What 2026 Signals for the Future of Cross-Border Finance

April 23, 2026 – Stablecoin rails are no longer parallel infrastructure. They are the primary infrastructure. The data makes that undeniable, and the regulatory window has finally opened.

Cross-border payments are entering their most consequential year since 1977. That is when SWIFT first went live. Now, nearly five decades later, blockchain stablecoin rails are challenging the very architecture that SWIFT built.

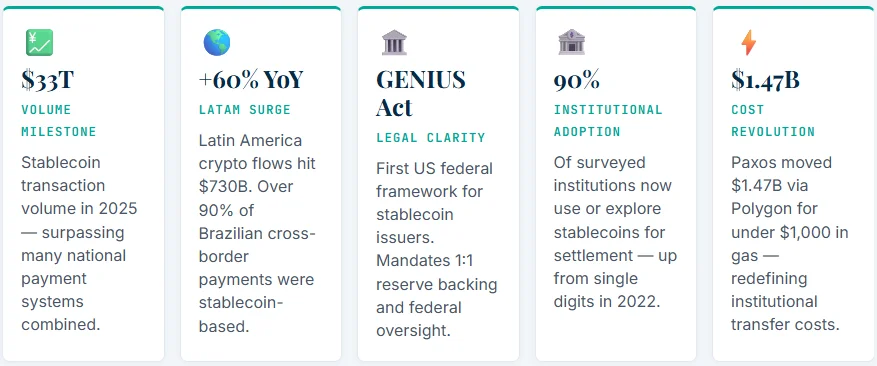

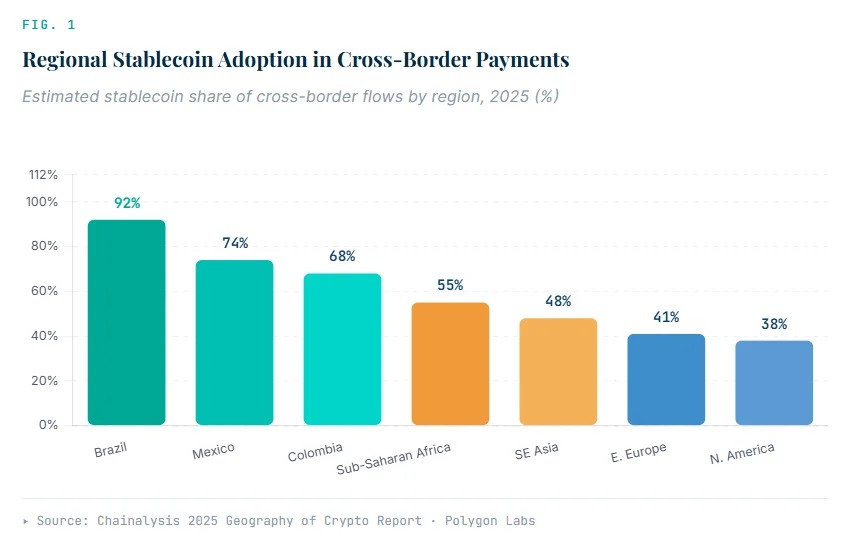

The numbers from 2025 leave little room for debate. According to Chainalysis, Latin America alone received over $730 billion in crypto transaction volume, a 60% year-over-year surge. More than 90% of Brazilian flows were stablecoin-related.

Globally, stablecoin transaction volume reached $33 trillion in 2025. That figure, cited by Polygon Labs in their April 2026 analysis, dwarfs many national payment systems combined.

“The question is no longer about infrastructure. It is about operations: who moves the money, on what rails, and at what cost.”

— Polygon Labs, April 2026

The Data Is Decisive

Individual company metrics reinforce the macro trend. Bitso Business hit $82 billion in annualised total payment volume. It now handles an estimated 10% of all US-Mexico remittances.

