April 03, 2026 – A new $100 million bond deal reveals exactly how traditional finance values BTC as collateral. The numbers are sobering, and the liquidation math is tight.

In Summary

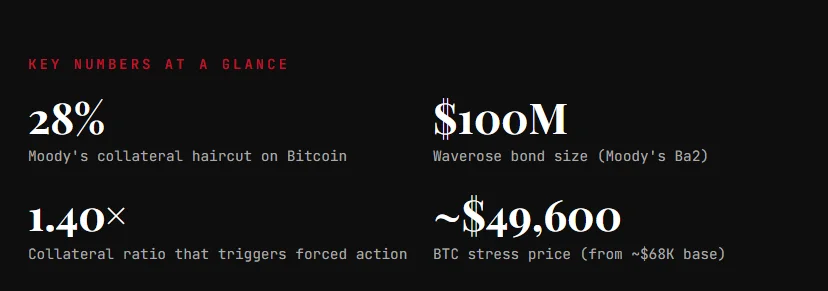

Moody’s valued Bitcoin at just 72 cents per dollar in the Waverose bond deal.

Forced selling triggers when BTC drops only 12.5% from the issuance price.

Three separate Bitcoin credit structures launched within six weeks in early 2026.

Moody’s stress price of ~$49,600 matches Standard Chartered’s stated bear-case target.

Cascading liquidations across multiple structures could amplify price drops in a downturn.

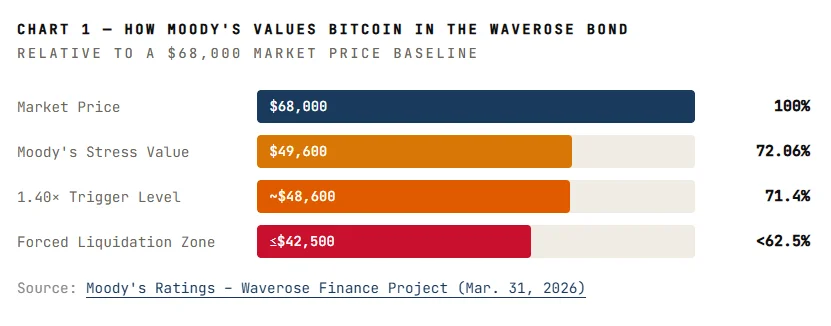

Bitcoin has spent years being called digital gold. Now, Wall Street has put a price on that gold, and it is worth less than you think. On March 31, Moody’s assigned a provisional Ba2 rating to up to $100 million in taxable revenue bonds for the Waverose Finance Project. The bonds are backed by Bitcoin held by NH CleanSpark Borrower Trust 2026-1. The twist: Moody’s only counts 72 cents of every Bitcoin dollar as real collateral.

That 28% haircut is not a punishment. It is the price of admission. It is what happens when a volatile asset enters a credit structure that demands predictability. And the deal sets a clear liquidation trigger. If Bitcoin falls just 12.5% from its issuance price, forced selling begins automatically.

The Opening Price of Trust

The Waverose structure is a taxable conduit revenue bond. New Hampshire acts only as a pass-through. Bondholders carry all the risk. This is limited-recourse, institutional plumbing, and those are exactly the conditions under which traditional finance agreed to work with Bitcoin at all.

At a 1.60× initial collateral ratio, debt equals about 62.5% of collateral value at launch. The structure triggers automatic action when the ratio falls to 1.40×, meaning debt is 71.4% of collateral. That gap between the two is just 8.9 percentage points. A 12.5% drop in Bitcoin’s price closes it completely.

“Moody’s stressed the collateral at 72.06% of market value. Mapped to Bitcoin’s April 1 price near $68,000, the stress zone lands at approximately $49,600, nearly identical to Standard Chartered’s stated bear-case target.”

That convergence is not coincidental. Both Moody’s and Standard Chartered are pricing in the same downside risk. When major credit institutions and major investment banks independently arrive at the same stress figure, that number deserves attention.

