April 04, 2026 – With £1.24 billion in UK revenue, an ECB banking licence, and profits up eightfold, Monzo chose Europe over America. The data makes a compelling case.

In Summary

~50 layoffs from US operations

US accounts close June 2026

ECB licence granted Dec 17, 2025

£16.6B in UK deposits (+48% YoY)

New CEO: Diana Layfield (ex-Google, StanChart)

First application failed: Oct 2021

Monzo is leaving the United States. The UK’s largest app-based digital bank announced its withdrawal on March 31, 2026, citing a deliberate focus on home-market growth. The decision ends a six-year American experiment. It also reveals where Monzo’s real opportunity lies.

New CEO Diana Layfield signed off on the move. Around 50 US employees will be laid off. Existing US customer accounts will remain active until June 2026.

The Numbers Behind the Pivot

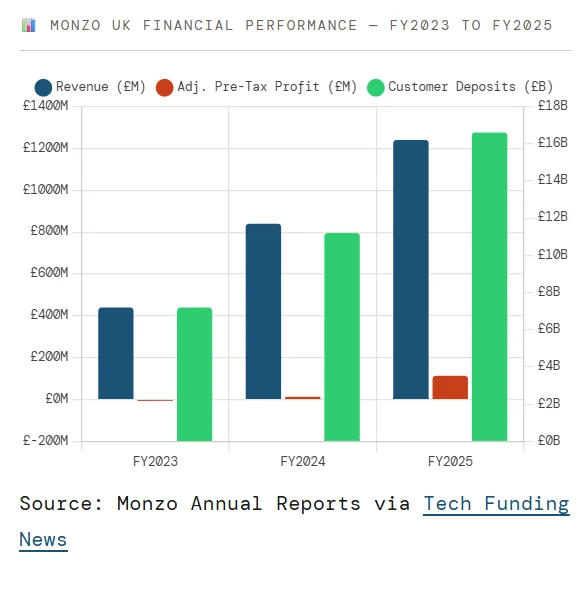

Monzo’s UK results make the decision look obvious in hindsight. Revenue hit £1.24 billion for the year ending March 2025, a 48% increase year-on-year. Adjusted pre-tax profit surged to £113.9 million. That is an eightfold jump.

Customer growth was equally strong. Monzo added roughly 2.4 million accounts. That is a 25% rise in a single year. UK deposits climbed 48% to £16.6 billion. These figures build a strong lending base. They make US investment extremely hard to justify.

Why the US Never Worked

Monzo first entered the US in 2019. It launched a banking charter application in April 2020. But regulators indicated the bid would fail. Monzo withdrew the application in late 2021 after 17 months.

Without a charter, Monzo relied on partner banks. First, it used Sutton Bank. Then Lead Bank. This dependency blocked core revenue streams like direct lending and interchange. Monzo remained an app in the US. It never functioned as a full bank.

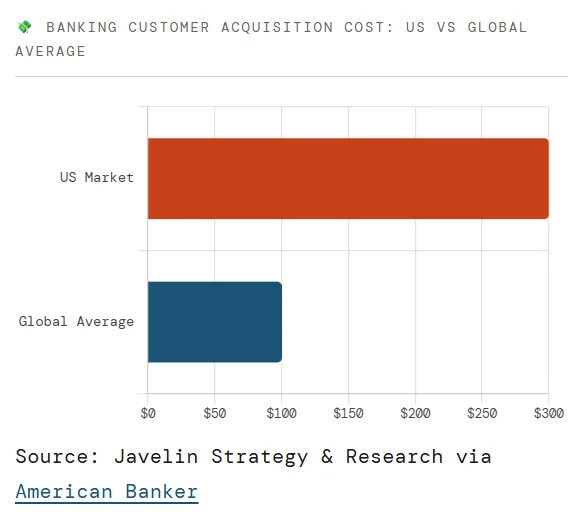

The structural problem ran deeper than licensing. US customer acquisition costs average $300 per customer. That is three times the global average of $100. Analyst Emmett Higdon of Javelin Strategy called it plainly: “A one-size-fits-all global digital banking play will never prosper in the US.”

“With a fast-growing customer base of 15 million in the UK and the growth opportunity our European banking licence creates, we’re making a deliberate, strategic decision to focus on scaling in our home market and Europe.”— Monzo Spokesperson, March 2026

The European Licence Changes Everything

On December 17, 2025, the European Central Bank granted Monzo a full banking licence. Monzo became the first digital bank fully regulated by the Central Bank of Ireland. Dublin serves as its European headquarters. The licence covers all EU member states via passporting rights.

This single regulatory asset unlocked a market of 450 million people. Monzo can now offer full banking services across the EU. It requires no separate national licence for each country. The contrast with the US is stark. America required a separate OCC charter, state-by-state compliance, and dedicated capital.

The timing of the US exit, just 12 weeks after the ECB approval, is not coincidental. Monzo chose to concentrate capital where its regulatory standing is strongest and most recently acquired. Ireland is its first launch market. Personal, business, and savings accounts will roll out to Irish customers first.

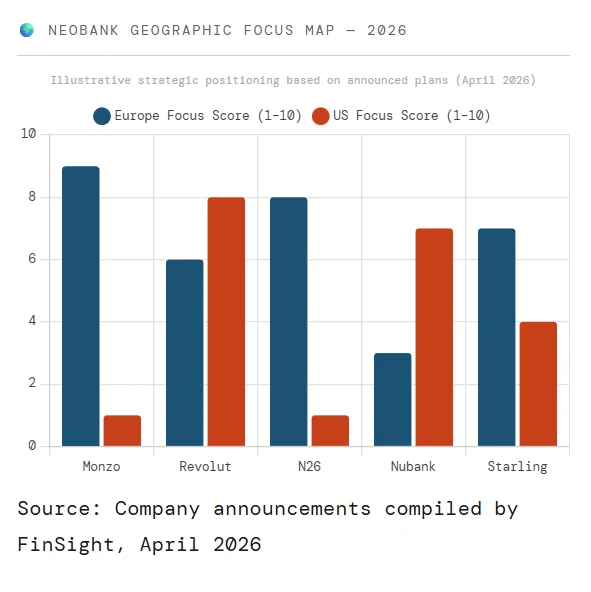

Rivals Move in Opposite Directions

While Monzo retreats, competitors are advancing into the US. Revolut applied for a US national bank charter last month. It plans to invest $500 million in North American growth. It already has over one million US customers.

Germany’s N26 exited the US in 2021. That closure came under regulatory pressure. Monzo’s exit follows a different logic, a strategic choice, not a constraint. The pattern shows that the US market quickly separates well-capitalised entrants from aspirational ones.

Nubank is also entering the US from a position of profitability. The Brazilian fintech reported $783 million in quarterly net income and serves 127 million customers. Its OCC-approved US subsidiary targets a 2027 launch.

What This Means for Monzo’s IPO

Monzo is widely expected to go public in 2026. The US exit cleans up the narrative. Loss-making international operations are hard to explain to public market investors. A profitable UK core and a clear EU expansion path are far easier to price.

Former CEO TS Anil was reportedly removed, in part, over disagreements about IPO timing. Diana Layfield, previously at Google and Standard Chartered, is signalling discipline. The US closure is the first proof point. The UK and Europe are where Monzo is betting its future.