April 21, 2026 – DeFi Is Finally Entering Its Capital Markets Era, and the $12 billion sitting idle proves it. The TVL obsession is the problem. Capital discipline is what comes next.

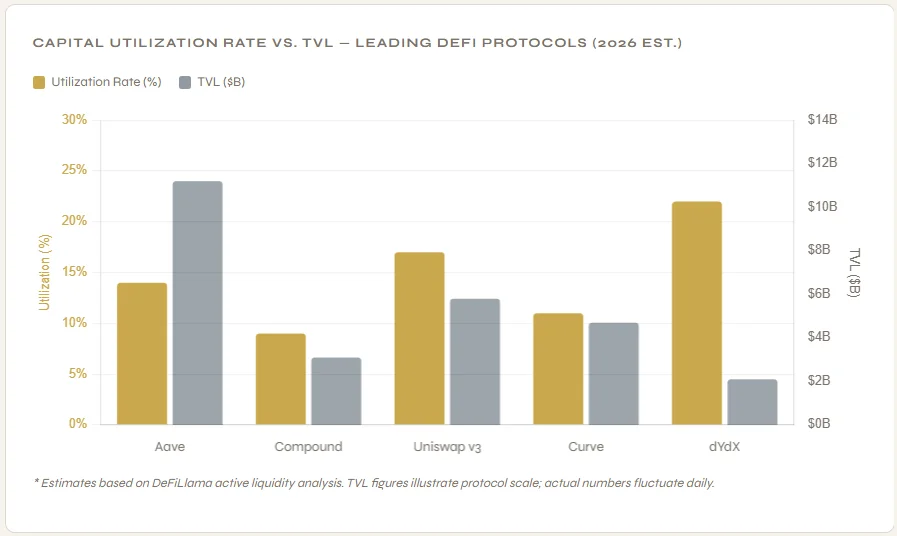

Decentralised finance has a utilisation crisis. CoinDesk reports that over $12 billion in DeFi capital remains unused at any given time. In fact, up to 95% of money deposited into trading pools never executes a single trade. Meanwhile, lending platforms operate well below capacity. DeFi can attract capital, yet it still struggles to put it to work.

This is not a temporary glitch. Rather, it is a design flaw baked into how DeFi has been built, funded, and measured over the past five years. In 2026, that flaw is consequently becoming impossible to ignore.

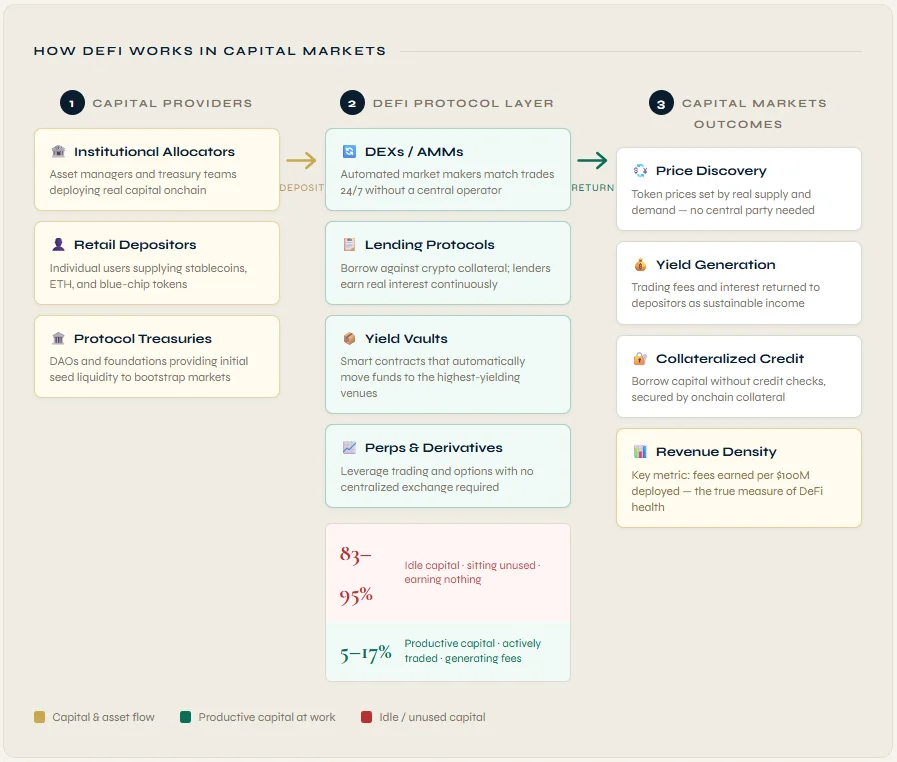

What Is the TVL Trap?

TVL stands for Total Value Locked. Think of it like a bank reporting how many deposits it holds. That sounds reassuring. However, it says nothing about whether those deposits are actually being used productively.