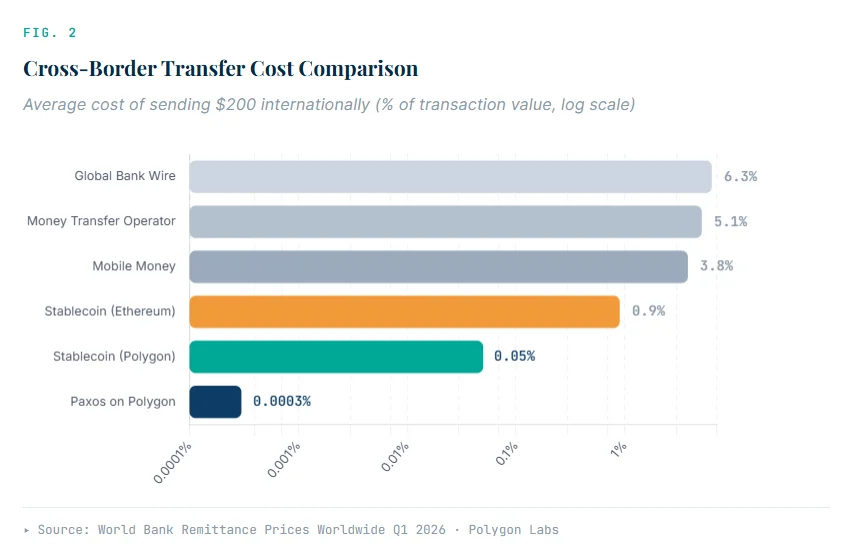

That is not a rounding error. The World Bank estimates the average cost of sending $200 across borders remains above 6%. Blockchain-based alternatives undercut that figure by an order of magnitude.

BlindPay, backed by Y Combinator, crossed $580 million in transaction volume on Polygon. It connects directly to Pix, SPEI, and PSE, the national payment rails of Brazil, Mexico, and Colombia. Minteo’s COPM crossed $200 million in monthly transfer volume.

How the Infrastructure Works

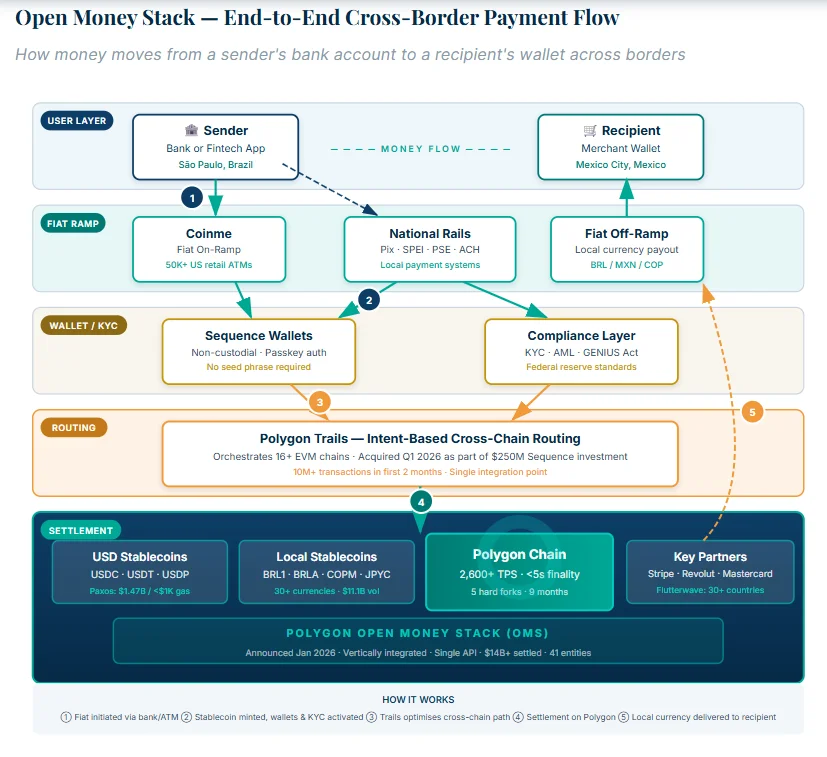

The Open Money Stack (OMS) is Polygon’s vertically integrated answer to fragmented payment infrastructure. It connects every layer, from fiat cash to blockchain settlement, in a single unified framework. The diagram below shows the complete end-to-end payment flow.

Cost Parity Is Now the Baseline

Sub-cent settlement is now possible on multiple chains. Cost alone no longer differentiates competitors.

The new frontier is liquidity depth, settlement speed, and full-stack integration. Moving money from São Paulo to Mexico City, with neither party thinking about blockchain, is now the real competitive advantage.

