June 11, 2026 – The new Agent Pay for Machines service lets software buy and settle on its own, across cards, bank accounts, and stablecoins.

In Summary

Mastercard launched Agent Pay for Machines on June 10, 2026.

The network lets AI agents authorize and settle payments automatically.

Settlement runs across cards, bank accounts, and stablecoins.

More than 30 firms back the rollout, including Coinbase and Stripe.

Stablecoins now anchor a market worth roughly $317 billion.

A new payment rail for machines

Mastercard has opened its global network to autonomous software. On June 10, 2026, the company launched Agent Pay for Machines (AP4M). The service lets AI agents authorize, coordinate, and settle payments without a person at checkout. Therefore, machines can now buy services from other machines at high speed.

The launch marks a clear shift in how value moves online. Traditional card payments stay discrete and user-initiated. By contrast, machine payments run continuously in the background. Moreover, many of these transactions involve tiny sums, some worth only fractions of a cent.

Jorn Lambert, Mastercard’s chief product officer, framed the ambition plainly. He said the service could create a “superbloom of AI business models.” In other words, agents may soon transact at speeds and volumes that today’s rails cannot match.

Why agents need their own rails

AI agents have moved well beyond simple advice. Increasingly, they act on human intent and complete tasks end-to-end. For example, an agent could build a flower shop’s website within a set budget. It might buy a domain, hosting, images, and checkout pages on its own. As a result, one request becomes a chain of linked transactions.

Consider a second case from logistics. An agent managing a delivery route could automatically pay for freight. It might also reserve loading access and settle warehouse fees as goods move. Consequently, payments shift from single events to constant background activity.

Human payment systems struggle with this pattern. They were designed for occasional, deliberate purchases. However, agents transact far more often and at far smaller amounts. The industry therefore needs infrastructure that can authorize a non-human buyer.

How Agent Pay for Machines works

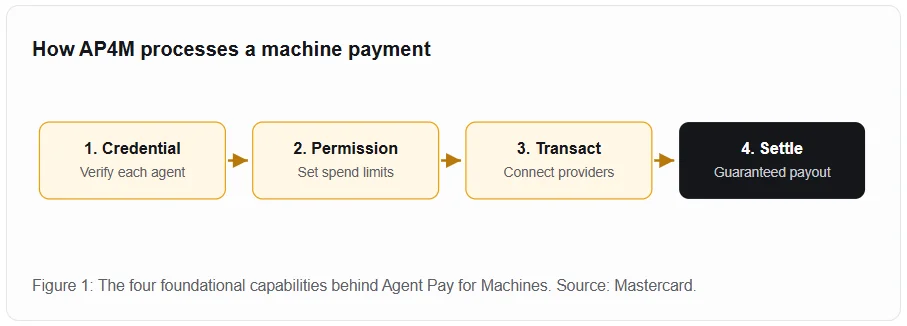

The system relies on four core functions. First, Mastercard credentials every agent so partners can recognize it. Second, organizations set spending limits and authorization rules. These controls run automatically and keep each agent within bounds. Third, verified participants connect and transact across providers. Finally, the network settles payments across multiple rails.

This design aims to bring trust to a chaotic new space. Notably, Mastercard ties the service to its Verifiable Intent technology. That layer confirms an agent is authorized before it acts. In addition, the company guarantees settlement once a transaction clears. Businesses therefore gain confidence that they will get paid.

The stablecoin connection

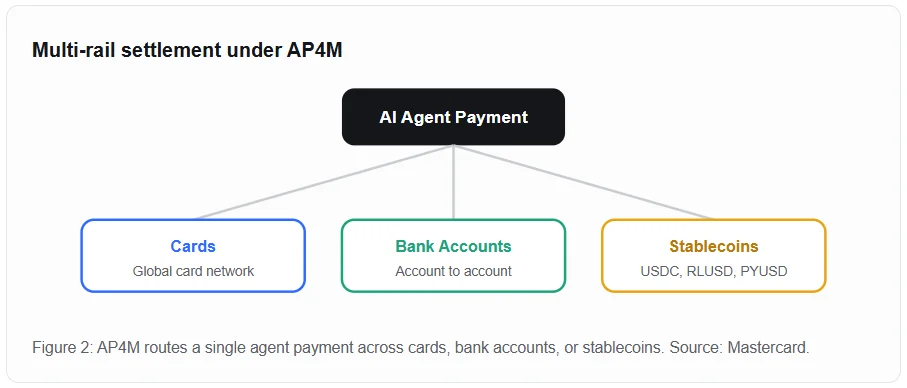

Crucially, AP4M settles across cards, bank accounts, and stablecoins. This multi-rail approach gives the platform a clear crypto dimension. Stablecoins suit machine commerce especially well. They clear quickly, run around the clock, and carry low fees.

