May 04, 2026 – A 31-million-pound supply shortfall is forcing producers worldwide to accelerate. New mines are switching on from Texas to Uzbekistan.

In Summary

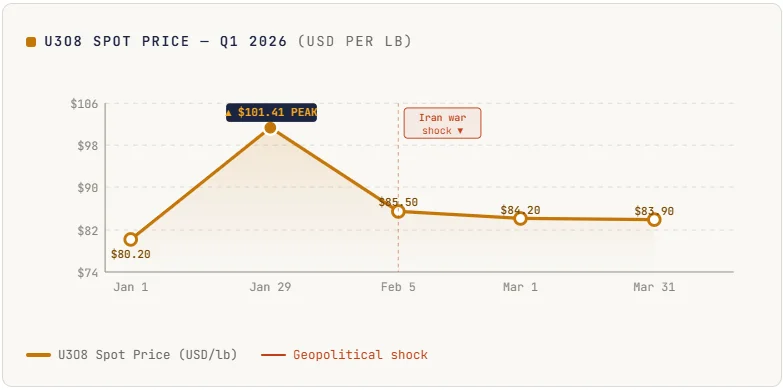

Spot U3O8 held above $80/lb since Jan 2026, peaking at $101.41 on Jan 29.

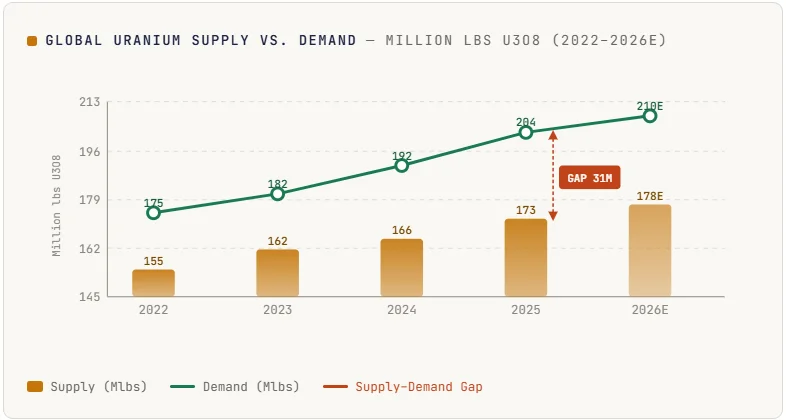

2025 production (~173 Mlbs) trailed demand (~204 Mlbs) by 31 Mlbs.

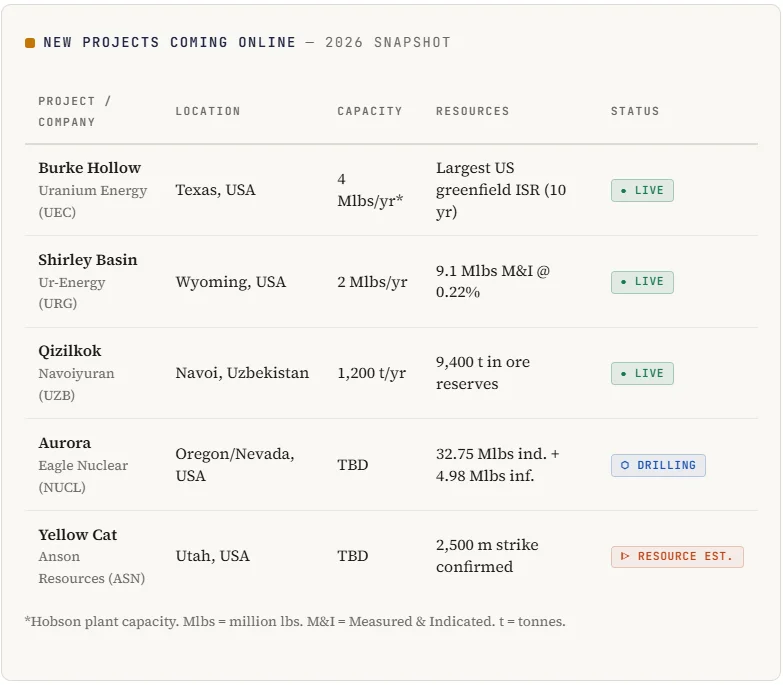

UEC’s Burke Hollow (Texas) is live, the largest US greenfield ISR in a decade.

Ur-Energy restarted Shirley Basin (Wyoming) with 9.1 Mlbs M&I reserves.

Uzbekistan’s Qizilkok adds 1,200 tonnes/year with a 15-year mine life.

