, it relies on multiple intermediaries. Each step adds cost, time, and exchange-rate risk. As a result, settlement can take several days.

Stablecoins, however, offer a direct alternative. Unlike traditional rails, they settle on-chain in near real-time. Furthermore, stablecoin networks operate 24 hours a day, seven days a week, eliminating intermediary fees, SWIFT messaging charges, and FX conversion margins entirely.

Consequently, stablecoins are especially suited to high-value corporate transfers. Juniper identifies treasury operations, supply chain settlements, and international invoicing as key use cases. In particular, dollar-backed stablecoins act as a neutral settlement layer in high-friction corridors.

From Speculation to Infrastructure

Indeed, the shift signals a fundamental change in how markets view stablecoins. For years, fiat-pegged tokens were seen as crypto-trading tools. That era, however, is ending.

Notably, Juniper Research finds that 85% of all stablecoin transaction value in 2035 will come from B2B activity. As a result, retail crypto use will become a minority segment. Stablecoins are therefore becoming the backbone of institutional payment infrastructure.

By 2035, one dollar in every $5 trillion of global B2B cross-border payments could flow through stablecoins. That represents a complete reimagining of corporate treasury operations.

This is further backed by a broader industry trend. Blockchain analytics firm Chainalysis separately projects that adjusted stablecoin transaction volumes will reach $719 trillion by 2035, driven solely by organic growth. Moreover, in a higher scenario, volumes could reach $1.5 quadrillion.

The Competitive Threat to Correspondent Banking

The Juniper report is direct: stablecoins are actively disrupting correspondent banking channels. Rather than merely supplementing them, businesses are already embedding stablecoins into operational workflows, not just as a hedge, but as primary infrastructure.

Furthermore, the case is compelling on cost alone. Traditional cross-border payments carry correspondent fees, FX margins, and messaging charges. By contrast, a stablecoin transfer cuts these to a fraction of conventional cost.

Big Finance Is Already Repositioning

Major institutions are not waiting for 2035. Indeed, they are moving now. According to The Block’s coverage of the Chainalysis report, Stripe acquired Bridge for $1.1 billion, while Mastercard acquired BVNK for up to $1.8 billion. These are not speculative bets; rather, they represent strategic acquisitions of core stablecoin infrastructure.

Similarly, Standard Chartered has flagged that stablecoin usage is rising faster than expected. Meanwhile, UBS and Swiss institutions are piloting franc-denominated stablecoins. In addition, DoorDash now pays drivers and merchants across 40+ countries using stablecoin rails.

As a result, Juniper urges stablecoin issuers to act on this momentum. Specifically, the firm recommends prioritising enterprise integrations and partnerships with treasury management systems. Those who move early will therefore capture the majority of a $5 trillion market.

Regulatory Scrutiny: The Key Risk Factor

Nevertheless, the growth story is not without risk. Regulators are watching closely. BIS General Manager Pablo Hernández de Cos has warned that large USD stablecoins could introduce systemic risks if they expand outside established safeguards.

In the United States, however, the GENIUS Act, signed into law last year, is providing some legal clarity. Consequently, the law signals that policymakers recognise stablecoin infrastructure as a permanent part of the financial system. Clear rules should therefore accelerate institutional entry.

Chainalysis notes that regulatory momentum, combined with a $100 trillion generational wealth transfer between 2028 and 2048, creates a powerful long-term tailwind. As a result, Millennials and Gen Z are increasingly likely to treat crypto rails as a default financial tool.

The Bottom Line

In summary, the Juniper Research forecast is extraordinary in scale. A 37,000% rise in nine years is not a prediction to dismiss lightly. Indeed, the underlying drivers, speed, cost, programmability, and 24/7 availability, are structural advantages, not temporary trends.

For corporate treasurers, payment providers, and bank strategists, therefore, the message is clear. Stablecoins are moving from the margins to the mainstream. Ultimately, the $5 trillion question is not whether this shift will happen, but how quickly institutions choose to lead it.