April 27, 2026 – Ten companies absorbed the bulk of European fintech capital. The UK led decisively. Debt financing reshaped the entire stack, and the numbers tell a stark story.

European fintech hit a crossroads in 2025. Total funding fell 11% year-on-year to $16.3 billion. Deal volume shrank from 1,047 transactions in 2024 to just 743. Yet the money that did move flowed into larger, bolder bets. Average deal size jumped to $21.9 million, up from $17.5 million in 2024.

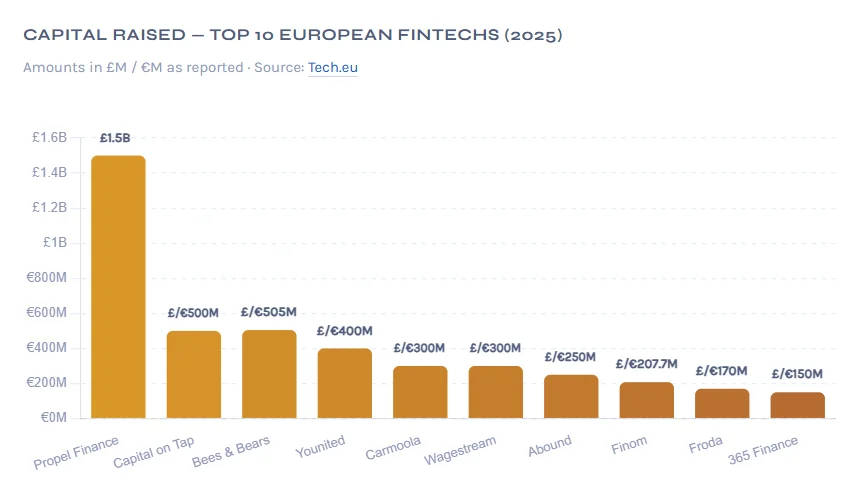

This is not a sector in retreat. It is a sector consolidating. Capital is concentrating on proven platforms with real revenue. The ten companies below captured a disproportionate share of Europe’s fintech funding.

The UK’s Commanding Lead

No country dominates European fintech like the United Kingdom. The UK captured 56% of total European fintech funding in 2025. London alone accounted for 79% of that national total. Germany and France trail at roughly €1.5 billion and €1 billion, respectively.

Seven of the ten largest raises came from UK-based firms. The UK benefits from deep institutional lending networks. Its mature regulatory framework and embedded finance infrastructure give it a structural edge.

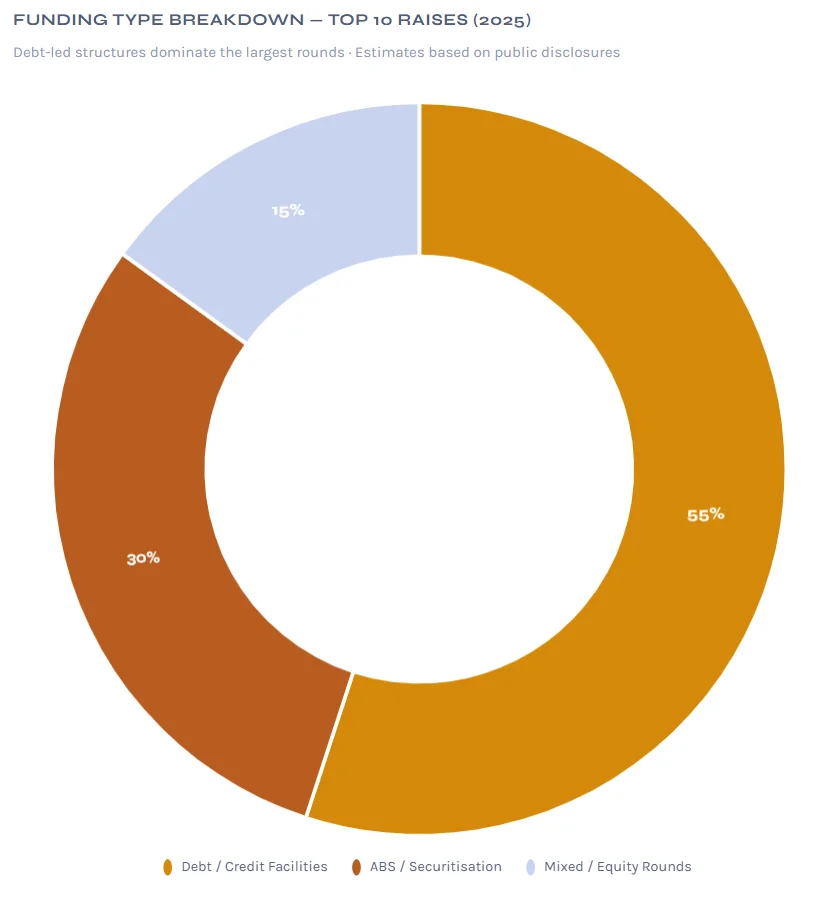

Debt Is Now the Dominant Force

Look at the top ten raises, and a pattern emerges fast. Most of these are not equity rounds. They are credit facilities, asset-backed securities, and warehouse financing structures.

