US and EU regulators are softening post-2008 capital rules. A near-20% hike is now just 9%. The global framework is fracturing.

In Summary

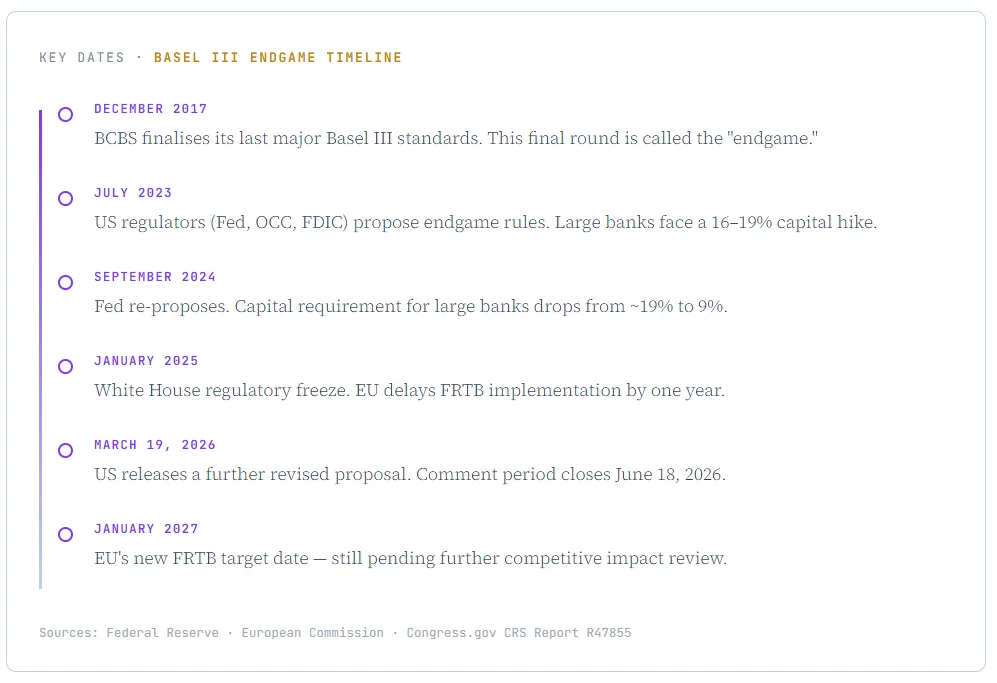

On March 19, 2026, US regulators revised Basel III. Capital requirements for large banks fall from ~19% to 9%.

The EU delayed the FRTB, the market-risk sub-framework, to at least January 2027.

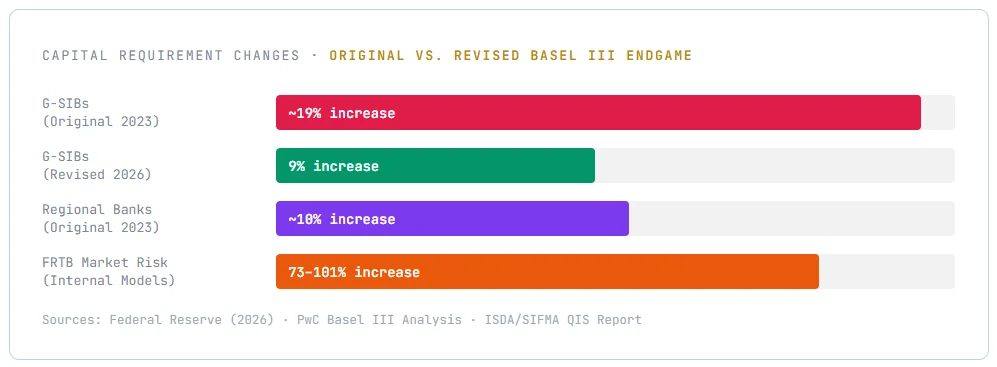

ISDA and SIFMA data show FRTB would raise market risk capital by 73–101%, depending on model choice.

US G-SIBs already hold ~$880B in CET1 capital, up from ~$214B before the 2008 crisis.

Diverging US, EU, and UK rules risk regulatory arbitrage. The decades-old global standard could fragment.

What Is Basel III?

