April 06, 2026 – The bank argues rising energy prices will not derail the disinflation trend, but warns the timeline has shifted to the second half of the year.

In Summary

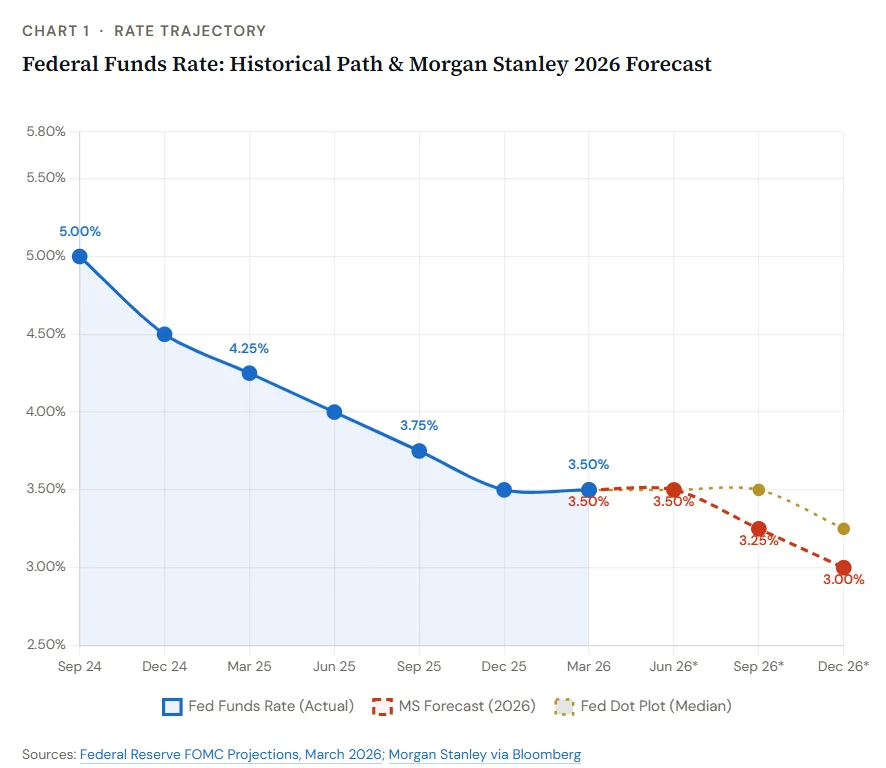

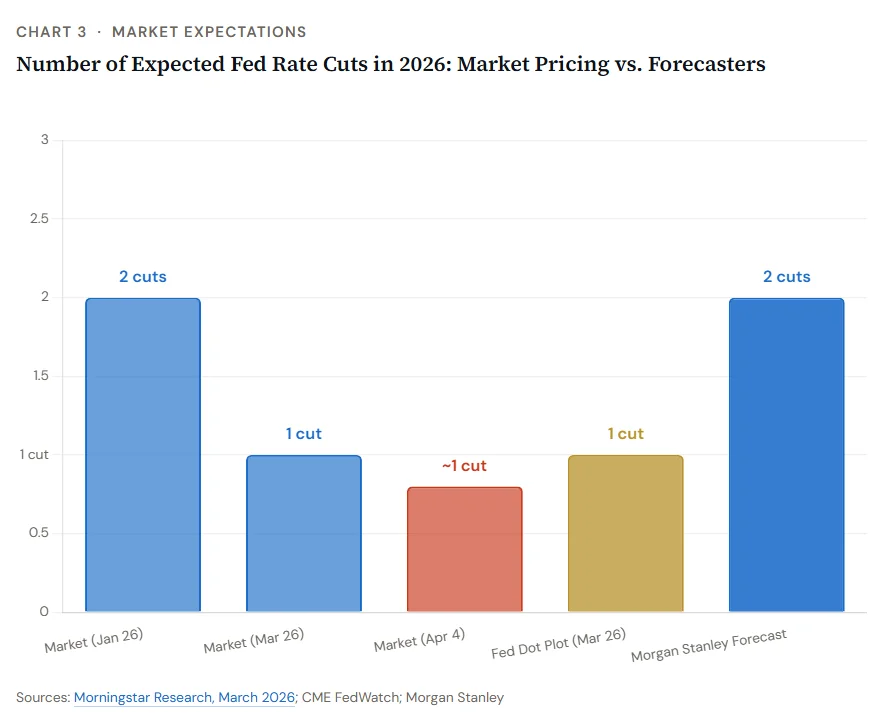

Morgan Stanley forecasts two 25-bp rate cuts in H2 2026, likely in September and December.

The Fed’s current policy rate stands at 3.50%–3.75%; MS targets 3.00%–3.25% by year-end.