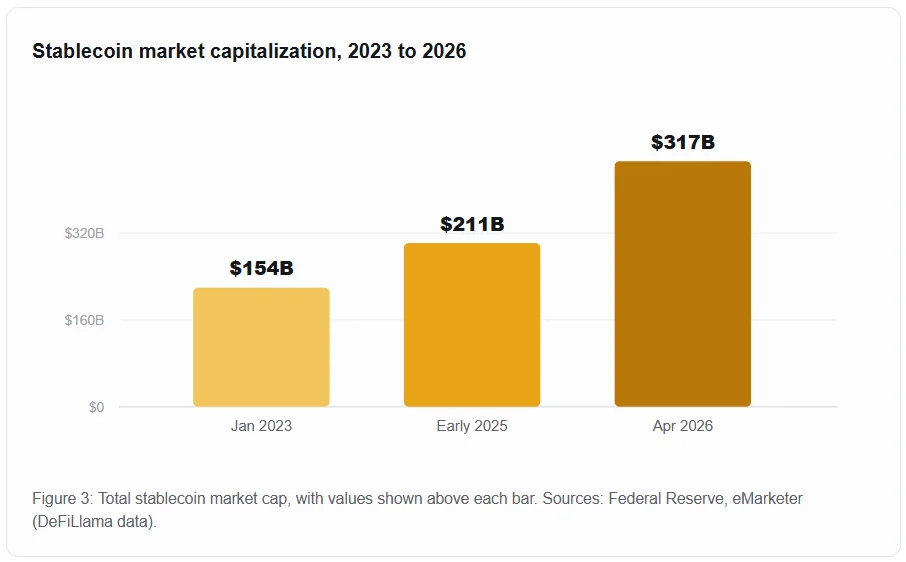

The timing reflects rapid market growth. According to the Federal Reserve, the stablecoin market reached about $317 billion in April 2026. That figure represents more than 50% growth since early 2025. Furthermore, eMarketer data shows the market more than doubled between 2023 and 2026.

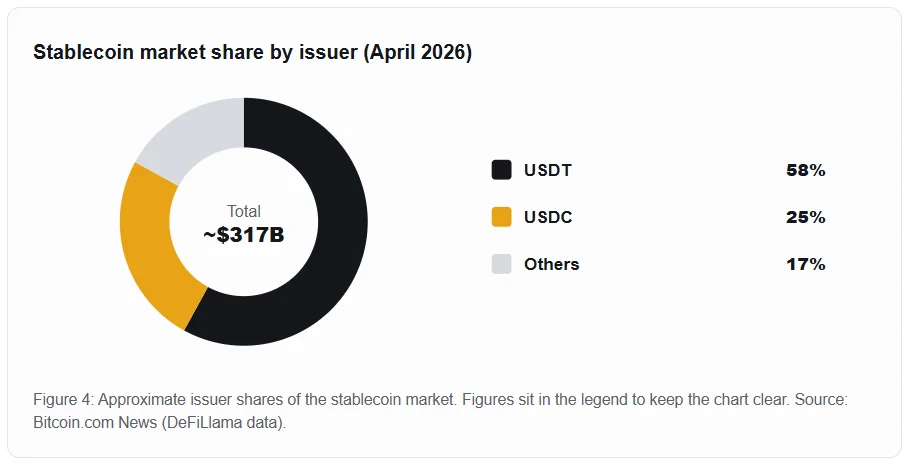

Issuers remain highly concentrated, however. Tether’s USDT held close to 58% of the market in April 2026. Circle’s USDC followed with about $79 billion, according to industry tracking. The chart below breaks down that split.

A crowded partner field

Mastercard did not build AP4M alone. More than 30 firms support the initial rollout. The group spans payments, blockchain, and cloud infrastructure. Coinbase, Stripe, Adyen, Checkout.com, and Cloudflare all joined. Crypto names such as RippleX, Polygon, OKX, and the Solana Foundation also signed on.

These partners bring different strengths to the table. RippleX, for instance, offers the XRP Ledger and its RLUSD stablecoin for settlement. Cloudflare secures the agents themselves. Meanwhile, Coinbase contributes programmable dollars and open standards. Together, they aim to keep the system open rather than closed.

Competition is heating up

Mastercard is not the only player chasing agent payments. Earlier in 2026, Decrypt reported that MoonPay launched a card for AI agents. That product lets agents spend stablecoins at any online Mastercard merchant. Clearly, the race to power autonomous commerce has already begun.

Still, real risks remain. Autonomous spending raises hard questions about fraud and accountability. Who pays when an agent buys the wrong thing? Mastercard answers with credentialing, audit trails, and strict spending caps. Even so, the model will face heavy scrutiny as adoption widens.

What comes next

The agent economy is still young. Yet the building blocks are arriving fast. If agents truly transact at machine speed, payment volumes could climb sharply. Furthermore, new business models may emerge around metered, pay-per-use services.

Mastercard clearly wants to own that infrastructure layer. Its reach across 200-plus countries gives it a strong head start. For now, businesses and developers will watch closely. The next phase of digital commerce may run with no human in the loop at all.