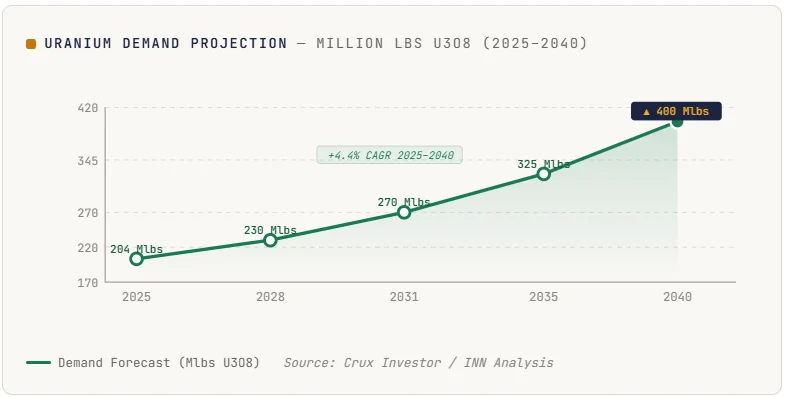

Global demand forecast: 400 Mlbs by 2040, double current levels.

The global uranium market is in deficit. In 2025, world production reached roughly 173 million pounds. Primary demand, however, stood at about 204 million pounds. That 31 million-pound gap is structural, not cyclical.

Producers are responding. New mines are coming online. Projects long dormant are restarting. The industry is moving faster than it has in two decades. This report breaks down what is happening, where it is happening, and what it means for the market.

Prices Are the Catalyst

The spot U3O8 price started in 2026 just above $80 per pound. It surged to $101.41 on January 29. That marked a year-to-date high. Geopolitical shocks pulled prices back. By the end of Q1, spot sat at $83.90.

The floor has held. Prices above $80 make many deposits economical. Producers that sat idle for years are now acting. The market’s signal is clear: supply is needed, and the price supports it.

The U.S. DOE committed $2.7 billion over the next decade to expand domestic uranium enrichment. Government backing is removing another barrier for producers.

US Projects Go Live

Burke Hollow, Texas, Uranium Energy Corp

Uranium Energy Corp (UEC) received final approval from the state of Texas to produce at Burke Hollow. The site covers 20,000 acres. It is the largest greenfield ISR discovery in the US over the past ten years.

The project runs as a hub-and-spoke model. Recovered uranium feeds UEC’s Hobson processing plant. That plant holds a licensed capacity of 4 million pounds per year. A second ISR project, Ludeman, is planned to start in 2027.

“With two ISR operations now producing, we are building a scalable, multi-faceted platform supported by the largest uranium resource base in the United States.”

— Amir Adnani, President & CEO, Uranium Energy Corp

Shirley Basin, Wyoming, Ur-Energy

Ur-Energy launched mining operations at Shirley Basin. Wyoming is historically the birthplace of commercial ISR mining. The project holds a licensed wellfield capacity of up to 2 million pounds per year. Its mine life spans nine years across three shallow units.

Measured and indicated resources total 9.1 million pounds at an average grade of 0.22%. Uranium on resin at Shirley Basin will travel to Ur-Energy’s Lost Creek facility for final processing this summer.

Central Asia Expands Output

The US push matters. But Central Asia still dominates global supply. Kazakhstan alone accounts for roughly 40% of world output. Uzbekistan is now adding momentum too.

On April 23, Uzbekistan’s state-owned Navoiyuran announced commercial ISR recovery at the Qizilkok deposit. Uzbekistan is the world’s fifth-largest uranium producer. Qizilkok is Navoiyuran’s third-largest deposit, holding 9,400 tonnes in ore reserves.

The site uses low-reagent oxygen ISR technology. The company says this cuts production costs by two to three times. The projected mine life is 15 years. Annual capacity stands at 1,200 tonnes.

The Exploration Pipeline Is Growing

Eagle Nuclear Energy is running a 27,000-foot, 47-hole drill program at Aurora on the Oregon-Nevada border. The program begins in July. It targets a prefeasibility study by H2 2027.

Aurora hosts 32.75 million pounds of indicated resources. That makes it the largest conventional uranium deposit in the US. Eagle plans to pair it with small modular reactor technology.

In Utah, Anson Resources confirmed uranium and vanadium mineralisation at Yellow Cat. The strike extends 2,500 meters. The company is tightening its drill spacing to accelerate a formal resource estimate.

What the Deficit Means Long-Term

Global uranium demand is projected to reach 400 million pounds by 2040. That is more than double the current consumption. Primary mine production runs 25–30% below theoretical capacity. The shortfall is expected to intensify through the 2030s.

Current global production ranges from 140 to 173 million pounds annually. Reactor fuel demand is climbing toward 200 million pounds and beyond. Mine development timelines run five to seven years. Reactor builds take eight to twelve years. The timing gap suggests markets will remain tight well into the 2030s.

The AI data centre boom adds another layer of demand. Hyperscale computing requires reliable baseload power. Nuclear is one of the few scalable solutions. More than 63% of investors in a recent survey believe AI demand will become a material factor in nuclear planning within a decade.

The verdict is straightforward. Supply is responding. But demand is growing faster. The projects going live today are necessary, not surplus. Every pound produced closes a gap that would otherwise widen. Investors, utilities, and policymakers are all watching the same clock.