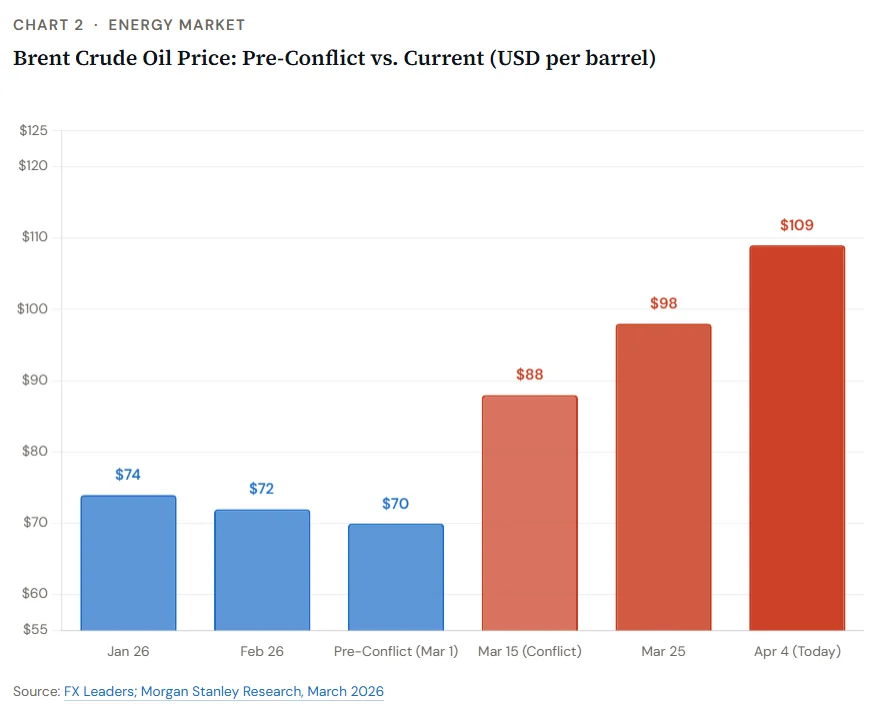

Brent crude surged from ~$70/bbl pre-conflict to over $109/bbl today, a 56% spike.

Financial conditions have already tightened by the equivalent of an 80-basis-point rate hike.

The Fed’s own March 2026 dot plot projects just one cut this year, MS sees two.

Key risk: if long-run inflation expectations de-anchor, the easing cycle could stall entirely.

The Federal Reserve is still likely to cut interest rates in 2026. That’s the view from Morgan Stanley, which argues the recent oil-driven inflation shock will not fundamentally alter the Fed’s easing path. Underlying price pressures remain contained, the bank says. The broader disinflation trend is still intact.

The Core Argument

Morgan Stanley’s base case hinges on one key distinction. Headline inflation is elevated, but core inflation is not. Core measures exclude volatile food and energy costs. The bank expects limited pass-through from oil prices into core components. That means the Fed can effectively “look through” the current energy spike.

According to the bank, the critical variable is not the headline CPI. It’s whether long-run inflation expectations stay anchored. Short-term expectations have risen, a direct reflection of higher fuel prices. But long-run gauges remain near pre-pandemic levels, suggesting the Fed’s credibility in controlling inflation is still intact.

Financial Conditions Already Tightened

Markets have already done some of the Fed’s work. Morgan Stanley estimates that higher oil prices, a stronger dollar, and rising equity risk premiums are equivalent to roughly an 80-basis-point rate hike. That is significant. It reduces the need for additional policy restraint from the central bank.

The Fed currently holds rates at 3.50%–3.75%. It has held rates steady for two straight meetings. Fed Chair Jerome Powell underscored the uncertainty surrounding the oil shock at his recent press conference. He noted the US had not made as much progress on inflation as hoped.

What Morgan Stanley Forecasts

The bank forecasts two 25-basis-point cuts in 2026. These are expected in the second half of the year, most likely in September and December. The projected target range would fall to 3.0%–3.25% by year-end.

This is a revised timeline. Morgan Stanley’s Chief U.S. Economist Michael Gapen shifted the expected cut dates from June and September to September and December. The reason: the Fed needs more confirmation that disinflation is resuming. The oil shock simply delays; it does not cancel the easing cycle.

“I think the answer is caution, and probably rate cuts come later than earlier. It will likely take the Fed longer to conclude that disinflation is occurring.” – Michael Gapen, Chief U.S. Economist, Morgan Stanley

What the Fed’s Own Data Shows

The Fed’s March 2026 dot plot shows a median projection of just one rate cut in 2026. That matches the December 2025 forecast unchanged despite geopolitical turmoil. Powell added an important caveat. The Fed cannot yet treat energy-driven inflation as “transitory”. It must also contain tariff-related price pressures. Both shocks are running simultaneously. That complicates the Fed’s communication strategy.

The Key Risk

Morgan Stanley’s base case depends on one condition: long-run inflation expectations must remain anchored. A sustained rise would force the Fed to hold rates higher for longer. Morningstar’s senior U.S. economist Preston Caldwell warns that the current oil shock is large enough to justify a firm Fed stance, even amid a softening labor market. If oil prices fail to retreat, second-round effects on wages and services become a real concern.

The Bottom Line

Morgan Stanley’s message is constructive but nuanced. The oil shock delays, but it does not deny Fed easing in 2026. Two rate cuts remain on the table for the second half of the year. Markets pricing in just one cut may be underestimating the Fed’s flexibility, provided inflation expectations hold steady. Watch the September FOMC meeting. That is likely to be the defining moment of the year for monetary policy.