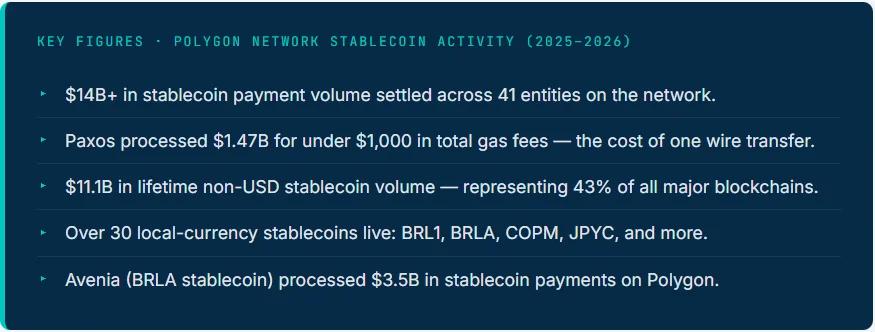

Polygon’s network processes 2,600+ transactions per second with sub-five-second finality. Five hard forks shipped in nine months achieved that. Paxos proved it: $1.47 billion moved for what a single wire transfer costs at most banks.

Regulation Has Finally Arrived

Infrastructure readiness alone was never sufficient. Institutions needed regulatory clarity. That clarity is now materialising at speed.

The GENIUS Act provided a federal legal framework for stablecoins in the United States for the first time. It mandates 1:1 reserve backing and federal oversight for payment stablecoin issuers. Brazil’s central bank classifies stablecoin transfers as foreign exchange operations. Paxos holds a conditional OCC national trust charter.

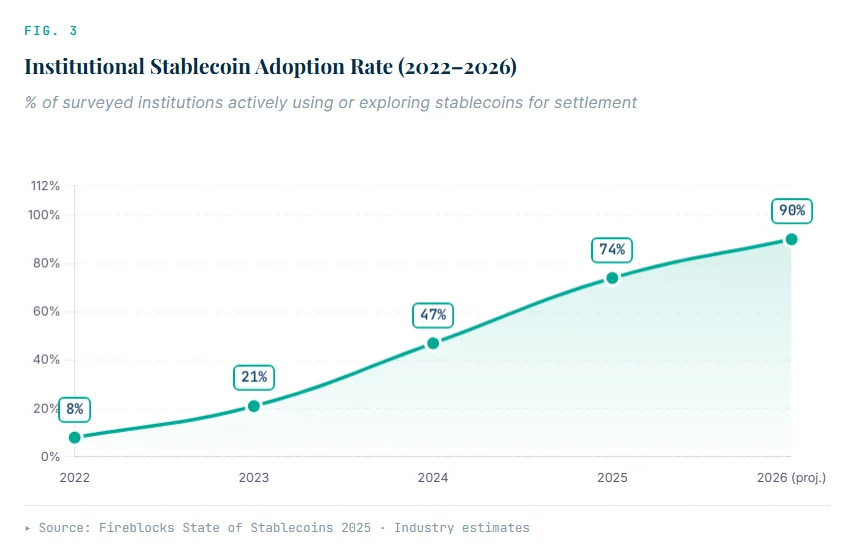

A Fireblocks survey found that 90% of institutional players now use or actively explore stablecoins for settlement. That figure was in single digits just three years ago.

Three Signals That Define What Comes Next

Signal 1: Liquidity over cost. Polygon holds over 43% of all non-USD stablecoin transfers across major blockchains. Institutions entering Latin America, Africa, or Southeast Asia face one question. It is not which chain is cheapest. It is where the liquidity already sits.

Signal 2: Corridors merging into unified infrastructure. Stripe, Revolut, Flutterwave, and Mastercard have each chosen Polygon as core settlement infrastructure. Flutterwave covers 30+ African countries. Revolut has processed over $800 million through Polygon. Fragmentation, the core reason cross-border payments have been expensive, is being solved at the network layer.

Signal 3: The institutional-grade bar has been met. The era of experimentation is over. Compliance frameworks exist. Reserve requirements exist. National bank charters are being issued. Stablecoin payments in 2026 are as regulated as many traditional payment systems.

The Bottom Line

Choosing settlement infrastructure in 2026 is a strategic decision, not a technical one. The regulatory clarity exists. The throughput exists. The institutional partnerships exist.

For banks, Bitso handling 10% of US-Mexico remittances is a competitive signal. Correspondent banking is being disintermediated corridor by corridor. The tools to respond are already live.

For corporates, the Paxos data frames the stakes clearly. Treasury teams that understand stablecoin settlement today gain a structural cost advantage over those learning it in 2027.

For fintechs, the corridor you want to win likely already has a local-currency stablecoin on Polygon. Building on that liquidity rather than assembling five vendors is the new competitive baseline.

The infrastructure decision, ultimately, is a market position decision. And 2026 is the year that the window starts to close.