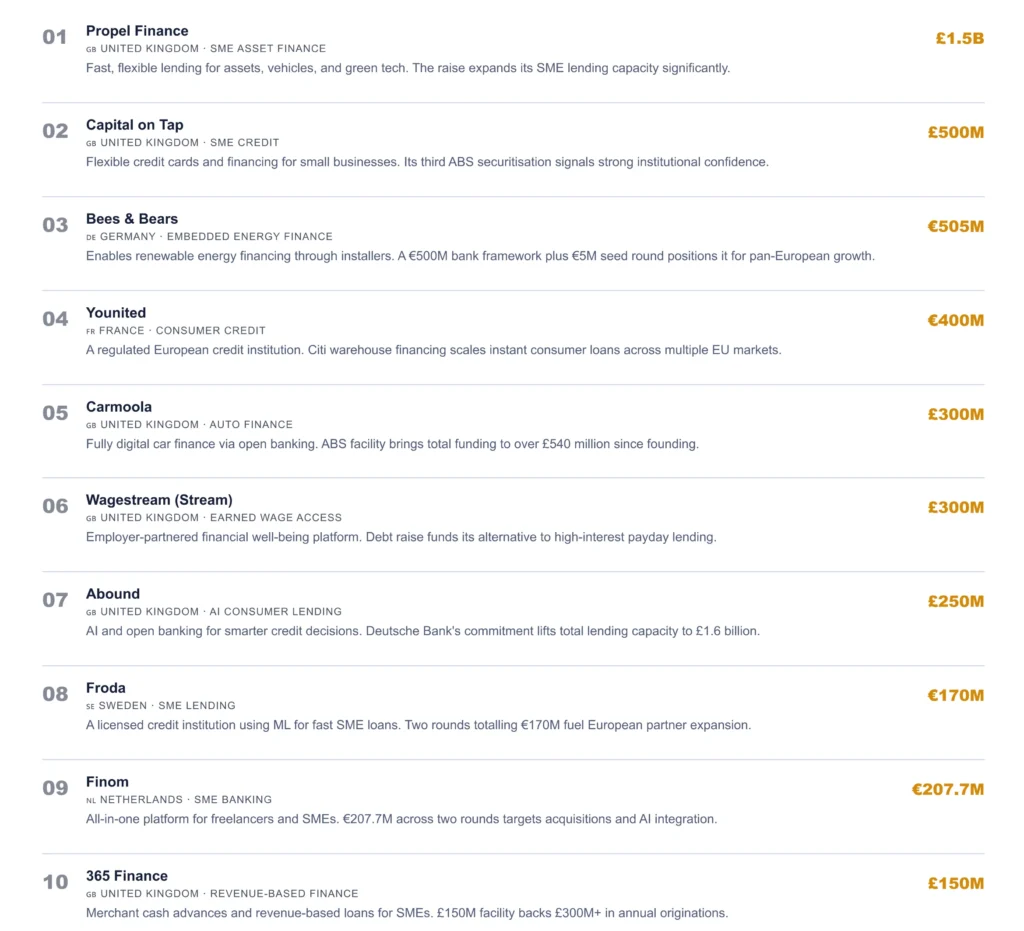

Propel Finance’s £1.5 billion raise expanded lending capacity. Capital on Tap’s £500 million was its third ABS securitisation. Carmoola secured a £300 million private ABS facility. Wagestream closed £300 million in debt financing. Younited’s €400 million came via Citi warehouse financing.

“Capital is concentrating on fewer, larger deals, and debt is leading everyone.”

— Analysis based on Fintech Global & Tech.eu data, 2026

This is a maturity signal. Fintech lending platforms no longer need to prove the model. They need fuel to scale it. Debt is cheaper and faster than equity at this stage.

The Ten Companies That Led the Pack

Each company operates in a distinct fintech vertical. Together, they span SME credit, consumer lending, vehicle finance, earned wage access, and embedded energy finance.