A bank with $2 billion in deposits but only $80 million in active loans is not healthy. Instead, it is a storage facility. DeFi built the same problem. DeFiLlama data show that leading protocols have utilisation rates of just 5%–17%. Protocols competed for deposits using token rewards. As a result, users came for the rewards, not the product. When rewards slowed, capital consequently fled.

“A protocol with $2B in TVL but only $80M in active capital is not a market. It is a parking lot.”

— Capital markets logic applied to DeFi

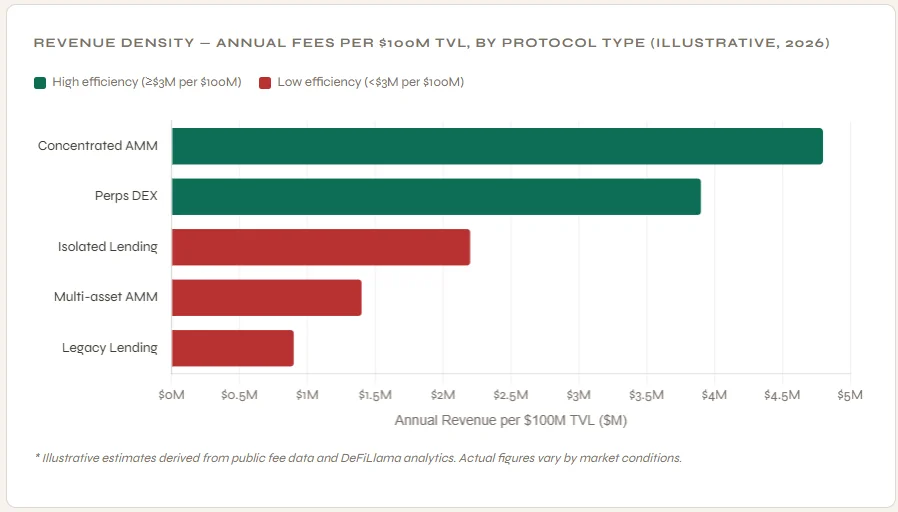

Revenue Density: A Simpler, Better Metric

Here is a simple analogy. Imagine two restaurants. The first has 200 seats but is always half empty. In contrast, the second has just 50 seats and is always full. Consequently, the smaller venue makes more money per table and per square meter. That is revenue density.

In DeFi terms, revenue density asks: how much in fees does a protocol earn for every $100 million it holds? Uniswap v3’s concentrated liquidity model proved this works at scale. By letting providers focus funds in active price ranges, v3 earned far more per dollar than its predecessor. Therefore, the lesson is clear: concentration beats breadth when efficiency is the goal.

The gap is indeed striking. A concentrated AMM earns more than five times as much per dollar as a legacy lending protocol. As a result, when institutional capital enters DeFi, it will target revenue density, not raw TVL.

Why Institutions Are Paying Attention

Institutional investors do not measure in TVL. Instead, they evaluate return on capital, yield sustainability, and risk-adjusted efficiency. Consequently, a protocol earning $10 million from $200 million in active funds is far more attractive than one earning $3 million from $2 billion in idle funds.

Moreover, research from the Bank for International Settlements has flagged idle DeFi liquidity as a systemic risk, not just an efficiency problem. Large idle pools attract mercenary capital that leaves at the first sign of trouble. As a result, that fragility ultimately undermines the entire ecosystem.

Furthermore, regulatory frameworks like the GENIUS Act are making efficient capital deployment a governance expectation. Auditable, productive use of funds is therefore no longer optional for serious on-chain participants.

Four Ways to Build Capital Discipline

First, concentrate liquidity. Fewer, deeper pools consistently outperform dozens of thin ones. As a result, concentration produces tighter spreads, higher fees, and better lending rates for everyone involved.

Second, put bridged assets to work. Billions locked in Layer 2 bridge contracts sit completely idle today. However, a smarter architecture deploys those same assets into lending markets, so one dollar therefore performs two jobs at once.

Third, recycle protocol revenue. When a protocol earns fees, it can extract that value or reinvest it. Reinvesting consequently builds deeper liquidity and steadier yields over time, the on-chain equivalent of a market maker reinvesting into tighter quotes.

Finally, measure productive TVL, not total TVL. Track fees earned per dollar deployed. That single shift changes what protocols build toward and, in turn, what users reward with their capital.

The Road Ahead

DeFi’s first chapter proved that decentralised finance is technically possible. AMMs, lending protocols, and on-chain derivatives were, indeed, genuine breakthroughs. However, the second chapter must prove that DeFi is economically disciplined, not just technically impressive.

Protocols that build around capital efficiency will therefore attract serious allocators and sustainable yields. Those that instead chase TVL growth through token incentives will accumulate large numbers and ultimately find no credible institutional partners willing to deploy alongside them.

DeFi is not dying. Rather, it is finally growing up. And, as with every maturing financial market before it, the path forward runs through capital discipline.