Basel III is a global bank regulatory framework. It was created by the Basel Committee on Banking Supervision (BCBS) in 2010. Its aim: prevent a repeat of the 2008 Global Financial Crisis. It sets minimum standards for capital, liquidity, and leverage that banks must hold. The framework rests on three core pillars: minimum capital requirements, supervisory review, and market discipline.

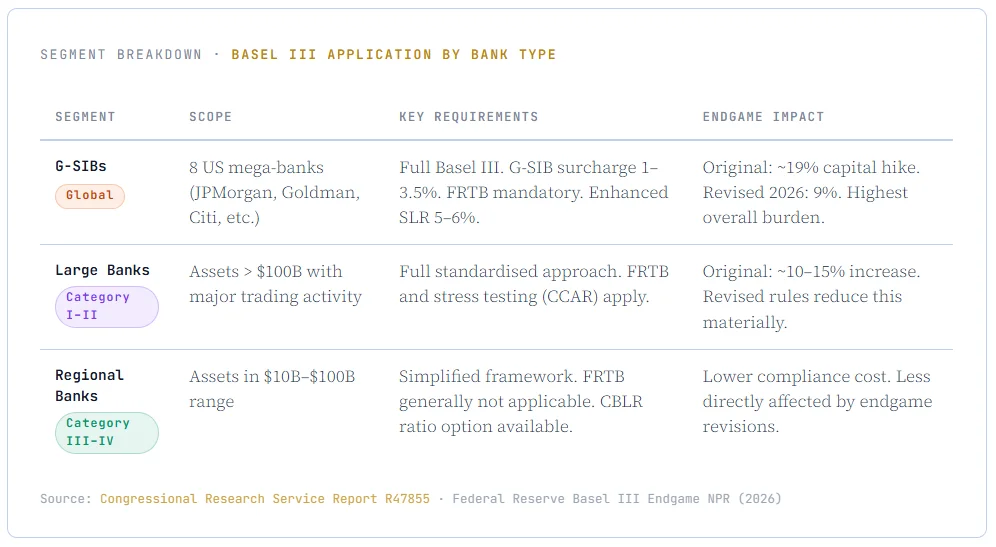

How Basel III Applies Across Segments

Basel III does not treat all banks equally. Requirements scale with a bank’s size, systemic importance, and trading complexity. Here is how the framework applies across the main segments.

The Endgame Unravels

Global banking regulation is at a crossroads. The Basel III “endgame”, nearly two decades in the making, is being rewritten. Both the US and EU are stepping back from strict capital demands. The reasons are competitive, political, and structural.

On March 19, 2026, the Federal Reserve, FDIC, and OCC released a revised Basel III endgame proposal. The original 2023 draft required the largest banks to raise capital by 16–19%. The new proposal slashes that to just 9%. That is a near-halving of the burden. Public comments close on June 18, 2026.

Meanwhile, the European Commission is reconsidering the FRTB. It has already been delayed to January 2027. Brussels is now exploring further measures. The goal: neutralise the competitive disadvantages that EU banks face relative to global rivals.

Why the Retreat?

The rollback did not happen overnight. Bank lobbying was fierce and effective. CEPR researchers note the 2023 proposal was effectively “killed in its original form.” By January 2025, a White House regulatory freeze had further extended the delay.

There is also a structural case. Since 2008, US banks have dramatically rebuilt their capital. ISDA and SIFMA data shows US G-SIBs raised CET1 capital from roughly $214 billion pre-crisis to around $880 billion by 2022. That is a 4x increase. Critics ask how much additional capital is truly necessary.

“At a time when global competition for capital is intense, maintaining a level playing field is critical to ensuring EU banks can lend and invest effectively.”

-Hyder Jumabhoy, Partner & Global Co-Head, Financial Institutions, White & Case

The FRTB Problem

At the heart of the debate sits the FRTB. It overhauls how banks measure risk in their trading books. It introduced stricter internal model tests and higher capital charges for complex positions. An ISDA/SIFMA quantitative study found FRTB would raise market risk capital by 73–101%. Europe’s banking industry called this “excessively conservative”, not aligned with actual economic risk.

The Bottom Line

Basel III’s endgame is being rewritten in real time. Capital requirements are falling. Timelines are slipping. Jurisdictions are diverging. The original promise of a unified global standard is under strain. If US, EU, and UK rules differ materially, banks could shift trading activity to lower-cost jurisdictions. The global framework built over decades of post-crisis cooperation could fracture permanently.

What is clear: the Basel III endgame is far from over.