April 09, 2026 – Minutes from the March FOMC meeting confirm the Fed still leans toward easing. But surging oil prices, sticky inflation, and a fragile growth outlook are all raising the bar.

In Summary

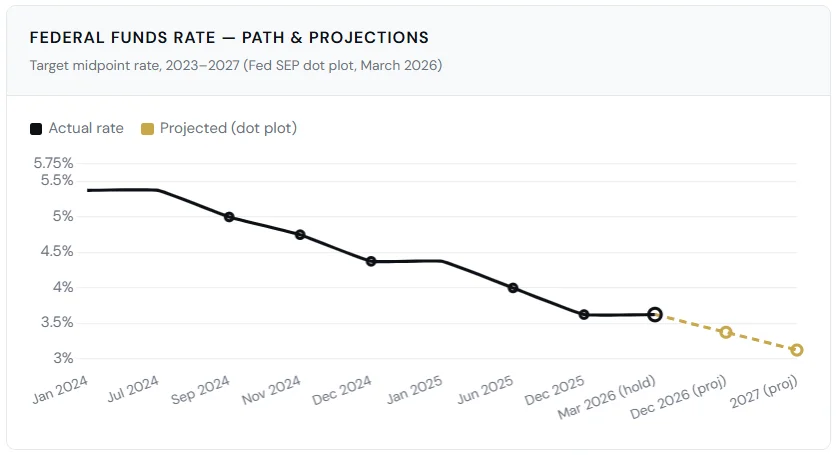

Fed held rates at 3.5%–3.75%, the FOMC voted 11–1 to hold steady.

The dot plot still projects one rate cut in 2026, unchanged since December.

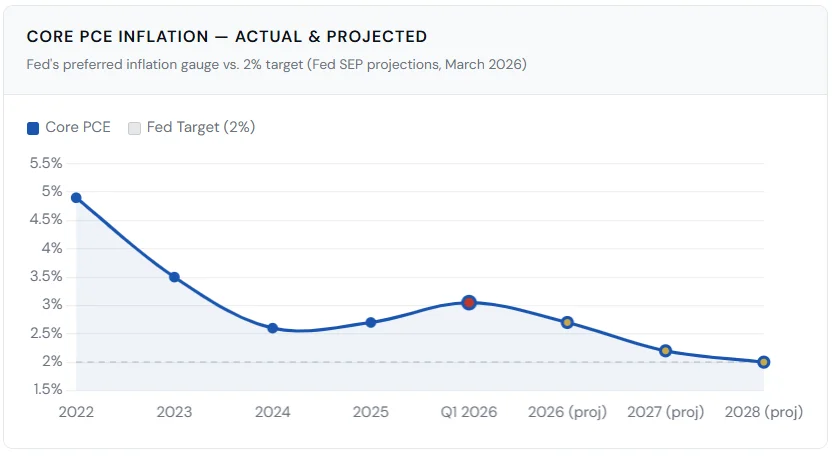

Core PCE inflation is running at 3.0%–3.1%, above the 2% target.

Prediction markets now price a 29.2% chance of zero cuts this year.

A rate hike carries a 14% probability, up sharply before the Iran ceasefire.

The Federal Reserve still wants to cut interest rates. But it wants lower inflation more. Minutes from the March 17–18 Federal Open Market Committee (FOMC) meeting, released Wednesday, make that tension plain. Many participants agreed rate cuts remain “likely appropriate”, if inflation falls as expected. That two-letter word, “if,” is carrying enormous weight right now.

The Current Stance

The FOMC voted 11–1 to hold the federal funds rate at 3.5%–3.75%. Governor Stephen Miran cast the lone dissent. He argued current policy remains too tight. It is dampening employment without clear benefit to inflation. The Fed has held rates at this level since December 2025.

Before the Iran war began, markets had priced in two rate cuts this year. That outlook has collapsed. Prediction markets now show a 29.2% chance of zero cuts in 2026. A rate hike, once dismissed as a tail risk, now carries a 14% probability.

Why the Fed Is Stuck

Inflation is the core problem. Core PCE ran at 3.0%–3.1% in January and February. That is a full percentage point above the Fed’s 2% target. It has been above target for five years. The Fed’s own projection for 2026 core PCE is 2.7%, still elevated.

Oil prices made the calculus worse. Front-month crude surged roughly 50% during the intermeeting period. The one-year inflation swap rate climbed nearly 50 basis points. These moves arrived before the March CPI data, meaning the full inflationary impact is still unknown.

“The balance of risks has shifted. The bar for cutting rates has risen meaningfully.”Luis Alvarado, Co-Head of Global Fixed Income Strategy, Wells Fargo Investment Institute

A Two-Sided Debate Inside the FOMC

The minutes expose a divided committee. Many members see cuts ahead. But some pressed for an explicit acknowledgment that hikes are also possible. They wanted the post-meeting statement to describe “two-sided” policy risk. That language did not make the final cut, but the debate itself signals unease.

Chair Powell has tried to calm markets. He noted that oil shocks are typically transitory. Long-term inflation expectations, he said, remain well anchored. The Fed’s job, he argued, is to wait for data, not react to headlines.

Key risk: Several FOMC participants raised the possibility of rate hikes if oil prices stay elevated and inflation remains persistently above target. This scenario was once off the table. It is now part of the Fed’s formal risk assessment.

The Growth Complication

Growth is softening, and that matters. GDP grew just 0.7% in Q4 2025. Early 2026 growth is tracking at 1.3%. The Fed still projects a solid 2.4% for the full year. But that optimism depends on the war’s impact being short-lived. Most FOMC participants said it is too early to know.

Schwab analysts note that seven FOMC members now see no cuts in 2026. That is one more than December. The median long-run rate ticked up to 3.125%. When that figure moves higher, it suggests current policy is less restrictive than assumed.

Unemployment is expected to reach 4.4% by year-end. That is unchanged from December. But a prolonged conflict could change that outlook quickly. Labor market weakness would add pressure for cuts, even as inflation remains stubborn.

What Comes Next

The next FOMC meeting is April 28–29. No action is expected. Polymarket shows a 98% probability of a hold. The March CPI report, released Friday, will be the first hard data capturing any post-war energy shock.

For investors, the Fed’s message is simple: patience. Rate cuts are possible. But they require falling inflation, stable energy prices, and clearer economic data. None of those conditions are confirmed yet.

The “wait-and-see” Fed is very much still in place.