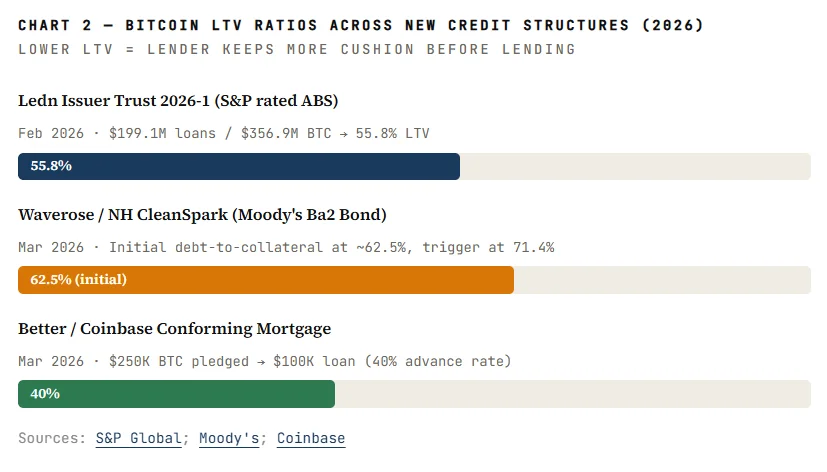

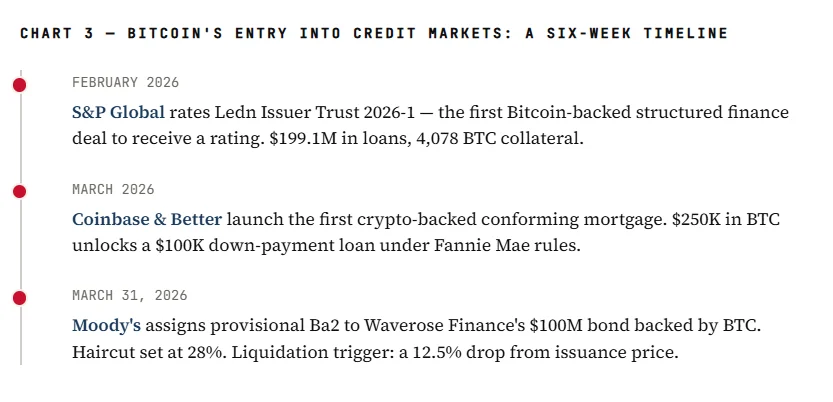

Three Credit Wrappers in Six Weeks

The Waverose deal is not a one-off. In February 2026, S&P Global assigned the first-ever rating to a Bitcoin-backed structured finance deal: Ledn Issuer Trust 2026-1. That transaction contained roughly $199.1 million in loans secured by 4,078 BTC worth about $356.9 million, an implied LTV of 55.8% at inception.

Then, in March, Coinbase and Better launched the first crypto-backed conforming mortgage. A borrower pledges $250,000 in Bitcoin to obtain a $100,000 down-payment loan. The first mortgage stays Fannie Mae-backed. The advance rate on pledged BTC: just 40%.

Why the Haircut Matters Beyond This Deal

Each new structure sets a precedent. When Moody’s stresses BTC at 72 cents on the dollar, that figure becomes a reference point. Other lenders, other bond deals, and other regulators will look at it. Haircuts tend to cluster. They become standard.

The risk is systemic. If multiple Bitcoin-backed structures share similar trigger levels, a single sharp price move could trigger forced selling across many positions simultaneously. That selling pressure itself deepens the price drop. Each structure is individually modest. Together, they could amplify volatility in ways no single deal’s prospectus describes.

Bitcoin’s integration into credit markets provides genuine utility for holders seeking liquidity without selling. But that same integration creates a new class of price risk, one driven not by sentiment, but by collateral maintenance calls that computers execute automatically.

“Bitcoin crossed a meaningful threshold. It is no longer just an asset people hold. It is now an asset that credit structures can liquidate on schedule, whether the market is ready or not.”