April 14, 2026 – The Pentagon just handed Anduril a $20B counter-drone contract. The broader market is racing toward $14–16B by 2030. Here’s why the opportunity is hiding in plain sight.

In Summary

The Pentagon awarded Anduril a $20B, 10-year counter-UAS contract vehicle in early 2026.

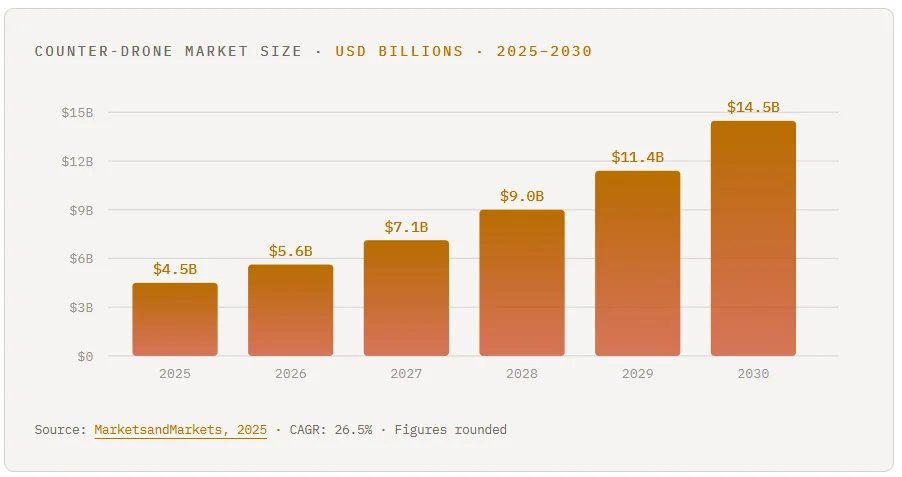

The global counter-drone market is projected to reach $14.5B by 2030, growing at a 26.5% CAGR.

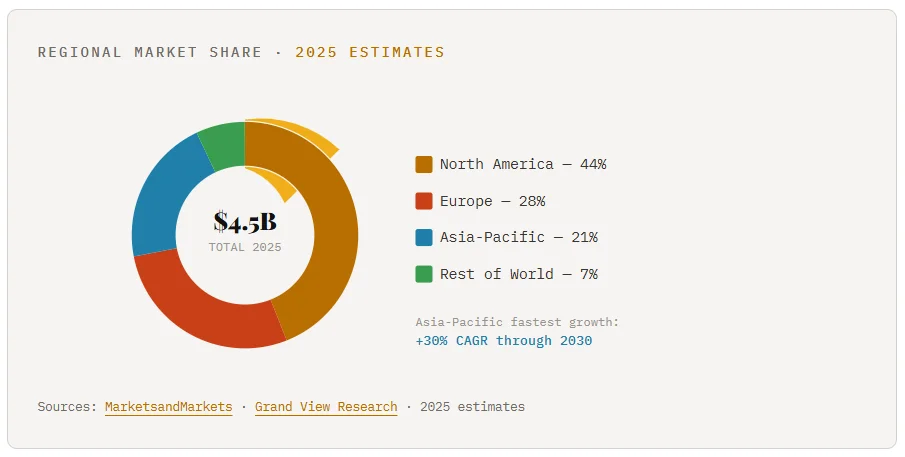

North America holds 44% of the market; Asia-Pacific is the fastest-growing region at 30% CAGR.

Directed energy and AI-powered detection are the two fastest-growing technology segments.

Private players like Epirus have raised over $550M, and institutional capital is already moving in.

Aseismic contract just landed in defense procurement. Specifically, the U.S. Army’s Joint Interagency Task Force 401 awarded Anduril a firm-fixed-price contract vehicle worth up to $20 billion over ten years. It consolidates hardware, software, and AI into a single counter-UAS capability. Yet most retail investors have barely noticed.

This isn’t an isolated deal. Rather, it is the loudest signal yet in a rapidly expanding market. Indeed, the global counter-drone sector now sits on a steep growth trajectory. Battlefield proliferation, critical infrastructure threats, and surging defense budgets worldwide actively drive this demand.

A Market Growing Faster Than Most Defense Sectors

Numbers from multiple research firms tell a consistent story. For instance, MarketsandMarkets projects the global counter-UAS market to grow from $4.48 billion in 2025 to $14.51 billion by 2030, at a compound annual growth rate (CAGR) of 26.5%. Similarly, Mordor Intelligence places the 2025 figure at $3.03 billion, climbing to $9.3 billion by 2030 at a 25.14% CAGR. Even at the conservative end, growth remains exceptional.

Moreover, Precedence Research extends the timeline further, forecasting the market to reach $30.91 billion by 2035, growing at a 26.4% CAGR. As a result, few defense segments outside hypersonics match this pace.

Why Demand Is Structural, Not Cyclical

Crucially, this is not a trend tied to a single conflict or budget cycle. Instead, three structural forces permanently expand the addressable market.

First, drone proliferation has outpaced defenses. Notably, Fortune Business Insights estimates that the commercial drone market reached $32 billion in 2024 and is heading toward $189 billion by 2033. As a result, every new drone creates a potential threat vector. Consequently, every threat vector demands a countermeasure.

Second, modern warfare has exposed the asymmetric cost problem. Low-cost drones, some costing under $500, destroy assets worth millions. Therefore, militaries need economical, scalable responses. That demand, moreover, is permanent.

Third, civilian infrastructure now ranks as a primary target. Airports, power grids, and government buildings face rising drone incursions. As a result, this threat opens a massive commercial segment alongside the defense market.

“The initial task order is $87 million. The bigger story is the vehicle itself: a firm-fixed-price contract worth up to $20 billion over 10 years.”

— REX Shares Defense Market Brief, March 2026

Four Technologies Driving the Market

Where Smart Money Is Moving

North America commands 44% of the current market. However, the fastest growth lies elsewhere. Specifically, the Asia-Pacific region is forecasted to grow at a 30% CAGR through 2030. Similarly, Europe follows close behind at 27.5%, fuelled by NATO rearmament.

Key publicly traded names include DroneShield (ASX: DRO), AeroVironment (AVAV), and RTX’s Raytheon division. Furthermore, private players like Anduril and Epirus raise capital at scale. Notably, Epirus alone has raised over $550 million, including a $250 million Series D in 2025.

The Anduril contract is the clearest signal yet. Importantly, it is not $20 billion in hand; it is a contract vehicle. As the Army deploys the Lattice AI platform, task orders will continue to grow. Ultimately, that represents a decade of recurring defense revenue.

The counter-drone trade is no longer a niche bet. Instead, it is a structural defense theme that real contracts and government mandates back. Nevertheless, most investors still watch from the sidelines. That window, however, may be closing fast.